MaxedOutMama

MaxedOutMama

Thursday, June 30, 2011

Ho-Hum Thursday

NACM Update. This sounds a cautionary note. The strong drop in favorable indicators on manufacturing is not that good a sign. Both the combined index and the manufacturing index are negative this month, although the decline is much, much less than last month's reading. Indications of financial stress remain, but at least one can say that this month's survey does not show a cartwheel into disaster. We will have to see how this shapes up over the summer. Since April, the index of favorable factors for mfrg: 62.7 > 59.5 > 56.9. This should be strongly associated with production pace.

K.C. Update: This one rebounds as well, hardly surprising since it is strongly correlated to Chicago PMI. Inventory build, but production, etc, go back to April levels. Below March, but a recovery from May's unhappiness.

Update: I KNEW THERE WOULD BE A PONY IN HERE SOMEWHERE. Chicago PMI. Inventory cleared, and it probably is mostly on autos. There is a large rebound in headline, employment is growing but at a slower pace, and order backlogs fell to SA negative territory at 49.3. Still, as long as inventory is cycling through there is no need to panic and run screaming. This report is quite consistent with slowing growth trends in manufacturing, but not collapsing growth trends. A huge distinction. End update.

Well, at least it's no worse.

Initial claims advance was 428,000 from last week's unrevised 429,000. The four week moving average for initial claims moved up slightly to 426,750. The four week trajectory is 430,000 > 420,000 > 429,000 > 428,000. For a series so volatile, this is oddly consistent. There don't seem to be any distorting effects in here - it just is at this pace.

The pace suggests weakness in the job market this summer, mostly in services. Services tend to be more stable employment so that is probably why the series is so oddly even at this point. Nothing ever happens quickly in services, but jobs lost tend to take a long while before they are replaced, so that is not necessarily a good thing.

Later today Chicago PMI comes out, followed by K. C. Manufacturing survey.

Since we have indications of service weakness (concentrated in service directly to somewhat strapped consumers, with some residual weakness in services to state and local governments), I am watching the inventory portions of the manufacturing surveys with great attention. The natural response to building inventories is to scale back production, and if we see enough of a scale back conjoined to enough weakness in services, that will put us into a contraction cycle. The actual mechanisms causing a contraction cycle don't develop quickly - by the time it is overt you usually are six to eight months into the contraction cycle. Specifically, what I am looking for in these surveys is this progression (from May Chicago PMI):

Many analysts are predicting a better economy, but in reality it will all depend on inventories.

Ford made cheerful comments about car sales later this year, which is encouraging, although Ford also said it did not expect June sales to be all that great. Weakness in car sales is one of the factors that tends to push the economy into a contraction cycle, so I am waiting for June car sales in great anxiety. Ford did pretty well last month compared to GM. Ford's production lines are running all out.

My view can best be summed up by the observation that I am seeing a spate of absurdly optimistic economic projections. For example, Germany's economy is, by most standards, doing just great, with unemployment continuing to drop to a multi-decade low. But in May German retail sales fell 2.8%. German inflation is around 2.4% currently - households are just tight on energy costs, which now include electricity costs from Germany's foray into wind and solar power, which are jacking up German household's utility bills.

This is a regressive trend - most wealthier German households can install solar panels, which carry such a huge feed-in subsidy that they can essentially exempt themselves from this portion of inflation. So household that can do this have done it in great numbers - the revenue stream is guaranteed for over a decade. But the poorer households end up paying for it because the tab for extremely costly electricity generation is distributed on all their bills.

Expectations of some sort of surge in consumer spending on gas prices in the US are idiotic. It's not going to happen; in fact gas prices hugely rebounded yesterday on currency trends. Inflation is also raising auto prices in the US along with everything else, and I think affordability is one of the factors in what seems to be a somewhat weaker sales trend there.

Australia will probably raise rates next. ECB may not do it in June, but probably will by the fall. China is fighting its inflation war with little success to date, so it is letting its currency rise to help with import costs. This is not going to work out all that well for China, because most Chinese inflation is internally sourced at this point. The Fed ought to start raising US rates, paradoxically it would improve our economy in the short term. But it is too dangerous - the Fed does not have the guts to try it.

Given the global situation, commodities cannot adjust downwards significantly in pricing, but must continue to press on real incomes. So economic growth varies pretty much in proportion to each economy's individual consumption/production balance. The only short-term fix for the US is to raise interest rates, which will both suppress commodity pricing by making it more expensive to play in the market and adjust away some of the currency effect now very obvious in dollar-priced commodities.

K.C. Update: This one rebounds as well, hardly surprising since it is strongly correlated to Chicago PMI. Inventory build, but production, etc, go back to April levels. Below March, but a recovery from May's unhappiness.

Update: I KNEW THERE WOULD BE A PONY IN HERE SOMEWHERE. Chicago PMI. Inventory cleared, and it probably is mostly on autos. There is a large rebound in headline, employment is growing but at a slower pace, and order backlogs fell to SA negative territory at 49.3. Still, as long as inventory is cycling through there is no need to panic and run screaming. This report is quite consistent with slowing growth trends in manufacturing, but not collapsing growth trends. A huge distinction. End update.

Well, at least it's no worse.

Initial claims advance was 428,000 from last week's unrevised 429,000. The four week moving average for initial claims moved up slightly to 426,750. The four week trajectory is 430,000 > 420,000 > 429,000 > 428,000. For a series so volatile, this is oddly consistent. There don't seem to be any distorting effects in here - it just is at this pace.

The pace suggests weakness in the job market this summer, mostly in services. Services tend to be more stable employment so that is probably why the series is so oddly even at this point. Nothing ever happens quickly in services, but jobs lost tend to take a long while before they are replaced, so that is not necessarily a good thing.

Later today Chicago PMI comes out, followed by K. C. Manufacturing survey.

Since we have indications of service weakness (concentrated in service directly to somewhat strapped consumers, with some residual weakness in services to state and local governments), I am watching the inventory portions of the manufacturing surveys with great attention. The natural response to building inventories is to scale back production, and if we see enough of a scale back conjoined to enough weakness in services, that will put us into a contraction cycle. The actual mechanisms causing a contraction cycle don't develop quickly - by the time it is overt you usually are six to eight months into the contraction cycle. Specifically, what I am looking for in these surveys is this progression (from May Chicago PMI):

Many analysts are predicting a better economy, but in reality it will all depend on inventories.

Ford made cheerful comments about car sales later this year, which is encouraging, although Ford also said it did not expect June sales to be all that great. Weakness in car sales is one of the factors that tends to push the economy into a contraction cycle, so I am waiting for June car sales in great anxiety. Ford did pretty well last month compared to GM. Ford's production lines are running all out.

My view can best be summed up by the observation that I am seeing a spate of absurdly optimistic economic projections. For example, Germany's economy is, by most standards, doing just great, with unemployment continuing to drop to a multi-decade low. But in May German retail sales fell 2.8%. German inflation is around 2.4% currently - households are just tight on energy costs, which now include electricity costs from Germany's foray into wind and solar power, which are jacking up German household's utility bills.

This is a regressive trend - most wealthier German households can install solar panels, which carry such a huge feed-in subsidy that they can essentially exempt themselves from this portion of inflation. So household that can do this have done it in great numbers - the revenue stream is guaranteed for over a decade. But the poorer households end up paying for it because the tab for extremely costly electricity generation is distributed on all their bills.

Expectations of some sort of surge in consumer spending on gas prices in the US are idiotic. It's not going to happen; in fact gas prices hugely rebounded yesterday on currency trends. Inflation is also raising auto prices in the US along with everything else, and I think affordability is one of the factors in what seems to be a somewhat weaker sales trend there.

Australia will probably raise rates next. ECB may not do it in June, but probably will by the fall. China is fighting its inflation war with little success to date, so it is letting its currency rise to help with import costs. This is not going to work out all that well for China, because most Chinese inflation is internally sourced at this point. The Fed ought to start raising US rates, paradoxically it would improve our economy in the short term. But it is too dangerous - the Fed does not have the guts to try it.

Given the global situation, commodities cannot adjust downwards significantly in pricing, but must continue to press on real incomes. So economic growth varies pretty much in proportion to each economy's individual consumption/production balance. The only short-term fix for the US is to raise interest rates, which will both suppress commodity pricing by making it more expensive to play in the market and adjust away some of the currency effect now very obvious in dollar-priced commodities.

Wednesday, June 29, 2011

And We Don't Have Two Election Cycles

Seriously, we don't.

We can't implement the provisions of the health care reform act - we don't have the money to do it, and if we were to try to cut Medicare reimbursements as scheduled, most non-wealthy Medicare recipients would have increasing difficulties getting access to health care. No one at the CBO is willing to use the official plan as a basis for economic forecasts, because it is nonsense. Holtz-Eakin isn't alone in this.

The states don't have the money to spend on their portion of Medicaid, which is the chief mechanism for covering more people under the act. The private sector doesn't have the money to spend on insurance, so the public subsidy is scheduled to be much higher than theorized.

And even if it weren't for health care reform, the pressure of the retirement crunch is just beginning to build and is going to place so much stress on state and local governments that massive changes are necessary there. The only way to balance the budget is through mechanisms like President Obama's reform commission came up with, and there a large part of the contribution comes from a rise in middle-class taxation.

One of our worst problems is the green energy drive. For the most part, the strategy is not just a failure but a remarkable failure that will undercut the global trends which would tend to support a slow resurgence of US manufacturing.

Much of our federal deficit problem over the long term derives from a vast expansion of federal spending on health care. CBO blog post on the issue:

1) ...if the government’s programs and activities are maintained in their current form, spending for everything other than interest will rise to between 23 percent and 25 percent of GDP in 2035, compared with an average of 18.6 percent of GDP experienced over the past 40 years.

2) ... if current laws remained in place, spending on the major mandatory health care programs (Medicare, Medicaid, the Children’s Health Insurance Program, and the health insurance subsidies that will be provided through insurance exchanges) alone would grow from less than 6 percent of GDP today to about 9 percent in 2035 and would continue to increase thereafter.

3) Social Security and the major mandatory health care programs already account for about 46 percent of federal noninterest spending. Under current laws, that percentage will grow to nearly 60 percent by 2021 and to 67 percent by 2035, CBO projects.

You can't fool much with Social Security payments, because most Social Security recipients get very modest Social Security checks already, and reforms to CPI calculations have tended rather to diminish the real benefit over time. So the reform has to be to health benefits.

In another post, CBO addresses the long-term forecast by substituting their own more realistic assumptions on health care payments rather than the faked-up Pelosi deal:

The unthinkable has happened in NJ, because NJ had to reform. The unthinkable had better happen at the federal level very quickly.

We can't implement the provisions of the health care reform act - we don't have the money to do it, and if we were to try to cut Medicare reimbursements as scheduled, most non-wealthy Medicare recipients would have increasing difficulties getting access to health care. No one at the CBO is willing to use the official plan as a basis for economic forecasts, because it is nonsense. Holtz-Eakin isn't alone in this.

The states don't have the money to spend on their portion of Medicaid, which is the chief mechanism for covering more people under the act. The private sector doesn't have the money to spend on insurance, so the public subsidy is scheduled to be much higher than theorized.

And even if it weren't for health care reform, the pressure of the retirement crunch is just beginning to build and is going to place so much stress on state and local governments that massive changes are necessary there. The only way to balance the budget is through mechanisms like President Obama's reform commission came up with, and there a large part of the contribution comes from a rise in middle-class taxation.

One of our worst problems is the green energy drive. For the most part, the strategy is not just a failure but a remarkable failure that will undercut the global trends which would tend to support a slow resurgence of US manufacturing.

Much of our federal deficit problem over the long term derives from a vast expansion of federal spending on health care. CBO blog post on the issue:

1) ...if the government’s programs and activities are maintained in their current form, spending for everything other than interest will rise to between 23 percent and 25 percent of GDP in 2035, compared with an average of 18.6 percent of GDP experienced over the past 40 years.

2) ... if current laws remained in place, spending on the major mandatory health care programs (Medicare, Medicaid, the Children’s Health Insurance Program, and the health insurance subsidies that will be provided through insurance exchanges) alone would grow from less than 6 percent of GDP today to about 9 percent in 2035 and would continue to increase thereafter.

3) Social Security and the major mandatory health care programs already account for about 46 percent of federal noninterest spending. Under current laws, that percentage will grow to nearly 60 percent by 2021 and to 67 percent by 2035, CBO projects.

You can't fool much with Social Security payments, because most Social Security recipients get very modest Social Security checks already, and reforms to CPI calculations have tended rather to diminish the real benefit over time. So the reform has to be to health benefits.

In another post, CBO addresses the long-term forecast by substituting their own more realistic assumptions on health care payments rather than the faked-up Pelosi deal:

The unthinkable has happened in NJ, because NJ had to reform. The unthinkable had better happen at the federal level very quickly.

Briefly

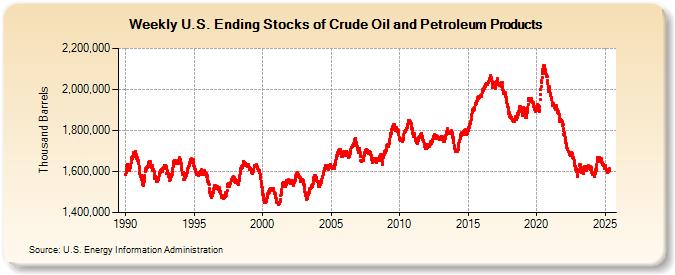

Crude inventories isn't moving much. Under the circs that can be regarded as a good thing, I suppose, except these levels seem to show real economic trouble. I can't see persistent drops in YoY diesel without thinking it is a sign of recession. After a point the temporary becomes the average - but at least the average isn't moving that much.

Pending home sales really isn't moving much either. May was about at the Jan/Feb levels. March was high, followed by a crash in April, but that sequence was almost certainly due to a rise in FHA insurance premiums in mid April, causing people to rush it a bit and then a decline. I think we are bouncing along the bottom of the housing market in terms of activity this year. That doesn't mean in terms of prices - in many areas, prices will tend to drift down for years to come.

Mostly I'm watching Treasuries. Indications vary. Some of this is currency flux, as the commodities seem to be. Some of it is just plain nerves about what the result of QE2's end will be.

Trichet spoke a few days ago, using ECB-code for an interest rate rise. This is very definitely moving the currencies. This weekend the various European finance groupies get together and try to orchestrate a Greek sovereign voluntary rollover deal. To be lined up and have your pocket picked while being forced to shout "Please sir, may I have another!" so the ratings firms don't clean you out is not going to improve your appetite for bad debt.

I would think that investors are contemplating US obligations with a mind to the result of not contemplating Greek obligations. Admittedly there is more time for the US, but that doesn't mean 20 years. A lot depends on the debt figures Congress comes up with. So in a way the Greek tragedy and the US farce are conjoined. The end of the Greek tragedy is uncertain. The US farce is just the first act.

Major Action in Treasuries continues. Look at the 7 year auction:

'

Look at today's trading.

Pending home sales really isn't moving much either. May was about at the Jan/Feb levels. March was high, followed by a crash in April, but that sequence was almost certainly due to a rise in FHA insurance premiums in mid April, causing people to rush it a bit and then a decline. I think we are bouncing along the bottom of the housing market in terms of activity this year. That doesn't mean in terms of prices - in many areas, prices will tend to drift down for years to come.

Mostly I'm watching Treasuries. Indications vary. Some of this is currency flux, as the commodities seem to be. Some of it is just plain nerves about what the result of QE2's end will be.

Trichet spoke a few days ago, using ECB-code for an interest rate rise. This is very definitely moving the currencies. This weekend the various European finance groupies get together and try to orchestrate a Greek sovereign voluntary rollover deal. To be lined up and have your pocket picked while being forced to shout "Please sir, may I have another!" so the ratings firms don't clean you out is not going to improve your appetite for bad debt.

I would think that investors are contemplating US obligations with a mind to the result of not contemplating Greek obligations. Admittedly there is more time for the US, but that doesn't mean 20 years. A lot depends on the debt figures Congress comes up with. So in a way the Greek tragedy and the US farce are conjoined. The end of the Greek tragedy is uncertain. The US farce is just the first act.

Major Action in Treasuries continues. Look at the 7 year auction:

Treasury supply may finally be getting ahead of demand. That's a conclusion that can reasonably be drawn from this week's poorly received string of coupon auctions including today's $29 billion offering of 7-year notes. Coverage of 2.62 is light for this issue while the high yield of 2.43 percent is three basis points over expectations. In a sign of weak retail demand, dealers ended up taking down an outsized 56 percent share of the offering. Demand for Treasuries is sinking following today's results.It's been weakening. The longer terms are suffering; bid/covers on the shorts this week were just fine. The four week on the 28th had a bid/cover of 4.57 and a yield of 1/2 a basis point. (0.005). The 52 week at the same time and same day had a bid/cover of 4.15% and a yield of 20 basis points (0.20). An hour and a half later, the 5 year had a bid/cover of 2.59 and a yield of 1.5%. Compared to earlier auctions this year, this is a definite move down in demand.

'

Look at today's trading.

Tuesday, June 28, 2011

Just Reading Along

Richmond Fed - The good thing about this is that the overall rose to 3 from -6 in May, which was a dizzying drop from 10 in April. The bad thing is that inventories of finished goods took a wild hop up to 23 (from 10 > 12 in recent months). Inventory builds aren't necessarily bad if shipments are rising, but in May shipments moved to -13, and in June shipments were still marginally negative at -1. So this may be a report I don't want to read next month. Also the backlog of orders was still quite negative at -16. Prices paid current and expectations are in the 4s - better than last month, but still in compress territory. Prices received are in the lower 2s, and expectations are similar.

The average workweek fell to -5, but that is not too paid because number of employees was still healthily positive at 12. Wages are still rising; in April that index was 22, it fell to 6 in May and rose to 9 in June. So probably manufacturers are trying to control costs by limiting overtime, and are staffing more to ensure that happens.

Note: I am not certain, but I suspect that part of the Texas slump shown yesterday is related to Japanese supply problems. Autos we pretty much know about, and because May Southeastern PMI was better than national, I think autos had a limited, although negative, influence to date. Electronics component shortages should be showing up about now.

Given the power problems in Japan, I am expecting some continuing influence. The long and the short of it is that out of 54 reactors Japan has 17 now running, no new restarts have been approved (on those that were shut down for normal maintenance), and this summer at least four more have to shut down for maintenance. At least three utilities have asked for the 15% power conservation; the problem is compounded because some of the larger companies had shifted movable work out of the Tokyo area only to find themselves facing new restrictions.

The average workweek fell to -5, but that is not too paid because number of employees was still healthily positive at 12. Wages are still rising; in April that index was 22, it fell to 6 in May and rose to 9 in June. So probably manufacturers are trying to control costs by limiting overtime, and are staffing more to ensure that happens.

Note: I am not certain, but I suspect that part of the Texas slump shown yesterday is related to Japanese supply problems. Autos we pretty much know about, and because May Southeastern PMI was better than national, I think autos had a limited, although negative, influence to date. Electronics component shortages should be showing up about now.

Given the power problems in Japan, I am expecting some continuing influence. The long and the short of it is that out of 54 reactors Japan has 17 now running, no new restarts have been approved (on those that were shut down for normal maintenance), and this summer at least four more have to shut down for maintenance. At least three utilities have asked for the 15% power conservation; the problem is compounded because some of the larger companies had shifted movable work out of the Tokyo area only to find themselves facing new restrictions.

Monday, June 27, 2011

Eek, Squeak, Yelp

Texas, Dallas Fed.

The overall report was less depressing. The hours worked index was still positive, if only marginally, capacity utilization was -0.8, falling 11.9 from April, and new orders and employment were still increasing. Future expectations are still marginally positive (the red dotted line above). I'm really surprised, though - I thought Texas would be pretty decent. This is not pretty decent. I can't really claim that it is more worry than anything else because of the large drop in capacity utilization.

ATA Truck Tonnage for May was bad also. In just a few months the direction has changed a lot. We kind of knew that because of diesel; so far diesel supplied has not rebounded. Last week the four week supplied average was down 5.7% YoY, which does not forecast well for ATA Truck Tonnage in June. Rail is holding, and may be doing slightly better in June, but it is probably doing that from displaced truck freight. Much more freight rolls on trucks than trains.

Tomorrow we get Richmond Fed. If it's not good I don't want to look at it; last month it was surprisingly bad. The Richmond Fed also puts out the survey of agricultural conditions, which was neutral with price concerns dropping demand for pricey stuff, and lenders worried about credit. Kansas City is due to weigh in also, I think on Thursday. K.C.'s May survey was not that much fun; the headline was neutral at 1, but production, shipments, new orders and the average workweek indices dropped, so I probably don't want to see June K.C. either:

I'm thinking that the odds that I will really like the next bar on that graph aren't that hot, but it should update automatically so I can just scroll down here, and if it doesn't look too bad, I'll deign to read the report.

I have been saving the following for an opportune moment full of cheer and hilarity when everyone would enjoy good laugh. Unfortunately, after looking at the Dallas Fed survey I realized that such a moment may not come. However, if you are personally in a good mood, you might enjoy St. Louis' scholarly review of the burning issue - could it be, that by any unforeseen and indeed unforeseeable chance, that an easy money policy might drive up asset and commodity prices? Could it be and who'd a thunk?

I do have to look at June car sales when those figures are released. Also inventory. I use Ward's figures. I have been sadly staring at MV shipments on the rail reports, but sales can be different so perhaps it won't be too bad. In May car sales dropped YoY and, cough, inventories rose for Chrysler and GM, although not for Ford and not for most of the foreigns. However looking at April beginning YTD MV rail shipments (still up 12.8% YoY) versus the most recent week's YTD YoY of 7.2%, I don't think I'm going to like the Ward's data that much. Of course I have to read Chicago PMI, NACM, and I'll look at the ISM indices. Somewhere in there something will look better.

Anyway, when I sum up my reading plans for the near future, I realize that I am only looking for good news to rebut the highly probable reality that Q3 is going to mark the slide into outright contraction. The reason is timing; end user inflation for most primary goods is still escalating, and oil prices won't have time to fall far enough to offset it. Most older people are facing higher drug costs and the doughnut hole this summer; they'll pull back hard on spending. Their spending would be sparse anyway, because food costs are too high and no SS COLAs for several years have impacted their finances most unfavorably.

The hit on the service businesses is proceeding along, and actually the economic infusion at the top end (FICA cuts for high earners) falls off hard by August (they start reaching cap then)/September. So relatively that contribution fades out but the effect of inflation is still there.

Then to cap it all, due to Congress' failure to extend unemployment benefits for the 99rs, by late summer the bulk of those who haven't found employment will find themselves with no unemployment benefits. This spring the drop off has been pretty hard, and it is undoubtedly affecting some spending patterns.

Economic stimulus in 2011 was very front-loaded. Initial claims are up. What can I say? When oil prices are this high and the Dallas Fed produces a survey that ugly-looking, it is hard to be optimistic. I began this year with the thesis that everything depended on auto sales - that this was the sole remaining real growth edge for the economy. It appears that we have lost that growth edge. If this is true, it is going to be hard to pull out and see much in the way of growth in the third quarter.

There are pockets of real growth out there remaining, but you have to understand that we were in a bad position at the beginning of the year. The net Gross Private Domestic Investment over Q4/Q1 was negative. We do have suppressed demand rebounds still on things like cars, but an unemployment rate over 8% sharply limits the scope, and the negative trajectory for many service businesses is going to limit their equipment spending.

Housing and CRE is bad this year and will not have any significant impact on growth. The only possible growth avenue this year was from trickle-up from the bottom 40%, and the Fed;'s failure to realize that boosting asset prices had to come at the cost of real incomes for the bottom 40% pretty much destroyed that, then Congress and our dear, dear Community Organizer made sure to organize the bottom 40% out of the growth picture. It was a one-two blow that our economy was too weak to withstand.

So this is the Fed downturn - an economic horror movie probably coming to a theater near you. If Andrew Jackson were running for president in 2012, he'd win in a landslide.

Right now I am struggling with this reality. People will die because of this. Right now I truly despise all the talking heads.

The overall report was less depressing. The hours worked index was still positive, if only marginally, capacity utilization was -0.8, falling 11.9 from April, and new orders and employment were still increasing. Future expectations are still marginally positive (the red dotted line above). I'm really surprised, though - I thought Texas would be pretty decent. This is not pretty decent. I can't really claim that it is more worry than anything else because of the large drop in capacity utilization.

ATA Truck Tonnage for May was bad also. In just a few months the direction has changed a lot. We kind of knew that because of diesel; so far diesel supplied has not rebounded. Last week the four week supplied average was down 5.7% YoY, which does not forecast well for ATA Truck Tonnage in June. Rail is holding, and may be doing slightly better in June, but it is probably doing that from displaced truck freight. Much more freight rolls on trucks than trains.

Tomorrow we get Richmond Fed. If it's not good I don't want to look at it; last month it was surprisingly bad. The Richmond Fed also puts out the survey of agricultural conditions, which was neutral with price concerns dropping demand for pricey stuff, and lenders worried about credit. Kansas City is due to weigh in also, I think on Thursday. K.C.'s May survey was not that much fun; the headline was neutral at 1, but production, shipments, new orders and the average workweek indices dropped, so I probably don't want to see June K.C. either:

I'm thinking that the odds that I will really like the next bar on that graph aren't that hot, but it should update automatically so I can just scroll down here, and if it doesn't look too bad, I'll deign to read the report.

I have been saving the following for an opportune moment full of cheer and hilarity when everyone would enjoy good laugh. Unfortunately, after looking at the Dallas Fed survey I realized that such a moment may not come. However, if you are personally in a good mood, you might enjoy St. Louis' scholarly review of the burning issue - could it be, that by any unforeseen and indeed unforeseeable chance, that an easy money policy might drive up asset and commodity prices? Could it be and who'd a thunk?

I do have to look at June car sales when those figures are released. Also inventory. I use Ward's figures. I have been sadly staring at MV shipments on the rail reports, but sales can be different so perhaps it won't be too bad. In May car sales dropped YoY and, cough, inventories rose for Chrysler and GM, although not for Ford and not for most of the foreigns. However looking at April beginning YTD MV rail shipments (still up 12.8% YoY) versus the most recent week's YTD YoY of 7.2%, I don't think I'm going to like the Ward's data that much. Of course I have to read Chicago PMI, NACM, and I'll look at the ISM indices. Somewhere in there something will look better.

Anyway, when I sum up my reading plans for the near future, I realize that I am only looking for good news to rebut the highly probable reality that Q3 is going to mark the slide into outright contraction. The reason is timing; end user inflation for most primary goods is still escalating, and oil prices won't have time to fall far enough to offset it. Most older people are facing higher drug costs and the doughnut hole this summer; they'll pull back hard on spending. Their spending would be sparse anyway, because food costs are too high and no SS COLAs for several years have impacted their finances most unfavorably.

The hit on the service businesses is proceeding along, and actually the economic infusion at the top end (FICA cuts for high earners) falls off hard by August (they start reaching cap then)/September. So relatively that contribution fades out but the effect of inflation is still there.

Then to cap it all, due to Congress' failure to extend unemployment benefits for the 99rs, by late summer the bulk of those who haven't found employment will find themselves with no unemployment benefits. This spring the drop off has been pretty hard, and it is undoubtedly affecting some spending patterns.

Economic stimulus in 2011 was very front-loaded. Initial claims are up. What can I say? When oil prices are this high and the Dallas Fed produces a survey that ugly-looking, it is hard to be optimistic. I began this year with the thesis that everything depended on auto sales - that this was the sole remaining real growth edge for the economy. It appears that we have lost that growth edge. If this is true, it is going to be hard to pull out and see much in the way of growth in the third quarter.

There are pockets of real growth out there remaining, but you have to understand that we were in a bad position at the beginning of the year. The net Gross Private Domestic Investment over Q4/Q1 was negative. We do have suppressed demand rebounds still on things like cars, but an unemployment rate over 8% sharply limits the scope, and the negative trajectory for many service businesses is going to limit their equipment spending.

Housing and CRE is bad this year and will not have any significant impact on growth. The only possible growth avenue this year was from trickle-up from the bottom 40%, and the Fed;'s failure to realize that boosting asset prices had to come at the cost of real incomes for the bottom 40% pretty much destroyed that, then Congress and our dear, dear Community Organizer made sure to organize the bottom 40% out of the growth picture. It was a one-two blow that our economy was too weak to withstand.

So this is the Fed downturn - an economic horror movie probably coming to a theater near you. If Andrew Jackson were running for president in 2012, he'd win in a landslide.

Right now I am struggling with this reality. People will die because of this. Right now I truly despise all the talking heads.

BIS Annual Report

The 81st Bank of International Settlements (BIS) Annual report was published yesterday. I have not finished it, but there is some particularly juicy stuff in here that can be read as oppositional to the Fed.

If you read nothing else, read the chapter on low interest rates. I think every adult citizen of the US with a normal to above IQ should read this, and think about it. It's not difficult.

The fiscal sustainability chapter is of most relevance to current US political debate. The BIS takes a position somewhat more adverse to debt than Paul Krugman's, to put it delicately. On page 66 you will find graphs for some of the more significant industrialized countries:

The green line is what would happen if primary balance (gov revenues - gov expenditures less interest) were improved by 10% over 10 years at a rate of 1% a year. In the US, this would only help until about 2025.

The blue line is what would happen in the green scenario AND by holding age-related expenditures constant as a percent of GDP.

As BIS notes:

Jill, this chapter contains the answer to your questions. We have to make policy decisions by 2017 that will change the social contract in the US for the worse. If we don't make them, the social contract in the US will change hugely for the worse.

From the point of view of the average family, the economy of the US in the 2020's will seem far more like the economy in the later 50s and 60s if we correct earlier. If we correct later, it will be worse.

This need not lead to dire disaster for most people and for most families if we address the situation realistically. Unfortunately, most of our current catalog of public authorities on the issue are unwilling to be realistic. Electoral time is running out. One key in the US is to abandon our current energy policies - they are too destructive of economic growth. Eventually the correction in the US will lead to more production of items for consumer needs, and you can't run an industrialized economy on wind and solar. You can do coal, NG and/or nuclear, but you cannot do current "green". Germany is about to find this out; Japan is probably going to NG to provide power.

The other thing one can clearly derive from this report is that China is facing a huge economic transition which will be difficult.

If you read nothing else, read the chapter on low interest rates. I think every adult citizen of the US with a normal to above IQ should read this, and think about it. It's not difficult.

The fiscal sustainability chapter is of most relevance to current US political debate. The BIS takes a position somewhat more adverse to debt than Paul Krugman's, to put it delicately. On page 66 you will find graphs for some of the more significant industrialized countries:

The green line is what would happen if primary balance (gov revenues - gov expenditures less interest) were improved by 10% over 10 years at a rate of 1% a year. In the US, this would only help until about 2025.

The blue line is what would happen in the green scenario AND by holding age-related expenditures constant as a percent of GDP.

As BIS notes:

Coming on top of the improvement in the primary balance, the freeze of the GDP share of age-related expenditures leads to a faster decline in the debt/GDP ratio or a slower rate of increase. Preventing age-related spending from growing faster than GDP for the entire projection horizon may be somewhat unrealistic. Nonetheless, the results suggest that early efforts to reduce future age-related spending or finance the spending through additional taxes and other measures (discussed below) could significantly improve fiscal sustainability in several countries over the medium term.In fact, BIS takes an extremely anti-Krugman position:

Although the evidence on the growth implications of high levels of public debt is slim, it suggests that the effects could be significant. Among countries with a debt/GDP ratio of more than 90%, the median growth rate of real GDP is 1 percentage point lower (and the average is 4 percentage points lower) than in countries with a lower ratio. Recent evidence also suggests that the expected increase in the debt/GDP ratio in the advanced economies for the 2007–15 period may permanently reduce future growth of potential output by more than half a percentage point annually.6Please note that the BIS' inflection point for the US is about 2015. When you are playing around with the debt levels we already have plus the demographics we have plus the deficits we are running, delaying action for just a few years can have a huge effect on future outcomes.

Jill, this chapter contains the answer to your questions. We have to make policy decisions by 2017 that will change the social contract in the US for the worse. If we don't make them, the social contract in the US will change hugely for the worse.

From the point of view of the average family, the economy of the US in the 2020's will seem far more like the economy in the later 50s and 60s if we correct earlier. If we correct later, it will be worse.

This need not lead to dire disaster for most people and for most families if we address the situation realistically. Unfortunately, most of our current catalog of public authorities on the issue are unwilling to be realistic. Electoral time is running out. One key in the US is to abandon our current energy policies - they are too destructive of economic growth. Eventually the correction in the US will lead to more production of items for consumer needs, and you can't run an industrialized economy on wind and solar. You can do coal, NG and/or nuclear, but you cannot do current "green". Germany is about to find this out; Japan is probably going to NG to provide power.

The other thing one can clearly derive from this report is that China is facing a huge economic transition which will be difficult.

GrumpWatch I.0

Reading financial reports is no fun these days.

First up: BEA's Personal Income and Outlays for May. There look to have been some downward revisions for April.

Look at real (chained 2005 dollars) PCE. That has a lot to do with the escalating rise of money in Other Deposits on H.8. Most households probably are experiencing falling real incomes and pretty sharp increases in the their bill for basics, so they respond by cutting more discretionary spending.

Smaller businesses aren't doing too well:

I don't understand how all the big outfits can be predicting Q2 GDP so high even after cutting their forecasts down a percent and a half. Real growth in Personal Consumption Expenditures is absent the picture, and just by looking at H.8 (do they???) you can tell that everyone didn't run out and blow the wad in June.

The main problem right now for the economy is food prices and the rise in service costs, but that isn't going to evaporate.

First up: BEA's Personal Income and Outlays for May. There look to have been some downward revisions for April.

Look at real (chained 2005 dollars) PCE. That has a lot to do with the escalating rise of money in Other Deposits on H.8. Most households probably are experiencing falling real incomes and pretty sharp increases in the their bill for basics, so they respond by cutting more discretionary spending.

Smaller businesses aren't doing too well:

Proprietors' income decreased $1.7 billion in May, in contrast to an increase of $3.2 billion in April.And our economy becomes ever more dependent on government payments!

Farm proprietors' income decreased $1.3 billion, the same decrease as in April. Nonfarm proprietors' income decreased $0.4 billion in May, in contrast to an increase of $4.5 billion in April.

Rental income of persons increased $3.3 billion in May, compared with an increase of $2.9 billion in April. Personal income receipts on assets (personal interest income plus personal dividend income) increased $10.0 billion, compared with an increase of $6.0 billion. Personal current transfer receipts increased $9.3 billion, in contrast to a decrease of $1.8 billion.

I don't understand how all the big outfits can be predicting Q2 GDP so high even after cutting their forecasts down a percent and a half. Real growth in Personal Consumption Expenditures is absent the picture, and just by looking at H.8 (do they???) you can tell that everyone didn't run out and blow the wad in June.

The main problem right now for the economy is food prices and the rise in service costs, but that isn't going to evaporate.

Sunday, June 26, 2011

Good Morning, Munchkins

The theme, I guess, is 2012.

I'm sorry this is German, but this article claims that the Greek rollover deal is supposed to be five years. On Friday the banking association was in talks; they apparently did not get what they were looking for - guarantees. Schauble is saying no. This weekend the large banks are supposed to show up and say how much they are willing to roll. But the banks still want an assurance that this will be treated as a voluntary deal by the credit ratings industry (this affects how it looks on their books). Five years? They should just write off 50% and be done with it. July 3rd is the drop-dead date for anteing up with the rollover amounts.

There is also this article about the claims of German firms that they can't get tax refunds from Greek authorities, because the Greek authorities don't have money to pay up! Let's just say that the real burden of debt on the Greek economy is probably higher than formally stated. The VAT refunds alone add up to a lot - as a result of the crisis, Greece raised its VAT from 21 to 23%. I did laugh a bit, because it is famously hard for foreigners to get refunds from German tax authorities.

Let's see - periodically I roam frantically through a bunch of company financial reports. The fun part is when you get to the Indian/Chinese ones, but I may never get there this round. I was struck by the Kellogg prediction of continued cost inflation in 2012:

Look at H.8 Assets and Liabilities of Commercial Banks. Deposits are liabilities to banks - they owe those funds to others. Over the last three months, the trend in annualized seasonally-adjusted growth trend in Other Deposits has been March: 4.8%, April: 7.7%, May 10.4%. Large time deposits are building too. A trend like this means that expectations for consumer spending should be adjusted downward.

One of the reasons (among many) I was so upset by the Bernank's presser was his nattering about mortgage underwriting terms. Virtually the entire board has climbed on that bandwagon, but it only makes them look like fools. SA residential delinquencies as of the first quarter were still at 10.23% - a slight increase from Q4 2010. This does not predict well. The charge-off rate on cards was still quite high at 7.22%.

Now, when you factor in the very real increase in consumer essential living costs (food, utilities, cars, fuel, medicines), you know that these trends were set to worsen this year, as a round of financially strapped but responsible consumers suddenly hit the point at which they can not pay any more. So granting mortgages to consumers with higher housing payments/income is not likely to work out well long term, and if the Fed really wants banks to do that, they should not have shoved inflation rates as high as the Fed has.

Now - U B Da Banker. One one hand, you are looking at some really crappy loan losses. On the other hand, you are looking at real income drops for many consumers. Further, with unemployment at 9.1% the "flex" for working borrowers, which has traditionally been odd jobs to catch back up, is gone. Not only that, but you are looking at a rise in initial unemployment claims, and such rises have been historically strongly associated with increased delinquencies. If you want to lend, you need to make sure that consumers have a pretty good chance of paying back the loan from their current income streams, because you have an increased chance of default just from job trends. You really need to watch their debt/income ratios.

Businesses are a little different. We have been through a winnowing process; if the business walks in and is currently in decent shape, you can review the last year and a half of financials and make a reasonably precise risk estimation. Credit quality of marginal businesses with high exposures to cost inflation risks is degenerating, but the point is that anyone reasonably competent should be able to estimate risk accurately! But not with consumers. Oh no. We have to also confront tax policy issues; under current law banks are facing the following issues in the next three years:

2012: A two-percent increase in FICA, which is going to shave some margin off those recent graduates who did get good tech jobs. A possible increase in taxes for most of the upper-middle class.

2013: Hey, ho, so, so, in the red the mortgage goes.... Few things shock and awe mortgage lenders quite like all those proposals to eliminate the mortgage tax deduction or property tax deduction. Also likely more tax increases from some local and state governments.

2014: Hey, ho, oh, no, CC repayments into medical insurance go.... Folks - the fact that so many waivers have been granted to various organizations kind of indicates that there will be a price shock in 2014. This is not the time to be cutting your borrower's margins, and you know what? That income loss is going to show up in some businesses as well.

Elizabeth Duke gave a rational-sounding speech recently. Perhaps that is because, cough, she actually knows something about commercial banking? Wiki bio. She is the only Fed member with any background in commercial banking. They don't seem to understand the impact of regulatory measures, which is pretty frightening. They don't seem to understand commercial banking, which makes me want to whimper and pee on myself like a beaten puppy. They don't seem to understand the impact of their own policies, which makes me want to grab them and shake them out of their coma. In fact, they don't even seem to know about regulation changes issued by the Fed.

So while I don't see what alternative we have to a central bank, I have to admit that Foo's claim that they have too much power is beginning to seem credible. All of life is trade-offs, and that's a truism. But when those who run the system don't even seem to understand what the trade-offs are, a rational person gets nervous. So to Foo, I would say that you would be likely to see a better-functioning Fed if you had commercial bankers as a larger percentage of governors. Commercial bankers must know a lot about Main Street. Most of the Fed doesn't, which is why they do seem like a convention of nutty professors. That's what they are.

I'm sorry this is German, but this article claims that the Greek rollover deal is supposed to be five years. On Friday the banking association was in talks; they apparently did not get what they were looking for - guarantees. Schauble is saying no. This weekend the large banks are supposed to show up and say how much they are willing to roll. But the banks still want an assurance that this will be treated as a voluntary deal by the credit ratings industry (this affects how it looks on their books). Five years? They should just write off 50% and be done with it. July 3rd is the drop-dead date for anteing up with the rollover amounts.

There is also this article about the claims of German firms that they can't get tax refunds from Greek authorities, because the Greek authorities don't have money to pay up! Let's just say that the real burden of debt on the Greek economy is probably higher than formally stated. The VAT refunds alone add up to a lot - as a result of the crisis, Greece raised its VAT from 21 to 23%. I did laugh a bit, because it is famously hard for foreigners to get refunds from German tax authorities.

Let's see - periodically I roam frantically through a bunch of company financial reports. The fun part is when you get to the Indian/Chinese ones, but I may never get there this round. I was struck by the Kellogg prediction of continued cost inflation in 2012:

David, the way we look at it is that we are in a long-term upward trend on cost of goods. The supply of grains has been relatively limited. The demand for grains is increasing, whether it be ethanol production or whether it be emerging market consumption or direct grains or meat-based products. And the result of that is you're going to see increased prices for grains over time. And so we would look at 2012 and say, yes, it's probably going to be inflationary. How inflationary? We have to wait to see where all the supply demand shakes out and where the prices shake out.That was on a response to a UBS question on page 12 of the transcript. Private brands are being beaten pretty solidly. The tremendous range of new products Kellogg is introducing is probably to achieve uniqueness so that they don't face store brand challengers, but it is a costly strategy! Gas prices are falling, but I doubt that consumers on average are getting ahead. Until they feel like they are, consumers are going to stockpile money.

Look at H.8 Assets and Liabilities of Commercial Banks. Deposits are liabilities to banks - they owe those funds to others. Over the last three months, the trend in annualized seasonally-adjusted growth trend in Other Deposits has been March: 4.8%, April: 7.7%, May 10.4%. Large time deposits are building too. A trend like this means that expectations for consumer spending should be adjusted downward.

One of the reasons (among many) I was so upset by the Bernank's presser was his nattering about mortgage underwriting terms. Virtually the entire board has climbed on that bandwagon, but it only makes them look like fools. SA residential delinquencies as of the first quarter were still at 10.23% - a slight increase from Q4 2010. This does not predict well. The charge-off rate on cards was still quite high at 7.22%.

Now, when you factor in the very real increase in consumer essential living costs (food, utilities, cars, fuel, medicines), you know that these trends were set to worsen this year, as a round of financially strapped but responsible consumers suddenly hit the point at which they can not pay any more. So granting mortgages to consumers with higher housing payments/income is not likely to work out well long term, and if the Fed really wants banks to do that, they should not have shoved inflation rates as high as the Fed has.

Now - U B Da Banker. One one hand, you are looking at some really crappy loan losses. On the other hand, you are looking at real income drops for many consumers. Further, with unemployment at 9.1% the "flex" for working borrowers, which has traditionally been odd jobs to catch back up, is gone. Not only that, but you are looking at a rise in initial unemployment claims, and such rises have been historically strongly associated with increased delinquencies. If you want to lend, you need to make sure that consumers have a pretty good chance of paying back the loan from their current income streams, because you have an increased chance of default just from job trends. You really need to watch their debt/income ratios.

Businesses are a little different. We have been through a winnowing process; if the business walks in and is currently in decent shape, you can review the last year and a half of financials and make a reasonably precise risk estimation. Credit quality of marginal businesses with high exposures to cost inflation risks is degenerating, but the point is that anyone reasonably competent should be able to estimate risk accurately! But not with consumers. Oh no. We have to also confront tax policy issues; under current law banks are facing the following issues in the next three years:

2012: A two-percent increase in FICA, which is going to shave some margin off those recent graduates who did get good tech jobs. A possible increase in taxes for most of the upper-middle class.

2013: Hey, ho, so, so, in the red the mortgage goes.... Few things shock and awe mortgage lenders quite like all those proposals to eliminate the mortgage tax deduction or property tax deduction. Also likely more tax increases from some local and state governments.

2014: Hey, ho, oh, no, CC repayments into medical insurance go.... Folks - the fact that so many waivers have been granted to various organizations kind of indicates that there will be a price shock in 2014. This is not the time to be cutting your borrower's margins, and you know what? That income loss is going to show up in some businesses as well.

Elizabeth Duke gave a rational-sounding speech recently. Perhaps that is because, cough, she actually knows something about commercial banking? Wiki bio. She is the only Fed member with any background in commercial banking. They don't seem to understand the impact of regulatory measures, which is pretty frightening. They don't seem to understand commercial banking, which makes me want to whimper and pee on myself like a beaten puppy. They don't seem to understand the impact of their own policies, which makes me want to grab them and shake them out of their coma. In fact, they don't even seem to know about regulation changes issued by the Fed.

So while I don't see what alternative we have to a central bank, I have to admit that Foo's claim that they have too much power is beginning to seem credible. All of life is trade-offs, and that's a truism. But when those who run the system don't even seem to understand what the trade-offs are, a rational person gets nervous. So to Foo, I would say that you would be likely to see a better-functioning Fed if you had commercial bankers as a larger percentage of governors. Commercial bankers must know a lot about Main Street. Most of the Fed doesn't, which is why they do seem like a convention of nutty professors. That's what they are.

Saturday, June 25, 2011

Fukushima Daiichi Reactor 2

The good news - I must start with that - is that TEPCO says it has got its decontamination rig working, and it is now planning to add the desalinization step. The water, according to TEPCO, has had its radioactivity levels reduced to 1/100,000th of original levels.

The bad news is pretty darned bad. TEPCO installed a new temperature gauge on Reactor 2, but says it isn't working because the temperature around the reactor is so high that all the water has evaporated from the pipes it is attempting to measure. Remember that TEPCO recently lowered water injection rates to all the reactors to try to prevent the flooding of the highly contaminated water. There may be just about no water in Reactor 2.

That may induce a thoughtful pause, and after that thoughtful pause, the news that the chopper drone TEPCO has been using to inspect areas over the reactors failed while flying over Reactor 2 may assume more significance to you. It was crashlanded on a portion of the Reactor 2 roof. The chopper was sent on a mission to test radioactivity above Reactor 2. This is a small device, and they are going to try to use one of the cranes to hook it off the roof.

In the link above, there is also information about modeling the ocean radioactivity dispersion from this incident.

In a way, it is a great relief that they came out and told us about the problems - the pause in the flow of news about the Reactor 2 project has been worrying me.

TEPCO is beyond bankrupt. It has no money to throw at the situation. It has asked the banks to roll over its loans for about 1% interest rate, and it needs more money from somewhere to try to deal with the Fukushima Daiichi incident. It should be a global priority to fund the recovery effort; Japan is going to have trouble finding the funds to rebuild the quake/tsunami damage; TEPCO theoretically has to pay compensation, and it has paid a little, but it doesn't have the money to do that either. So the Japanese government is going to have to assume the tab. I have been trying to glean facts about larger quake/rebuilding effort; it appears that the government quake fund is going to be exhausted by this event.

It's time to ante up. The workers at the site are in danger, and all the criticism (much warranted) about TEPCO's efforts kind of ignores the fact that they don't have the money to fund what is needed to do this.

PS: You can find more info on what they have done and are doing at each reactor at this link. After each reactor diagram page there is a summary of the major initiatives.

The bad news is pretty darned bad. TEPCO installed a new temperature gauge on Reactor 2, but says it isn't working because the temperature around the reactor is so high that all the water has evaporated from the pipes it is attempting to measure. Remember that TEPCO recently lowered water injection rates to all the reactors to try to prevent the flooding of the highly contaminated water. There may be just about no water in Reactor 2.

That may induce a thoughtful pause, and after that thoughtful pause, the news that the chopper drone TEPCO has been using to inspect areas over the reactors failed while flying over Reactor 2 may assume more significance to you. It was crashlanded on a portion of the Reactor 2 roof. The chopper was sent on a mission to test radioactivity above Reactor 2. This is a small device, and they are going to try to use one of the cranes to hook it off the roof.

In the link above, there is also information about modeling the ocean radioactivity dispersion from this incident.

In a way, it is a great relief that they came out and told us about the problems - the pause in the flow of news about the Reactor 2 project has been worrying me.

TEPCO is beyond bankrupt. It has no money to throw at the situation. It has asked the banks to roll over its loans for about 1% interest rate, and it needs more money from somewhere to try to deal with the Fukushima Daiichi incident. It should be a global priority to fund the recovery effort; Japan is going to have trouble finding the funds to rebuild the quake/tsunami damage; TEPCO theoretically has to pay compensation, and it has paid a little, but it doesn't have the money to do that either. So the Japanese government is going to have to assume the tab. I have been trying to glean facts about larger quake/rebuilding effort; it appears that the government quake fund is going to be exhausted by this event.

It's time to ante up. The workers at the site are in danger, and all the criticism (much warranted) about TEPCO's efforts kind of ignores the fact that they don't have the money to fund what is needed to do this.

PS: You can find more info on what they have done and are doing at each reactor at this link. After each reactor diagram page there is a summary of the major initiatives.

Friday, June 24, 2011

Absolute Devotion!

Or so Fisher of Dallas FRB claims:

Looking at durable goods, there are some signs of an inventory build that hint at weakness over the summer. See Table 2 in the release. This really is not surprising given the Empire State and Philly Fed surveys, but it tends to confirm that the patterns shown in those releases are general.

If you look at Table 10 in the GDP release, you'll see that annualized real personal income ex government transfers was 9.4 trillion versus 2008's 9.64 trillion. Therein lies the sensitivity of this economy to rapid price increases!

In the meantime, Moody's rudely and crudely made some comment or another about reviewing Italian banks' exposures to a decline in the Italian government's credit rating. The result was kind of a dramatic fall in the stock prices of various Italian banks, which is hardly going to help their position. Oil is trading down today with some reason!

The Draghi/Smaghi drama is about over. Draghi is in - this announcement probably forced from Sarkozy today in an attempt to shore up perceptions about continuity and stability at the ECB. They needed Draghi, because it always has been about Italy rather than the small fry that Greece and Portugal represent. We're clearly nearing the end of the European hand. Everyone's trying to drag out the hand by betting whatever they can afford, but sooner or later everyone's going to have to put their cards on the table. According to French newspapers, Smaghi is out at the end of the year. ECB:

There is a huge technical revision coming on GDP that will be published next month with the Q2 US advance GDP release. If it were not for that, Q2 GDP would be no higher than 1.4% annualized. As it is, we could get almost any number.

Developments in China are moving apace as well. I have the sensation that the 2008 crisis will reach its global culmination in 2012, but I don't know what it will be. The prior resolution was fake. This time it will have to be real.

“We are devoted absolutely to making sure that we don’t give rise to sustainable inflationary pressures that could be destructive,” Fisher said. “I very much look forward to an exit when it’s appropriate.”The major indicator in the GDP Q1 "final" release was higher inflation. The implicit price deflator for gross domestic purchases was 3.9%. Let's just say that if the Fed had an inflation goal in mind, they reached it with admirable speed. The YoY on GDP total (quarter from quarter a year ago) was 1.7% already at the end of March. Despite Fisher's laudable devotion, he claims that the Fed will not stomp on this tender little sprig of increasing prices it has so carefully nurtured. He claims they are of one mind on this.

Looking at durable goods, there are some signs of an inventory build that hint at weakness over the summer. See Table 2 in the release. This really is not surprising given the Empire State and Philly Fed surveys, but it tends to confirm that the patterns shown in those releases are general.

If you look at Table 10 in the GDP release, you'll see that annualized real personal income ex government transfers was 9.4 trillion versus 2008's 9.64 trillion. Therein lies the sensitivity of this economy to rapid price increases!

In the meantime, Moody's rudely and crudely made some comment or another about reviewing Italian banks' exposures to a decline in the Italian government's credit rating. The result was kind of a dramatic fall in the stock prices of various Italian banks, which is hardly going to help their position. Oil is trading down today with some reason!

The Draghi/Smaghi drama is about over. Draghi is in - this announcement probably forced from Sarkozy today in an attempt to shore up perceptions about continuity and stability at the ECB. They needed Draghi, because it always has been about Italy rather than the small fry that Greece and Portugal represent. We're clearly nearing the end of the European hand. Everyone's trying to drag out the hand by betting whatever they can afford, but sooner or later everyone's going to have to put their cards on the table. According to French newspapers, Smaghi is out at the end of the year. ECB:

The European Central Bank reiterated Friday that all members of its executive board, including Italy's Lorenzo Bini Smaghi, are appointed for eight-year terms and decide on their futures independently of outside pressure.The river looks to be running deep and fast, with forecasts of more water coming down. Italian two year yields at 3.28? The US two-year is rolling between 0.35 and 0.40%. Yikes!

There is a huge technical revision coming on GDP that will be published next month with the Q2 US advance GDP release. If it were not for that, Q2 GDP would be no higher than 1.4% annualized. As it is, we could get almost any number.

Developments in China are moving apace as well. I have the sensation that the 2008 crisis will reach its global culmination in 2012, but I don't know what it will be. The prior resolution was fake. This time it will have to be real.

Thursday, June 23, 2011

Oh, THURSDAY

Initial claims 429,000; last week's initial claims revised up to 420,000 from 414,000. Four week moving average on initial claims is 426,250. But there was a higher-than-expected lack of reporting, so there could be big revisions next week either way.

CFNAI MA3 weakening still. June would have to be quite positive to stop the slide in this number.

Tomorrow Q1 GDP final. It looks like Q2 is going to be worse than Q1. New Home Sales later today, but why bother? It's the same old, same old bouncing on the bottom. It ain't gonna get no worse because it can't, and it doesn't seem to be able to get much better due to competition from existing home sales. Next year in Jerusalem, folks. On condos, these supply figures can't be trusted either on existing or new, because there is a lot of inventory out there that shifts from rental to sale and back in some areas.

Asia greeted the downward revisions for projected US GDP with some dismay, and commodities trading turned quite negative. Chinese prelim PMI was reported about at "stall", so that is not helping the situation, money is moving into the risk currencies like the yen, the Swiss franc, and yes, the good 'ol USD. Perhaps the ECB should have laid less stress on "risk" yesterday. The Germans are rounding up investors and having a little meeting about "voluntary" rollovers. "Zo, Hans, Ve haf vays to obtain your cooperation ..." These meetings are completely confidential.

The brightest news out there is that TEPCO has perhaps found the problem with the water filtration system and may be able to fix it. One story. Another story. Who knows? Maybe today they'll get it working, maybe not, because this more detailed story doesn't sound quite right when read with the other two.

Let's see - the Sniffies (do you realize that we fund this stuff?) are crusading against potato chips and French fries. The Ivy Medical Sniffies appear to be chasing well-paid irrelevance - just think what a tremendous help this will be to all the doctors out there who up till now, were recommending a diet of potato chips and French fries for their patients who need to lose weight.

I had a good laugh over some of the oil articles. These are stocking levels:

Quite high, wouldn't you say? But even higher when one looks at consumption and capacity measures.

PS: On Meredith and munis:

Note: If it walks like a duck.....

European leading edge predictors don't look so hot. Germany is not in trouble, but there is growing wariness. Paradoxically, France is going to profit from the German decision to bag nuclear power so its economic growth trend should be adjusted upward. IEA's oil moves may not help Europe much.

CFNAI MA3 weakening still. June would have to be quite positive to stop the slide in this number.

Tomorrow Q1 GDP final. It looks like Q2 is going to be worse than Q1. New Home Sales later today, but why bother? It's the same old, same old bouncing on the bottom. It ain't gonna get no worse because it can't, and it doesn't seem to be able to get much better due to competition from existing home sales. Next year in Jerusalem, folks. On condos, these supply figures can't be trusted either on existing or new, because there is a lot of inventory out there that shifts from rental to sale and back in some areas.

Asia greeted the downward revisions for projected US GDP with some dismay, and commodities trading turned quite negative. Chinese prelim PMI was reported about at "stall", so that is not helping the situation, money is moving into the risk currencies like the yen, the Swiss franc, and yes, the good 'ol USD. Perhaps the ECB should have laid less stress on "risk" yesterday. The Germans are rounding up investors and having a little meeting about "voluntary" rollovers. "Zo, Hans, Ve haf vays to obtain your cooperation ..." These meetings are completely confidential.

The brightest news out there is that TEPCO has perhaps found the problem with the water filtration system and may be able to fix it. One story. Another story. Who knows? Maybe today they'll get it working, maybe not, because this more detailed story doesn't sound quite right when read with the other two.

Let's see - the Sniffies (do you realize that we fund this stuff?) are crusading against potato chips and French fries. The Ivy Medical Sniffies appear to be chasing well-paid irrelevance - just think what a tremendous help this will be to all the doctors out there who up till now, were recommending a diet of potato chips and French fries for their patients who need to lose weight.

I had a good laugh over some of the oil articles. These are stocking levels:

Quite high, wouldn't you say? But even higher when one looks at consumption and capacity measures.

PS: On Meredith and munis:

U.S. state and local governments will need to raise taxes by $1,398 per household every year for the next 30 years if they are to fully fund their pension systems, a study released on Wednesday said.The details vary hugely per plan. Obviously the above figures are an estimate. Some plans are in far worse shape and some are in far better shape. One rule of thumb is to look at demographics (growing or not?). The blue state government workers are about to see their worst nightmare take flesh and stalk the legislatures. This is why I posted all that stuff about the NJ plan, which cuts COLAs to eventually achieve a balance. There will be much more of these sorts of moves in many states, because many of these plans cannot be supported under any feasible scenario at all. This public pension bubble is very large indeed, but fortunately can be adjusted.

Note: If it walks like a duck.....

European leading edge predictors don't look so hot. Germany is not in trouble, but there is growing wariness. Paradoxically, France is going to profit from the German decision to bag nuclear power so its economic growth trend should be adjusted upward. IEA's oil moves may not help Europe much.

Wednesday, June 22, 2011

In Shock

I made the mistake of watching Gentle Ben's presser, and it will take days to recover. That was not a good experience.

I note that others seem unimpressed as well:

In the interests of Fed/public relations, I would like to offer some help to Ben about those confusing and frustrating slow recovery features. How about a fall in real earnings? The BLS puts out a series that the Fed might find very helpful known as "Real Earnings". The next release is scheduled for July 15th, and Ben might want to read it. As BLS notes in the narrative regarding all employees:

For production and non-supervisory employees on private nonfarm payrolls:

The moving parts here are nominal wages paid, CPI over the year, and most importantly, the average work week. Now let us turn to the ever-helpful St. Louis Fed Fred. Here I am going to just revolutionize modern economics nearly back to Adam Smith:

The economic moving parts we have been discussing pretty much are shown here.

The economic moving parts we have been discussing pretty much are shown here.

The strong orange line is CPI-W. The strong blue line (most variable) is Real Retail Sales.

The week red and green lines wages and salaries (not benefits) paid to private workers and government workers, and the line over the other weak line is of course government workers.

One thing Ben might want to note is the sudden bend up in CPI-W, which, oddly enough, almost seems to have something to do with the fall in real retail sales.

Now - revolutionizing ECONOMICS AZ WE KNOWZ IT:

This hyah is real retail sales level and the compounded annual rate of change for the private worker series shown in the above graph, adjusted by CPI.

'

Note that the private worker series ends before the retail sales series.

When contemplating this graph:

A) For a self-sustaining recovery, the red line must be above the blue line as an average for a while. Otherwise, workers are withdrawing from savings or borrowing to sustain spending. Both trends have an end; the correction on the borrowing-to-spend is inevitably worse, because when you stop spending your savings, all you do is cut spending to income levels. When you have been borrowing to spend, when you stop you have to cut spending to income levels less debt repayment. The way we entered the 2007 recession was that households got behind the income/spending ball in 2005, and for the next two years, households borrowed very large sums of money to sustain spending. Of course the more they borrowed the more they fell behind each month, so when the correction came it was rather brutal.

B) We achieved that the magic red-line-above-blue-line. Toward the end of the last quarter of 2010 we were getting close to the margin, but remember that in the last quarter you always have holiday spending - the big recovery in real wages over the previous eighteen months basically funded that. So there wasn't going to naturally be a big dip, just a correction in rate of change of spending. Note the highly positive shift in annual compounded rate of change of real wages and salaries preceded emergence from the recession in 2009. Funny how that happens.... In an income recession, that must happen. It had very little to do with the governmental stimulus, in all sincerity.

C) You might think the Jan-April blue line trend (retail) looks odd. It is odd, but it occurred that way because of the FICA give back (mostly went to the top 30% of earners) plus the sudden rise in cost of basic goods. Now that the rate of cost changes is disseminating from basics through the economy, even higher income households are having trouble sustaining spending. Because the lower 30-40% spend so little relative to the top 30%, no one ever notices or worries when they're shoved to the wall. Their plight is only noticed when the incomes of the top 30% get affected. This is inevitable. Unfortunately, this relative invisibility means that most Wall Street forecasters are doomed to fail, because they always get surprised when the inevitable happens.