MaxedOutMama

MaxedOutMama

Friday, September 30, 2011

And Now The TGIF Good News

The case for a slower, more restrained US downturn lies in two reports today, not to mention the hope for next year in housing. Chicago PMI (concentrates on heartland production) is PDG, and so is NACM.

Neither of these reports show anything that can prevent the US from entering a downturn - far too much of our economy is based on consumer spending at levels disassociated with increases in real incomes and government spending at levels disassociated with the levels of taxation that the real economy can bear without buckling. In short, our only long-term hope is to restructure.

Nonetheless, the relative strength in these two reports does suggest that there are some underlying positives that could limit the scope of a downturn and also tend to suggest that there is enough base-level strength in low financial costs and a slow reindustrialization to support a non-catastrophic restructuring.

We should not do the jobs thingie - we should look at the relative strengths we have and try to accentuate them. We probably should raise FICA withholding back to its normal level in 2012, restore and increase the MWP to $500 with all other terms left. This would represent a large tax increase on the higher income households, but they can stand it and the relative strength it would insert into the economy from the lower levels would greatly help.

The Euro crash will not last forever - trying to pretend unpayable sovereign debt will be paid is a parasite that will either kill its host or be killed. The situation cannot drag on for more than the middle of 2013, and as soon as it is resolved the US will come under fire.

We need to make sure we are strong enough at that time to reassure investors. I think we can pull it off if we just use some common sense. Common sense in an election year in the US is hard to come by, but perhaps we've suffered enough to fall back to something that will work.

So to our feckless president I would say "If you can't lead then follow, and if you can't follow then get out of the way."

2012 will be a tough year for the global economy, but price adjustments will happen and at the end of the year the situation will look different. It's up to us whether we are willing to put aside the fantasy phase of US politics and buckle down to achievable real-world progress.

Neither of these reports show anything that can prevent the US from entering a downturn - far too much of our economy is based on consumer spending at levels disassociated with increases in real incomes and government spending at levels disassociated with the levels of taxation that the real economy can bear without buckling. In short, our only long-term hope is to restructure.

Nonetheless, the relative strength in these two reports does suggest that there are some underlying positives that could limit the scope of a downturn and also tend to suggest that there is enough base-level strength in low financial costs and a slow reindustrialization to support a non-catastrophic restructuring.

We should not do the jobs thingie - we should look at the relative strengths we have and try to accentuate them. We probably should raise FICA withholding back to its normal level in 2012, restore and increase the MWP to $500 with all other terms left. This would represent a large tax increase on the higher income households, but they can stand it and the relative strength it would insert into the economy from the lower levels would greatly help.

The Euro crash will not last forever - trying to pretend unpayable sovereign debt will be paid is a parasite that will either kill its host or be killed. The situation cannot drag on for more than the middle of 2013, and as soon as it is resolved the US will come under fire.

We need to make sure we are strong enough at that time to reassure investors. I think we can pull it off if we just use some common sense. Common sense in an election year in the US is hard to come by, but perhaps we've suffered enough to fall back to something that will work.

So to our feckless president I would say "If you can't lead then follow, and if you can't follow then get out of the way."

2012 will be a tough year for the global economy, but price adjustments will happen and at the end of the year the situation will look different. It's up to us whether we are willing to put aside the fantasy phase of US politics and buckle down to achievable real-world progress.

With A Whimper?

Let's see: I stayed up late to catch the Markit PMIs for China and Japan. They weren't good. Chinese manufacturing is still in contraction with input price increases accelerating(!!!!) and Japanese manufacturing fell to 49.3 from 51.9 in August. The report notes weakness in Chinese orders as one of the causes of the fall in Japanese new orders. Japanese retail sales in August fell hard. Falling retail sales plus falling manufacturing presents a pretty difficult growth picture! So I then grumped my way off to bed.

This morning, I got a big fat stinking three-day-dead mackerel in the face in the form of Personal Income and Outlays for the US, which executed a real -0.3 negative for income on the month and a real 0.0 for Personal Consumption Expenditures (PCE) on the month. I thought from Treasury Receipts that nominal incomes (reported a 0.0) should be higher for August, although the high inflation is still cutting into real incomes. I will go back and look at receipts as soon as I have time. Maybe I missed something, but my first impulse is to say that this will be revised up (although still not to a real increase).

The preliminary benchmark revision for the establishment survey is out. This is still not real-time - it is picking up pulses from when the economy was stronger and employment was picking up in March - but it is certainly closer to current figures. This revision is deployed in February of 2012. See the release for more details.

Let's see - we have some other goodies here in the economic report grab bag. Eurozone inflation was reported to have jumped from 2.5% in August to 3.0% in September. This seems likely to delay any ECB move to cut rates, but most people think that the ECB will cut rates before the end of the year. It depends partly on inflation IMO. German retail sales were reported down 2.9% on the month. German unemployment keeps falling - it is currently below 7%!!!!! That's got to be the lowest since reunification. But Germans are experiencing increasing inflation, so it is reasonable perhaps that they are spending less in real terms. Unlike US retail sales, Germany reports inflation-adjusted retail sales.

The Euro is dropping and this may add to inflation. Normally you fight that with rate increases, not decreases. I think if I were the ECB I'd raise rates, because lower rates overall won't get through to the debt-troubled countries, and if the Euro drops more German unemployment will keep dropping, but everybody may just keep spending less. With a weakening market for exports, eventually that will tail off anyway. If you raise rates and cut inflation, there may be more spending oomph overall in the Eurozone. Just a thought. At this point a lower Euro is helping economies like Germany's, but it will over time still feed consumer inflation.

I think Germany's current fall in retail is cyclical and highly related to heating oil purchases for winter. So I expect this to improve later in the year. Or do I just hope for change? Well, anyway I expect the first shock to wear off and more Germans to hit the stores by November.

New Zealand got downgraded. This will not shake world markets. However the blinding fall in coffee on commodity markets shows what kind of downdraft we can expect in pricing. Part of the reason for the fall were reports that warehousing for green beans was quite well stocked indeed, and harvests were looking pretty good. But the truth is that earlier in the year no one cared about these stats, and now they do, which shows a change in trading methodology. These sorts of shifts generally last for at least six months, so risks are on the downside for all such commodities.

I also believe that while prices will adjust, they will not adjust quickly. There is too much money out there looking for a home, and with the equity markets doing poorly, especially in Asia, there is no other home. Therefore we are still not in a trading economy at which prices are adjusting on trade flows and supply, but rather still in a financial economy at which prices are adjusting for changes in money flows and supply. Given the choice of accepting a negative real rate of return on bonds and being chained to the fate of one currency, accepting a possible negative real rate of return with the option of being able to shift currencies smoothly still makes commodities look somewhat appealing even with high downside risks. Personally I would not do this, but I think producers will continue to stockpile supplies and so there is some near-term support for use commodities.

Such trading schemes generally produce nasty, sudden disruptive adjustments that hurt real trading of goods, so I expect the current sorrowful trend to continue. I also think that trading in such commodities has a much higher downside risk than the market believes. Oil now has no real support at almost any price level; I don't THINK it will go much below $45, but it could. It could go below $20 in a year, and that's more than a 5% probability. It all depends on how fast the global economy can adjust. I do think we have some slow adjustments in order for a while, because oil has a high psychic comfort level at this point. Note that abruptly the high copper stockpiles have emerged as a pricing factor; this is an example of the same evolution.

I do not think the Chinese manufacturing figures are quite as bad as they seem. As far as I can tell, Chinese manufacturing output is being dragged down by the inability to finance large buys of input costs. So manufacturers have shifted toward caution and lower output levels in order to try to retain the ability to finance new production runs on received orders. This does imply that there is further trouble ahead. I have to believe that part of the problem is construction and development companies that are borrowing money in the 15-25% range. This surely must shut out a lot of self-financed industrial investment!

This morning, I got a big fat stinking three-day-dead mackerel in the face in the form of Personal Income and Outlays for the US, which executed a real -0.3 negative for income on the month and a real 0.0 for Personal Consumption Expenditures (PCE) on the month. I thought from Treasury Receipts that nominal incomes (reported a 0.0) should be higher for August, although the high inflation is still cutting into real incomes. I will go back and look at receipts as soon as I have time. Maybe I missed something, but my first impulse is to say that this will be revised up (although still not to a real increase).

The preliminary benchmark revision for the establishment survey is out. This is still not real-time - it is picking up pulses from when the economy was stronger and employment was picking up in March - but it is certainly closer to current figures. This revision is deployed in February of 2012. See the release for more details.

Let's see - we have some other goodies here in the economic report grab bag. Eurozone inflation was reported to have jumped from 2.5% in August to 3.0% in September. This seems likely to delay any ECB move to cut rates, but most people think that the ECB will cut rates before the end of the year. It depends partly on inflation IMO. German retail sales were reported down 2.9% on the month. German unemployment keeps falling - it is currently below 7%!!!!! That's got to be the lowest since reunification. But Germans are experiencing increasing inflation, so it is reasonable perhaps that they are spending less in real terms. Unlike US retail sales, Germany reports inflation-adjusted retail sales.

The Euro is dropping and this may add to inflation. Normally you fight that with rate increases, not decreases. I think if I were the ECB I'd raise rates, because lower rates overall won't get through to the debt-troubled countries, and if the Euro drops more German unemployment will keep dropping, but everybody may just keep spending less. With a weakening market for exports, eventually that will tail off anyway. If you raise rates and cut inflation, there may be more spending oomph overall in the Eurozone. Just a thought. At this point a lower Euro is helping economies like Germany's, but it will over time still feed consumer inflation.

I think Germany's current fall in retail is cyclical and highly related to heating oil purchases for winter. So I expect this to improve later in the year. Or do I just hope for change? Well, anyway I expect the first shock to wear off and more Germans to hit the stores by November.

New Zealand got downgraded. This will not shake world markets. However the blinding fall in coffee on commodity markets shows what kind of downdraft we can expect in pricing. Part of the reason for the fall were reports that warehousing for green beans was quite well stocked indeed, and harvests were looking pretty good. But the truth is that earlier in the year no one cared about these stats, and now they do, which shows a change in trading methodology. These sorts of shifts generally last for at least six months, so risks are on the downside for all such commodities.

I also believe that while prices will adjust, they will not adjust quickly. There is too much money out there looking for a home, and with the equity markets doing poorly, especially in Asia, there is no other home. Therefore we are still not in a trading economy at which prices are adjusting on trade flows and supply, but rather still in a financial economy at which prices are adjusting for changes in money flows and supply. Given the choice of accepting a negative real rate of return on bonds and being chained to the fate of one currency, accepting a possible negative real rate of return with the option of being able to shift currencies smoothly still makes commodities look somewhat appealing even with high downside risks. Personally I would not do this, but I think producers will continue to stockpile supplies and so there is some near-term support for use commodities.

Such trading schemes generally produce nasty, sudden disruptive adjustments that hurt real trading of goods, so I expect the current sorrowful trend to continue. I also think that trading in such commodities has a much higher downside risk than the market believes. Oil now has no real support at almost any price level; I don't THINK it will go much below $45, but it could. It could go below $20 in a year, and that's more than a 5% probability. It all depends on how fast the global economy can adjust. I do think we have some slow adjustments in order for a while, because oil has a high psychic comfort level at this point. Note that abruptly the high copper stockpiles have emerged as a pricing factor; this is an example of the same evolution.

I do not think the Chinese manufacturing figures are quite as bad as they seem. As far as I can tell, Chinese manufacturing output is being dragged down by the inability to finance large buys of input costs. So manufacturers have shifted toward caution and lower output levels in order to try to retain the ability to finance new production runs on received orders. This does imply that there is further trouble ahead. I have to believe that part of the problem is construction and development companies that are borrowing money in the 15-25% range. This surely must shut out a lot of self-financed industrial investment!

Thursday, September 29, 2011

I Think I'll Bother

Of late I have gotten really apathetic and depressed about pointing out the nonsense in many news reports, but this one was kind of over the top:

The important column is the "Current" Column. Very few of the mortgages exit via pay-off, although probably a lot are written down on short-sale or DIL - (most of rightmost column).

Now needless to say, as time rolls on more and more modified mortgages will default. For 2008, less than 29% of these mortgages are current or paid off. For mortgages modified in the first quarter of 2011, ONLY 77.7% are CURRENT. This is still an appallingly bad performance after at most five modified scheduled mortgage payments.

Beginning on page 5 you can see a breakdown of performance by 60 day delinquency rates at 3, 6, 9 and 12 months by year of modification, beginning with 2008 and ending with Q1 2011. The quality has improved overall, but still is pretty bad considering how much the payments have been dropped (see page 36 for 30 days plus after a year), but now delinquency rates on the overall mortgage portfolio have started rising again.

I really hate this report, because it seems to me that there are elements of dishonesty and, well, spin in the way the data is presented. I guess I'll write more on this tomorrow - I've shut up all these months, but I'm really irked now.

One in five homeowners whose mortgages were modified under a program aimed at reducing foreclosures defaulted again within a year after their payments were cut, the U.S. Comptroller of the Currency reported today.The report is OCC's Mortgage Metrics for Q2. A picture is worth a thousand words, so this chart from page 45 should be worth at least 500:

The important column is the "Current" Column. Very few of the mortgages exit via pay-off, although probably a lot are written down on short-sale or DIL - (most of rightmost column).

Now needless to say, as time rolls on more and more modified mortgages will default. For 2008, less than 29% of these mortgages are current or paid off. For mortgages modified in the first quarter of 2011, ONLY 77.7% are CURRENT. This is still an appallingly bad performance after at most five modified scheduled mortgage payments.

Beginning on page 5 you can see a breakdown of performance by 60 day delinquency rates at 3, 6, 9 and 12 months by year of modification, beginning with 2008 and ending with Q1 2011. The quality has improved overall, but still is pretty bad considering how much the payments have been dropped (see page 36 for 30 days plus after a year), but now delinquency rates on the overall mortgage portfolio have started rising again.

I really hate this report, because it seems to me that there are elements of dishonesty and, well, spin in the way the data is presented. I guess I'll write more on this tomorrow - I've shut up all these months, but I'm really irked now.

At This Point We're Just Looking To Slow The Bleeding

Markit Retail PMIs. Italy's still in deep, France is doing better, Germany's not really, Europe as a whole is falling more slowly. Because inflation is the problem, a slower pace of fall gives a chance for prices to come down. But Europe seems to be seeing increasing inflation rather than the alternative.

US initial claims are lower this week. Four-week average at 417K, but that isn't very encouraging for employment.

GDP Q2 reported at 1.3%. GDP Q3 ought to be at least 1.7-1.8%. We'll see. The US seems to be entering another few hard months based on the early store/services data I'm getting - but maybe this is just temporary based on BTS spending. A lot of households might be tight this month.

I think the US restructuring will take quite some time. It's focused on the states and localities at this point, but that will surely take another five-six years?

Census publishes estimates of state and local tax revenues. The numbers are not necessarily directly reflective of the economy, because tax increases abound, and on occasion in good times sales taxes and so forth will be cut. In particular, looking at the data through Q2, it's remarkable how much Q2 property tax revenue has risen in a few years. Needless to say it is not because of massive building or value increases; it's because of higher millage rates. In most states, when the value of the property goes down, the locality just increases property tax rates. Home values are reported by Case-Shiller to be back at 2003/2004 levels. In Q2 2004, property tax receipts were 61,509. In Q2 2011, property tax receipts were 88,518. In Q2 2001, property tax receipts were 51,249. Call me Ishmael, but I don't see how this is not creating a further impact for would-be homebuyers in some areas.

I was flipping through Zillow looking at their estimates, and in some of the high-tax areas, you get properties with an estimated total housing payment composed 70% of property taxes. This is reaching the breaking point, surely?

US initial claims are lower this week. Four-week average at 417K, but that isn't very encouraging for employment.

GDP Q2 reported at 1.3%. GDP Q3 ought to be at least 1.7-1.8%. We'll see. The US seems to be entering another few hard months based on the early store/services data I'm getting - but maybe this is just temporary based on BTS spending. A lot of households might be tight this month.

I think the US restructuring will take quite some time. It's focused on the states and localities at this point, but that will surely take another five-six years?

Census publishes estimates of state and local tax revenues. The numbers are not necessarily directly reflective of the economy, because tax increases abound, and on occasion in good times sales taxes and so forth will be cut. In particular, looking at the data through Q2, it's remarkable how much Q2 property tax revenue has risen in a few years. Needless to say it is not because of massive building or value increases; it's because of higher millage rates. In most states, when the value of the property goes down, the locality just increases property tax rates. Home values are reported by Case-Shiller to be back at 2003/2004 levels. In Q2 2004, property tax receipts were 61,509. In Q2 2011, property tax receipts were 88,518. In Q2 2001, property tax receipts were 51,249. Call me Ishmael, but I don't see how this is not creating a further impact for would-be homebuyers in some areas.

I was flipping through Zillow looking at their estimates, and in some of the high-tax areas, you get properties with an estimated total housing payment composed 70% of property taxes. This is reaching the breaking point, surely?

Wednesday, September 28, 2011

An Ugly Landscape When You Look Up

Roubini said yesterday in some panel discussion or another that the US was already in contraction and most other developed economies were heading into one. On that chirpy note, we start our Wednesday with a raft of reports about the Euro problem. The longer they play with this Greek thing, the larger the eventual loss.

The UK is clearly thanking its stars that it never went Euro. German inflation is up again, and this is not going to fill the Bundesbank with optimism and the urge to send Euros elsewhere by assuming more debt. Schäuble's conflict with Geithner is of long standing (that link is from May), and the positions have hardened. Attempting to build a huge Euro bailout fund would in fact denigrate Germany's credit rating, so success appears impossible over a couple of years time frame.

My guess is that the Greek question will break very soon, although apparently they are now opting for a property tax. That may prove suicidal - it looks like everyone who can is bailing out of Greece, so the country is going to be left poor with no investment.

While currently the rate isn't that bad - maximum 16 Euro a square meter - the chance of it being raised is high as the economy gets worse. )One square meter is about 10.76 square feet, so a 1,100 sq ft dwelling would be taxed about 102 Euro, or around $140 USD.] Bad numbers - could be be up to $2,200 or so. If you confiscated all residential property in Greece you could just about clear up Greece's debt - that is, if you could turn the property into money. But you couldn't do that, because once the government starts confiscating property no one will buy property. So Greece is on its last legs. Whatever it can get from measures such as this might be sustainable (and certainly collectible), but ultimately it needs a big debt writedown to start rebuilding its economy.

US durable orders for August looked good. There was a slight drop in new orders, but when you look at things a bit more deeply, most of the summer pop was in response to the clearing of the Japanese supply line block. Still, capital goods and machinery show that the US manufacturing recovery is still creeping along. At this pace, it is not enough to overcome the immense consumer drag, and it is still dependent on external sales for support. Any minor change in housing investment on the positive side will add a big relative boost.

Most of the basic economic flux (aside from the issue of government policy) derives from uncertainty about the pace of auto sales in the next year.

So I am marginally more comfortable with US prospects. I think we are in a recession, but it is a restructuring recession and not a cartwheeling-into-the-abyss recession. Unfortunately commodity prices will have a huge effect on the US economic trajectory over the next year. We have to get to the point at which real incomes for the bulk of working people aren't declining.

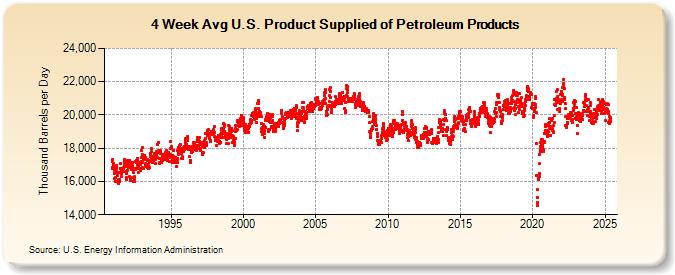

Note: Petroleum:

On a YTD YoY basis, petroleum products supplied are -0.7%, gas is -1.1%, and total imports are -10.2%, compared to a 4-week MA of -1.8% for products supplied, gas at -2.4%, and total imports at -12.3%. Current crude inventories are just above the average range for this time of year, so supply is good. Gas supplies are above the upper limit of the average range, and diesel supplies are near the upper limit of the average range. The average range is a five-year construct, so that is good strong supply, considering that total petroleum products supplied have been down consistently for years:

Nonetheless I think you will see petroleum prices only walk down, because there is just too much money out there chasing too few investment vehicles. I find it impossible to look at this graph and claim that we are not in recession. Unfortunately it is not just us, so I really wonder what Q1 of 2012 will look like globally. The global economic environment isn't going to get any better for a while.

The UK is clearly thanking its stars that it never went Euro. German inflation is up again, and this is not going to fill the Bundesbank with optimism and the urge to send Euros elsewhere by assuming more debt. Schäuble's conflict with Geithner is of long standing (that link is from May), and the positions have hardened. Attempting to build a huge Euro bailout fund would in fact denigrate Germany's credit rating, so success appears impossible over a couple of years time frame.

My guess is that the Greek question will break very soon, although apparently they are now opting for a property tax. That may prove suicidal - it looks like everyone who can is bailing out of Greece, so the country is going to be left poor with no investment.

While currently the rate isn't that bad - maximum 16 Euro a square meter - the chance of it being raised is high as the economy gets worse. )One square meter is about 10.76 square feet, so a 1,100 sq ft dwelling would be taxed about 102 Euro, or around $140 USD.] Bad numbers - could be be up to $2,200 or so. If you confiscated all residential property in Greece you could just about clear up Greece's debt - that is, if you could turn the property into money. But you couldn't do that, because once the government starts confiscating property no one will buy property. So Greece is on its last legs. Whatever it can get from measures such as this might be sustainable (and certainly collectible), but ultimately it needs a big debt writedown to start rebuilding its economy.

US durable orders for August looked good. There was a slight drop in new orders, but when you look at things a bit more deeply, most of the summer pop was in response to the clearing of the Japanese supply line block. Still, capital goods and machinery show that the US manufacturing recovery is still creeping along. At this pace, it is not enough to overcome the immense consumer drag, and it is still dependent on external sales for support. Any minor change in housing investment on the positive side will add a big relative boost.

Most of the basic economic flux (aside from the issue of government policy) derives from uncertainty about the pace of auto sales in the next year.

So I am marginally more comfortable with US prospects. I think we are in a recession, but it is a restructuring recession and not a cartwheeling-into-the-abyss recession. Unfortunately commodity prices will have a huge effect on the US economic trajectory over the next year. We have to get to the point at which real incomes for the bulk of working people aren't declining.

Note: Petroleum:

On a YTD YoY basis, petroleum products supplied are -0.7%, gas is -1.1%, and total imports are -10.2%, compared to a 4-week MA of -1.8% for products supplied, gas at -2.4%, and total imports at -12.3%. Current crude inventories are just above the average range for this time of year, so supply is good. Gas supplies are above the upper limit of the average range, and diesel supplies are near the upper limit of the average range. The average range is a five-year construct, so that is good strong supply, considering that total petroleum products supplied have been down consistently for years:

Nonetheless I think you will see petroleum prices only walk down, because there is just too much money out there chasing too few investment vehicles. I find it impossible to look at this graph and claim that we are not in recession. Unfortunately it is not just us, so I really wonder what Q1 of 2012 will look like globally. The global economic environment isn't going to get any better for a while.

Monday, September 26, 2011

Lalalalalalaaaaa

What can one do but party hearty? The Chief keeps walking around making comments about "putting on your marching shoes" and advises me to "stop complaining". I'm glad he's getting a charge out of this, because I am less than amused.

There's an article up on Drudge about the AMA, ObamaCare and actual doctors. SuperDoc quit the AMA in disgust years ago. The article is fine as far as it goes, but it doesn't go far enough.

In 2012, Medicare physician reimbursements are scheduled to drop 29.5%. The final rule is due November 1st, but the proposed rule gives a good feel for what this is going to cost doctors. That's 176 pages and hard going, so try this short article to get a feel for things. Excerpt chart:

Needless to say this sort of thing provokes either limitations on patients seen or cost-shifting to other patients.

Paying $16.53 for an X-ray is a bit ridiculous, don't you think?

SuperDoc is going to make about $48 per office visit on Medicare patients in 2012. This is not enough to keep the lights on (older patients are far more complex to deal with, require more time spent with them, and require far more follow-up), and he may have to limit Medicare patients, because if you don't keep your non-gov/gov ratios up, you're dead. This causes him great agony, because he is already 70 (working six days a week) and he keeps wandering around woefully wondering who is going to care for these people, and then, evincing considerable angst and threatening to leave the country. He claims Australia is the best bet, but his wife is holding out for Canada.

But this is the first of many projected Medicare cuts under ObamaCare. Five years from now things are going to get much worse.

I don't think the average person realizes how the medical industry works. Aside from the fact that SuperDoc does a tremendous amount of research on each patient with complex conditions (and many of the elderly have complex conditions), the administrative staff often does hours of work behind the scenes to get the required testing and medications through.

SuperDoc maintains a list of doctors he likes and thinks highly of, and over the last few years I called some of them to find out what they were doing. Almost all of them are cutting the vast majority of Medicare patients out of their practices, because they just can't practice quality medicine any more. The bitch of it is that many of the elderly respond superbly to good medical care (ultimately SuperDoc's way of practicing medicine is cheap), so that by shunting these people into practices that provide a much lower standard of care, we are probably costing the system a lot more.

Another problem is that as our arsenal of weapons against various conditions grows, the interactions between the weapons and the living being grow ever more complex. Without carefully balancing out risk factors, the risk of doing real damage to the patient grows. SuperDoc and I have been working on a project to apply some of the P-Nat risk-mapping techniques in the medical field, and so far it is promising. But I am also finding it terrifying, because he'll hand me a medication or condition to analyze, and I keep coming up with these risk holes (if you don't pay attention to them you run a very high risk of harming the patient), and then I take this stuff and the data back to SuperDoc and he gets very excited and tells me it is right.

If SuperDoc is correct, then medicine has reached a point at which it must learn to manage complexity in a different way and at an individual level. There seems no hope of doing that with the direction our current system is taking. The other "good" doctors I have spoken to all reiterated one of SuperDoc's worries - that they were seeing a high incidence of what they regarded as malpractice by specialists, due to a failure to take into account all the patient's conditions.

It seems pretty obvious that assessing general risk is going to be important in delivering workable medical care, and I don't see how we can do it on our current path. You can't defund primary care and basic diagnostics without fubaring the whole darned thing. Also we have to be realistic about the costs of medical care for the non-governmentally covered patients - these costs are going to show up in medical care costs for 40 year-olds, and that is neither fair nor sustainable.

There's an article up on Drudge about the AMA, ObamaCare and actual doctors. SuperDoc quit the AMA in disgust years ago. The article is fine as far as it goes, but it doesn't go far enough.

In 2012, Medicare physician reimbursements are scheduled to drop 29.5%. The final rule is due November 1st, but the proposed rule gives a good feel for what this is going to cost doctors. That's 176 pages and hard going, so try this short article to get a feel for things. Excerpt chart:

Needless to say this sort of thing provokes either limitations on patients seen or cost-shifting to other patients.

Paying $16.53 for an X-ray is a bit ridiculous, don't you think?

SuperDoc is going to make about $48 per office visit on Medicare patients in 2012. This is not enough to keep the lights on (older patients are far more complex to deal with, require more time spent with them, and require far more follow-up), and he may have to limit Medicare patients, because if you don't keep your non-gov/gov ratios up, you're dead. This causes him great agony, because he is already 70 (working six days a week) and he keeps wandering around woefully wondering who is going to care for these people, and then, evincing considerable angst and threatening to leave the country. He claims Australia is the best bet, but his wife is holding out for Canada.

But this is the first of many projected Medicare cuts under ObamaCare. Five years from now things are going to get much worse.

I don't think the average person realizes how the medical industry works. Aside from the fact that SuperDoc does a tremendous amount of research on each patient with complex conditions (and many of the elderly have complex conditions), the administrative staff often does hours of work behind the scenes to get the required testing and medications through.

SuperDoc maintains a list of doctors he likes and thinks highly of, and over the last few years I called some of them to find out what they were doing. Almost all of them are cutting the vast majority of Medicare patients out of their practices, because they just can't practice quality medicine any more. The bitch of it is that many of the elderly respond superbly to good medical care (ultimately SuperDoc's way of practicing medicine is cheap), so that by shunting these people into practices that provide a much lower standard of care, we are probably costing the system a lot more.

Another problem is that as our arsenal of weapons against various conditions grows, the interactions between the weapons and the living being grow ever more complex. Without carefully balancing out risk factors, the risk of doing real damage to the patient grows. SuperDoc and I have been working on a project to apply some of the P-Nat risk-mapping techniques in the medical field, and so far it is promising. But I am also finding it terrifying, because he'll hand me a medication or condition to analyze, and I keep coming up with these risk holes (if you don't pay attention to them you run a very high risk of harming the patient), and then I take this stuff and the data back to SuperDoc and he gets very excited and tells me it is right.

If SuperDoc is correct, then medicine has reached a point at which it must learn to manage complexity in a different way and at an individual level. There seems no hope of doing that with the direction our current system is taking. The other "good" doctors I have spoken to all reiterated one of SuperDoc's worries - that they were seeing a high incidence of what they regarded as malpractice by specialists, due to a failure to take into account all the patient's conditions.

It seems pretty obvious that assessing general risk is going to be important in delivering workable medical care, and I don't see how we can do it on our current path. You can't defund primary care and basic diagnostics without fubaring the whole darned thing. Also we have to be realistic about the costs of medical care for the non-governmentally covered patients - these costs are going to show up in medical care costs for 40 year-olds, and that is neither fair nor sustainable.

Hah, Numbers, Meaning, Punt

It kind of bugs me that the press keeps reporting numbers without statistical significance as if they mean anything.

New Home sales:

The August monthly change and the YoY change are so far below statistical significance that it is not worthwhile thinking about the numbers. The monthly is negative and the YoY is a larger 6.1% positive, but the 90% confidence range on the YoY is 18.8%, so just ignore it and throw it in the "nothing happening here" bucket.

The only number on this report that has statistical significance is the YTD YoY comparison, which is unfortunately negative at -8.3%, but this is influenced by housing credits, so again, ignoring it is the wisest course. The 90% confidence interval on that is +/- 4.4%. However revisions over the summer have been up, and this can be viewed as a moderately positive sign. When series like this drop out of statistical significance, I place more weight on revisions patterns than the numbers themselves.

Both median and average sales prices were down in August, but I think this is a mix effect. Not that I don't believe home prices are still dropping, but the new homes being built are mostly smaller and more modestly constructed, and as the older ones move off the market it is inevitable that offerings will shift downward in price.

CFNAI-MA3 for August came in at -0.28, which leaves June, July and August all below the -0.25 line. Monthly for August was -0.43. In March/April we took the big hit - the March monthly was +0.43 and then April was -0.84. Since then we seem to have marked out a new negative plateau, but unfortunately it is probably not permanent. At these levels, CFNAI-MA3 is consistent with either slow economic growth or the beginnings of recession.

The bummer about this is that it occurred during the period when we had something of production rebound due to clearing of the Japanese supply line blockages. So from here on we get more of "pace" effect in this stat, and it probably isn't going to look that good. I'm not looking forward to this index next February.

On Thursday we get the GDP revision (maybe up a notch or two) and on Friday we get Chicago PMI. There's housing chaff in the interim, none of which really is going to make a difference. Wednesday we have durable goods orders, and I do want to see that one.

If you are wondering about the equivocal nature of CFNAI, look at this graph:

IMO, it's got "double dip" written all over it.

The MI Consumer Confidence is not an emotional reading - according to the retail reports, it's because people are spending more for necessities and constraining spending on stuff like pharmaceuticals, not to mention eating out, electronics, etc.

I just got back from the cardiac hospital, where the Chief got the coveted "Most likely to live if continues good behavior" award, and I have to head out again. So see you later.

PS: Of all the potential presidential candidates, I like Herman Cain the best. Take a look at his 9-9-9 plan. I have some issues with it, but this type of thinking is necessary if we are to have a chance of escaping pure economic ugliness. We are forced to restructure or stay in our death spiral. History says that restructuring can work, but we have to start moving on it quickly. I wish Obama were more economically literate, but by now it is clear that he isn't and has no intention of studying.

New Home sales:

The August monthly change and the YoY change are so far below statistical significance that it is not worthwhile thinking about the numbers. The monthly is negative and the YoY is a larger 6.1% positive, but the 90% confidence range on the YoY is 18.8%, so just ignore it and throw it in the "nothing happening here" bucket.

The only number on this report that has statistical significance is the YTD YoY comparison, which is unfortunately negative at -8.3%, but this is influenced by housing credits, so again, ignoring it is the wisest course. The 90% confidence interval on that is +/- 4.4%. However revisions over the summer have been up, and this can be viewed as a moderately positive sign. When series like this drop out of statistical significance, I place more weight on revisions patterns than the numbers themselves.

Both median and average sales prices were down in August, but I think this is a mix effect. Not that I don't believe home prices are still dropping, but the new homes being built are mostly smaller and more modestly constructed, and as the older ones move off the market it is inevitable that offerings will shift downward in price.

CFNAI-MA3 for August came in at -0.28, which leaves June, July and August all below the -0.25 line. Monthly for August was -0.43. In March/April we took the big hit - the March monthly was +0.43 and then April was -0.84. Since then we seem to have marked out a new negative plateau, but unfortunately it is probably not permanent. At these levels, CFNAI-MA3 is consistent with either slow economic growth or the beginnings of recession.

The bummer about this is that it occurred during the period when we had something of production rebound due to clearing of the Japanese supply line blockages. So from here on we get more of "pace" effect in this stat, and it probably isn't going to look that good. I'm not looking forward to this index next February.

On Thursday we get the GDP revision (maybe up a notch or two) and on Friday we get Chicago PMI. There's housing chaff in the interim, none of which really is going to make a difference. Wednesday we have durable goods orders, and I do want to see that one.

If you are wondering about the equivocal nature of CFNAI, look at this graph:

IMO, it's got "double dip" written all over it.

The MI Consumer Confidence is not an emotional reading - according to the retail reports, it's because people are spending more for necessities and constraining spending on stuff like pharmaceuticals, not to mention eating out, electronics, etc.

I just got back from the cardiac hospital, where the Chief got the coveted "Most likely to live if continues good behavior" award, and I have to head out again. So see you later.

PS: Of all the potential presidential candidates, I like Herman Cain the best. Take a look at his 9-9-9 plan. I have some issues with it, but this type of thinking is necessary if we are to have a chance of escaping pure economic ugliness. We are forced to restructure or stay in our death spiral. History says that restructuring can work, but we have to start moving on it quickly. I wish Obama were more economically literate, but by now it is clear that he isn't and has no intention of studying.

Saturday, September 24, 2011

CBO Testimony About Budget Options

Worth a read!

Thus, according to CBO’s projections under current law, even with the new constraints on discretionary spending, federal spending excluding net interest will grow to 19.9 percent of GDP in 2021—compared with the 40-year average of 18.6 percent. And the composition of that spending will be noticeably different from what the nation has experienced in recent decades: Spending for Social Security and the major health care programs will be much higher, and spending for all other federal programs and activities, except for net interest payments, will be much lower. Alternatively, if the laws governing Social Security and the major health care programs were unchanged, and all other programs were operated in line with their average relationship to the size of the economy during the past 40 years, total federal spending excluding net interest would be much higher in 2021—nearly 24 percent of GDP. That amount exceeds the 40-year average for revenues as a share of GDP by nearly 6 percentage points—even before interest payments on the debt have been included.SuperDoc has me doing research on various aspects of breast cancer, which is making me twitch. Thus, I find reading such as the above less troublesome in contrast. This may not be true for all, so if you are having a good weekend you might want to postpone that link until Monday!

Friday, September 23, 2011

CA Unemployment Is At 12.1% - What Does It Mean?

And August CA state sales and use taxes were substantially below 2010's (7%), as were the July/August figures. It's hard to raise revenue in this environment.

For comparison, look at GA. Its economy is hurting, yet sales tax collections are still eking out a rise. One thing I always look at is the alcohol tax receipts - they tend to flag turns in state economies. Both are dropping YoY.

I have the sense that we are committing an eerie reprise of 2008, with a somewhat lesser amplitude but following a very similar curve. Last time we were crashing in from inflation-cut real incomes and the effects of cutting off the circulation of money gained from unsustainable private debt increases. This time we are folding up from inflation-cut real incomes and the effects of cutting off the circulation of money gained from unsustainable public debt increases. The more things change....

This year the 2007/2008 cycle is collapsed into one year.

There's a lot of talk about losses in government jobs, but look at the longer time sequence:

This is total private. As you can see, the number of private jobs is below where it was 10 years ago, not to mention 2007.

And here we have government jobs.

Relative to private jobs, government jobs are still far above the number a decade ago, and just about where they were in 2007.

Clearly the government sector cannot keep growing at the expense of the private sector - something is going to give. And it will give soon, because the revenues aren't there and now the really big government expenses for government retirees kick in.

The numbers:

From Table 2.1 we can add in another piece of the load the economy must carry, and that's government social benefits to persons. In Q2 2001 those amounted to 1,134.6 versus total wages and salaries of 4,961.4. In Q2 2011 these amounted to 2,308.6 versus total wages and salaries of 6,658.4. Respective ratios of 22.9% and 34.7%. Thus our fiscal problems.

Inflation does not help the fundamental imbalance there, and it's the big one. Also not included are all the unfunded expenditures, mostly in state and local, for government retirees. Very few of the systems accrued for retirement medical benefits, for example, and those must be paid out of current revenue each year.

People say we won't default on our debt, but I think we will. Inflation doesn't help the fundamental imbalance unless we cut benefits by not adjusting for inflation. People believe that we can inflate our way out of this, but we can't.

In that regard, we should remind ourselves that of all the government social benefits paid in 2011 Q2, Medicaid and Medicare amounted to significantly more (991.5) than the total of SS benefits (712.2). Note that these amounts are annualized on a seasonally adjusted basis. Clearly we would cut SS to nothing quite rapidly if we tried to compensate for medical increases by deflating SS payments. Also, Medicaid and Medicare benefits will become somewhat useless if reimbursements keep dropping - eventually, if the government doesn't pay for the service it will not be available. Further, let us not forget the greatly expanded Medicaid benefit and the new subsidy for private insurance that go into effect in 2014 under current law. These will make the picture far, far worse by 2017.

So we are going to default. How deeply we default depends on how quickly we can expand the private sector. And, to be realistic about it, a lot of that default may be inflicted on retirees, but most of it will hit the wealthier/comfortable retirees. Jimmy J. got uncomfortably close when he commented on a retirement income of 36K. By 2025 that may be about right.

For comparison, look at GA. Its economy is hurting, yet sales tax collections are still eking out a rise. One thing I always look at is the alcohol tax receipts - they tend to flag turns in state economies. Both are dropping YoY.

I have the sense that we are committing an eerie reprise of 2008, with a somewhat lesser amplitude but following a very similar curve. Last time we were crashing in from inflation-cut real incomes and the effects of cutting off the circulation of money gained from unsustainable private debt increases. This time we are folding up from inflation-cut real incomes and the effects of cutting off the circulation of money gained from unsustainable public debt increases. The more things change....

This year the 2007/2008 cycle is collapsed into one year.

There's a lot of talk about losses in government jobs, but look at the longer time sequence:

This is total private. As you can see, the number of private jobs is below where it was 10 years ago, not to mention 2007.

And here we have government jobs.

Relative to private jobs, government jobs are still far above the number a decade ago, and just about where they were in 2007.

Clearly the government sector cannot keep growing at the expense of the private sector - something is going to give. And it will give soon, because the revenues aren't there and now the really big government expenses for government retirees kick in.

The numbers:

2001 Aug:There's another way to look at this. Table 2.2B contains a breakdown of wage and salary disbursements so that you can get total government versus total private. In 2001 Q2, government wages and salaries were 815.4 vs private sector's 4,146.0, for a gov/private ratio of 19.7%. In 2011 Q2, it was 1,192.2 versus 5,466.2, for a gov/private ratio of 21.8%. These numbers do not accurately reflect relative costs; payments for benefits (retirement, insurance, etc) are recorded separately, and there government employees receive far more relatively.

Total private (nonfarm): 110,544,000

Total government: 21,218,000

Ratio gov/private: 19.2%

2011 Aug:

Total private (nonfarm): 109,170,000

Total government: 21,962,000

Ratio gov/private: 20.1%

From Table 2.1 we can add in another piece of the load the economy must carry, and that's government social benefits to persons. In Q2 2001 those amounted to 1,134.6 versus total wages and salaries of 4,961.4. In Q2 2011 these amounted to 2,308.6 versus total wages and salaries of 6,658.4. Respective ratios of 22.9% and 34.7%. Thus our fiscal problems.

Inflation does not help the fundamental imbalance there, and it's the big one. Also not included are all the unfunded expenditures, mostly in state and local, for government retirees. Very few of the systems accrued for retirement medical benefits, for example, and those must be paid out of current revenue each year.

People say we won't default on our debt, but I think we will. Inflation doesn't help the fundamental imbalance unless we cut benefits by not adjusting for inflation. People believe that we can inflate our way out of this, but we can't.

In that regard, we should remind ourselves that of all the government social benefits paid in 2011 Q2, Medicaid and Medicare amounted to significantly more (991.5) than the total of SS benefits (712.2). Note that these amounts are annualized on a seasonally adjusted basis. Clearly we would cut SS to nothing quite rapidly if we tried to compensate for medical increases by deflating SS payments. Also, Medicaid and Medicare benefits will become somewhat useless if reimbursements keep dropping - eventually, if the government doesn't pay for the service it will not be available. Further, let us not forget the greatly expanded Medicaid benefit and the new subsidy for private insurance that go into effect in 2014 under current law. These will make the picture far, far worse by 2017.

So we are going to default. How deeply we default depends on how quickly we can expand the private sector. And, to be realistic about it, a lot of that default may be inflicted on retirees, but most of it will hit the wealthier/comfortable retirees. Jimmy J. got uncomfortably close when he commented on a retirement income of 36K. By 2025 that may be about right.

Thursday, September 22, 2011

Twisted!!!

Because nothing says "I love you" like Japanese-style long rates.

Look at that 30-year, (she wrote reverently).

You can get the Treasury charting function here, but let me advise you not to try the longer terms at home. It was a true labor of love to get this. While I was waiting for the data to load, stars collided, galaxies were born, my dog nearly died of boredom and my patience almost ran out.

According to Treasury, the 30 year closed at 2.78% and the 10 year at 1.72%. The 7 year is at 1.24%. CPI-U is at 3.8%.

It will be interesting to see what happens. This is mostly produced by the combo of the bad economic news, especially the travails of Europe, reinforced by the Fed's announcement of Operation Twist. One can't feel confident about the economic trajectory we are seeing, and it is hard to imagine Italy's situation improving so the Euro angst is doomed to continue until it breaks into reality. That will happen within a year or two, and then Lord only knows what happens to Treasury rates.

You have to think there will be a wave of refinancings, although the net return for many will be low. For older people currently in good financial shape but with mortgages, the opportunity to refi into a 15 year at incredibly low rates might be enticing. With equity and good credit, 15 year rates should drop below 3%.

From my POV, this is a deflationary move. The rewards for saving money (or begging your parents for an equity handout) to qualify for loans at low rates are brilliant, but with rates so low underwriting criteria are surely going to tighten further. As rates fall,

rate risk increases and the relative percentage of loss risk rises, so underwriting criteria tend to tighten. It's hardly an easy money environment.

If that seems obtuse, let's consider FHA mortgage insurance premiums. Currently, the upfront premium is 1%. The annual premium varies according to downpayment and loan term.

Term > 15 years:BUT there's a kicker - if you have a 15 year term or less, and your Loan to Value ratio is under 90%, you don't have to pay any annual premium - just the one-time upfront 100 basis pts.

DP = or > 5%: 1.1% (110 basis pts)

DP < 5%: 1.15% (115 basis pts)

Term 15 years or less:

DP = or > 10%: 0.25% (25 basis pts)

DP < 10%: 0.50% (50 basis pts)

This raises interesting economic scenarios. For example, good mechanics are in short supply right now. A lot of skilled tradesmen could end up in far more decent economic shape in 10 years than the person who racked up a lot of debt for an expensive secondary education, even if that education paid off. Racking up a 40K-80K joint debt for a young couple has a lot of implications, whereas a young couple that is more stereotypically "working class" could save money, live at home for a few years, get married and buy a starter house with a good DP and a very low 15 year mortgage in many areas by the time they were in their mid 20s.

This is the reason I think we are going to emerge from this with an economy that looks much more like that of the 50s and than any time later.

Initial Claims, Unexpectedly

See, these babies unexpectedly rise or fall, depending on how you look at it, but there are too many of them no matter which way you look at it. Last week's figure was initially reported at 428K, which was revised up to 432K. This week's initial figure is 423K. The four-week moving average is now at 421K, up from last week's first-reported figure of 419,500.

Among the bummers here is that it is hard to get much of a drop of unemployment with claims in this range and indeed they are more consistent with increasing levels of unemployment. The 4 week MA for the comparable week in 2010 was only 37K more than this year's.

The 4-week MA for continuing claims was initially reported last week at 3,741,000. This week it is at 3,742,000, but through the magic of upward revisions that is reported as a slight decline. August 27 continuing claims were at 3,729,000. Although the damage is slight, the trend is bad and basically unaffordable with large companies tending to announce layoffs and declines in real average wages.

BLS reports 26 states plus DC having jobless rate increases in August, 12 having drops, and 12 with no change.

The FOMC announcement of Operation Twist (only) seems to have produced substantial selling fervor, most notably in oil. Further bank downgrades haven't helped Mr. Market develop the itch and the twitch in the buying finger. Gold prices are in sync downwards, completing the panic pattern. But the bad news is widespread at this point, with Europe in trouble, China sliding quietly down, India compromised, and many peripheral Asian economies seeing signs of a downward shift

The Fed could not notably improve matters by announcing QE3. It would drive asset prices up, but only temporarily. Mr. Market is quite capable of calibrating prices to spending power and maybe we'd just better let Mr. Market do his work for a while. The reason we are seeing the very strong global coordination is because prices have gotten out of sync with ability to consume (and therefore produce) at these prices. A price fix before the global downturn gets out of hand is the quickest medicine for this malady.

Note: The extent of the global contraction can best be seen in the PMIs, which have taken a remarkable turn for the worse over the last quarter. Markit's flash releases today only confirm the trend, with the Eurozone sliding into outright contraction, and France and Germany continuing expansions, but with declining trends and returns to levels last seen in the summer of 2009. Clearly, these Atlases will not continue to hold up the starry firmament of Euro prosperity. China does not enthuse either, although projections are for continued growth on growth in internal demand. These rates of internal expansion are causing continued inflation, which, if anything, appears to be still accelerating.

PS: The House voted down the spending authorization again. If you listen to the Dem talking points, this is a move by hidebound conservatives. But in fact, almost no Democrats voted for it and quite a few Republicans didn't, so the real picture is more complicated. However the fiscal year is almost over, and something has to be done by the end of September, so this is not going to soothe roiling markets. The debt limit is not a factor now, but spending authorizations (the US hasn't had a budget since the Dems took Congress in 2006) are a necessity also. US Treasury Debt to the Penny.

Further: Reuters article about the "unexpectedness" of the Eurozone PMI result.

Among the bummers here is that it is hard to get much of a drop of unemployment with claims in this range and indeed they are more consistent with increasing levels of unemployment. The 4 week MA for the comparable week in 2010 was only 37K more than this year's.

The 4-week MA for continuing claims was initially reported last week at 3,741,000. This week it is at 3,742,000, but through the magic of upward revisions that is reported as a slight decline. August 27 continuing claims were at 3,729,000. Although the damage is slight, the trend is bad and basically unaffordable with large companies tending to announce layoffs and declines in real average wages.

BLS reports 26 states plus DC having jobless rate increases in August, 12 having drops, and 12 with no change.

The FOMC announcement of Operation Twist (only) seems to have produced substantial selling fervor, most notably in oil. Further bank downgrades haven't helped Mr. Market develop the itch and the twitch in the buying finger. Gold prices are in sync downwards, completing the panic pattern. But the bad news is widespread at this point, with Europe in trouble, China sliding quietly down, India compromised, and many peripheral Asian economies seeing signs of a downward shift

The Fed could not notably improve matters by announcing QE3. It would drive asset prices up, but only temporarily. Mr. Market is quite capable of calibrating prices to spending power and maybe we'd just better let Mr. Market do his work for a while. The reason we are seeing the very strong global coordination is because prices have gotten out of sync with ability to consume (and therefore produce) at these prices. A price fix before the global downturn gets out of hand is the quickest medicine for this malady.

Note: The extent of the global contraction can best be seen in the PMIs, which have taken a remarkable turn for the worse over the last quarter. Markit's flash releases today only confirm the trend, with the Eurozone sliding into outright contraction, and France and Germany continuing expansions, but with declining trends and returns to levels last seen in the summer of 2009. Clearly, these Atlases will not continue to hold up the starry firmament of Euro prosperity. China does not enthuse either, although projections are for continued growth on growth in internal demand. These rates of internal expansion are causing continued inflation, which, if anything, appears to be still accelerating.

PS: The House voted down the spending authorization again. If you listen to the Dem talking points, this is a move by hidebound conservatives. But in fact, almost no Democrats voted for it and quite a few Republicans didn't, so the real picture is more complicated. However the fiscal year is almost over, and something has to be done by the end of September, so this is not going to soothe roiling markets. The debt limit is not a factor now, but spending authorizations (the US hasn't had a budget since the Dems took Congress in 2006) are a necessity also. US Treasury Debt to the Penny.

Further: Reuters article about the "unexpectedness" of the Eurozone PMI result.

Tuesday, September 20, 2011

Under Construction

I have another busy day ahead. Quick notes:

Parts of the new residential construction report are statistically significant, and parts aren't. Under construction is down from July, but not to a degree that's statistically significant. YoY is down 7.9%, and that is statistically significant. However the authorizations side offers more hope of some rebound off the bottom next year, with August authorizations up 7.8% YoY, which is most definitely statistically significant. So right now, we're not seeing economic boost, but the case for next year is more optimistic. One has to wonder what effect our current economic troubles will have on that, but with the pace of housing activity being so remarkably low viewed against history, it's not hard to argue that there is space for improvement.

Struggling for optimism, this Bloomberg article starts out by suggesting shipping companies could be helped by a last minute surge to restock if consumers all of a sudden start to spend like gangbusters for the holidays. I started snickering on the first paragraph with the comparisons to 2009 and the theory that retailers are just taking this terrible risk by understocking for the mad rush of consumers hellbent on spending their last dollar. Further in, the article gets more realistic:

I don't think retailers are taking a fearful risk. In 2009 we were months out of recession and real incomes were rebounding. Consumers with jobs felt a lot more confident about keeping them by the end of 2009, and having a bit of extra money, they spent it. That's the reason I posted all those graphs! Neither holds true this year:

Tomorrow we get existing home sales. I note in my driving around that there is tremendous inventory out there. If consumers want to buy a home and can qualify, they have plenty of options. It seems to me that the housing crash has diffused and spread to new areas and homes at higher price points. We'll see, but I am not that optimistic.

We also get the FOMC meeting announcement tomorrow, with the big bet being on Operation Twist (Fed shifting Treasury purchases to push long rates down). I don't think that will do much if any good, but I don't think it will do much harm either. Another round of quantative easing would produce another round of Main Street strangulation.

I do have some good news for you - we are not going to die from CO2 levels, the negative feedback effect from clouds is real, rather than the IPCC's assumed positive feedback. Of course, if you are truly a dedicated pessimist you can still work yourself up into a fit over this - you could assume that the sun's lower activity levels continue, that we go into a Maunder-type minimum, that CO2-engendered warming doesn't save us, that northern grain harvests fail and that the world endures another round of starvation-induced global warfare.

I am worried about the sun's lack of activity, but I would argue in mitigation that Maunder-type minimums seem to be somewhat rare, that aridity often goes along with cold spells, and that lower cloud formation might help the CO2 kick back in. Still, at this time it might be wise to stop burning the corn and stockpile it, just in case.

If you would - prayers for Carl of NOFP. He's had some severe health challenges and is facing another; he's in very real pain now. Pray for guidance for the doctors and Carl, and good healing.

Parts of the new residential construction report are statistically significant, and parts aren't. Under construction is down from July, but not to a degree that's statistically significant. YoY is down 7.9%, and that is statistically significant. However the authorizations side offers more hope of some rebound off the bottom next year, with August authorizations up 7.8% YoY, which is most definitely statistically significant. So right now, we're not seeing economic boost, but the case for next year is more optimistic. One has to wonder what effect our current economic troubles will have on that, but with the pace of housing activity being so remarkably low viewed against history, it's not hard to argue that there is space for improvement.

Struggling for optimism, this Bloomberg article starts out by suggesting shipping companies could be helped by a last minute surge to restock if consumers all of a sudden start to spend like gangbusters for the holidays. I started snickering on the first paragraph with the comparisons to 2009 and the theory that retailers are just taking this terrible risk by understocking for the mad rush of consumers hellbent on spending their last dollar. Further in, the article gets more realistic:

Shipping data currently show retailers preparing for a “muted” holiday season, Hartford said. The combined inbound- container volume at the Los Angeles and Long Beach ports fell 9.4 percent in August from a year earlier, following declines of 2.3 percent and 4.6 percent in July and June, according to Bloomberg data. These ports, the two largest in the U.S., account for about 40 percent of total imports, Hartford said.Heh. You read all that about the shipping at Snarky Mark's first.

I don't think retailers are taking a fearful risk. In 2009 we were months out of recession and real incomes were rebounding. Consumers with jobs felt a lot more confident about keeping them by the end of 2009, and having a bit of extra money, they spent it. That's the reason I posted all those graphs! Neither holds true this year:

Tomorrow we get existing home sales. I note in my driving around that there is tremendous inventory out there. If consumers want to buy a home and can qualify, they have plenty of options. It seems to me that the housing crash has diffused and spread to new areas and homes at higher price points. We'll see, but I am not that optimistic.

We also get the FOMC meeting announcement tomorrow, with the big bet being on Operation Twist (Fed shifting Treasury purchases to push long rates down). I don't think that will do much if any good, but I don't think it will do much harm either. Another round of quantative easing would produce another round of Main Street strangulation.

I do have some good news for you - we are not going to die from CO2 levels, the negative feedback effect from clouds is real, rather than the IPCC's assumed positive feedback. Of course, if you are truly a dedicated pessimist you can still work yourself up into a fit over this - you could assume that the sun's lower activity levels continue, that we go into a Maunder-type minimum, that CO2-engendered warming doesn't save us, that northern grain harvests fail and that the world endures another round of starvation-induced global warfare.

I am worried about the sun's lack of activity, but I would argue in mitigation that Maunder-type minimums seem to be somewhat rare, that aridity often goes along with cold spells, and that lower cloud formation might help the CO2 kick back in. Still, at this time it might be wise to stop burning the corn and stockpile it, just in case.

If you would - prayers for Carl of NOFP. He's had some severe health challenges and is facing another; he's in very real pain now. Pray for guidance for the doctors and Carl, and good healing.

Monday, September 19, 2011

Yikes - S&P, Italy,

Moody's was supposed to make a decision this fall, but S&P jumped in first. I understand their POV:

S&P said it lowered its outlook for Italy’s growth to a 0.7 percent annual average for 2011 to 2014, from a prior projection of 1.3 percent. “We believe the reduced pace of Italy’s economic activity to date will make the government’s revised fiscal targets difficult to achieve,” it saidThe reaction will be interesting. Outlook negative. I guess the Fed and ECB will huddle and throw some more dollars into the ring tomorrow. I wonder if this will come up in FOMC? You would think so.

BIS Quarterly Review Is Out

I always read these things, but right now they are particularly essential. Sept 19th issue. Even if you read nothing else, don't miss the brief recap of the events (only 13 pages). In particular, rates on junk corporate bonds escalated painfully. The syndicated loan feature is excellent from a risk standpoint also.

The article on trade sensitivity to real exchange rate changes provides something to discuss from a US standpoint. Low sensitivity to rate exchanges means that the real economy in a low IIT nation will experience high rates of economic drag (lower growth) when costs of imports rise. Applying this analysis to the tariff question and the wild inflation theory (just print money) shows up the limitations of US options:

There's a table with different assessments of the two measures by countries, and it explains why Greece is staggering along without already going to its own currency. The rewards for Greece of being able to print money in the short term are not great.

The article on trade sensitivity to real exchange rate changes provides something to discuss from a US standpoint. Low sensitivity to rate exchanges means that the real economy in a low IIT nation will experience high rates of economic drag (lower growth) when costs of imports rise. Applying this analysis to the tariff question and the wild inflation theory (just print money) shows up the limitations of US options:

Based on this intuition, the sensitivity of the trade balance to movements in real exchange rates should be much lower in a country with a low level of intra-industry trade (low IIT) than in a country with high IIT. Its imports are unlikely to fall significantly following a real exchange rate depreciation because no domestic industry can easily replace the imports that have become more expensive. Low IIT countries are typically those where raw materials or natural resources like oil account for a major share of imports. They could also be countries that have specialised in particular industries in order to benefit from a comparative advantage in some sectors. By contrast, imports fall much more in a high IIT country that depreciates its real exchange rate, as the country can more easily provide domestic substitutes for imports that have become more expensive. The sensitivity of the trade balance to the real exchange rate should therefore depend positively on IIT.The article also considers import content of exports (ICE). If exports have a high import content, it is not reasonable to assume that depreciating your currency will redress your trade deficit much. So IIT measures the degree of overlap between import and export products (0 IIT if a country imports just products A & B and exports just products C & D; 1 if a country imports products A, B, C & D and exports the same products), and ICE measures dependency of exports on imports.

There's a table with different assessments of the two measures by countries, and it explains why Greece is staggering along without already going to its own currency. The rewards for Greece of being able to print money in the short term are not great.

Sunday, September 18, 2011

My Answer Is No

I had to think it over for a few days before I reached the conclusion. Foxmark's comment on the previous post (containing the 3K question) sums up my thinking process:

The data here can be found at BLS CPS. This is another way of looking at the base of information in the graph in my prior post. First up, full-time median inflation adjusted wages (this excludes self-employed incorporated workers):

This bounces around a lot, and one of the reasons is inflation. Note that real median wages started to rise quite quickly at the end of 2008, coincident with the financial panic.

There is a time lag for higher real wages to feed through the economy, even when you have a rather dramatic move such as this. So the recession ended June 2009. Employment losses lag, of course.

In eleven years, we have made no progress on median real wages. Q2 2011 was $334 - Q2 2000 was $332.

The reason I knew that the Fed's QE2 program would be a disaster for the economy was that it was doomed to further drop real median and below wages, which had been declining slowly anyway. Of course the Fed error was exacerbated to some extent by the truly nutty "deal" reached by the Congress and President at the end of 2010, which raised federal taxes on the bottom 40% of wage earners. There is significant overlap between that bottom 40 percent and older households largely dependent on SS, but still that took the nominal damage to 45% of all households, and the inevitable inflation in base costs involved in the Fed's action took it right to 60%. From there it diffused upward.

And then we must not forgot the job losses. This graph is of fulltime workers:

So not only do we have declining median full-time wages, but we have a substantial employment problem. Rising costs, part-time work or no work. This graph gives me a headache and stomach cramps. I have a Zomig sitting right in front of me, and I may need it to get through this post.

In Q2 of 2000, we had 101,424,000 full time workers. In Q2 of 2011, we had 100,593,000 full time workers. Call me a pessimist, but given the growth in the population, I'd say we are missing a minimum of 6,000,000 full time jobs.

Filling in with part-time jobs obviously does something to household incomes. We have sustained an increase in part-time jobs, but in many circumstances this is a function of employers having leverage and using it to get the cheapest possible employees:

It's stunning to see how the end of the recession boosted part-time jobs, but not full-time jobs.

And it's not just teen-agers and young people. You can't really comprehend the damage we have sustained without looking at what I call the "core" rate of employment, which is workers 25 and over:

This graph is of the number of workers aged 25 and over who are employed full-time.

Remember, when BLS calculates real median weekly wages, it excludes part-time workers!

Shattering. You don't really need to go much further to comprehend why the housing market is so dead. The first-time purchase bracket was already exhausted from easy term lending, and since it has been eroded by the job market.