MaxedOutMama

MaxedOutMama

Wednesday, April 29, 2009

GDP AND Consequences

First, according to hard data such as rail and retail, the economy is getting worse rather than better in the first part of the second quarter. March was worse than Jan/Feb, and April is worse than March.

Second, there was an astounding drop in private domestic investment. Here's the recent history on gross private domestic investment:

06: +2.1%By recent quarter:

07: -5.4%

08: -6.7%

08 Q1: -05.8%; chained 2000 dollars: 1,754.7Since this is a fundamental economic driver, there ain't gonna be no real second half recovery. All subcategories were negative.

08 Q2: -11.5%; chained 2000 dollars: 1,702.0

08 Q3: +0.4%; chained 2000 dollars: 1,703.7

08 Q4: -23.0%; chained 2000 dollars: 1,596.0

09 Q1: -51.8%; chained 2000 dollars: 1,329.8

Third, government spending is declining. Total was -3.9% in Q1, and state and local was -3.8%.

To understand the implications, you have to look at three factors - quarterly change in GDP, change in real exports, and change in real domestic private investment compared to earlier downturns:

You should be able to view a larger version of this graph by clicking on the image. The data can be found here.

You should be able to view a larger version of this graph by clicking on the image. The data can be found here.This constellation of factors has not occurred since WWII. There was a worse collapse in domestic investment during the 75 debacle, but it was produced by an earlier and milder collapse in exports. We were also then a pretty big manufacturing economy. To have a coincident collapse in gross private domestic investment along with such a big collapse in exports implies that there is further weakness in domestic investment to come. Needless to say the global recession is not helping.

Further implications are that the futures price of crude oil is way too high. The stuff is piling up all over. US crude inventories this week are reported as being up YoY 12.3%, and YTD domestic product supplied has dropped 4.4% on a YTD basis. So we are not going to be sucking up the excess.

At this point I would say that a total 7-8% drop in GDP by trough is more likely than not. If we actually implement some of the wackier energy proposals, there could be reiterated downturns over a decade or so, and we could end up in 2019 with GDP over 10% lower than it is now. Seriously.

The stimulus bill never actually stuffed in much traditional stimulus. We are going to have to go back and revisit it. Still, it is too late to prevent the second half debacle for 09.

Other implications: China will have to devalue its currency after buying up all the natural resources it can get. It has no option; it must boost domestic social welfare spending, and it needs exports to sustain that effort. Right now it appears to be in more trouble than India.

The 10 year budget projections by both the White House and the CBO are ridiculously optimistic at this point.

Tuesday, April 28, 2009

Waiting For Stupendous Man

I spent some time on DU during my swine flu research. I wanted to see what the overall US reaction would be. DU may be a big forum, but it is quite atypical of the US at large. The number of purely maniacal threads on there (i.e. it's a CIA plot against Obama, it's a neocon plot, it's biowarfare) amounted to at least a hundred. There was a remarkably high noise-to-signal ratio. The population at large seems to be much calmer.

I just checked ol DU again, and somebody had posted a thread about Nazi ideology being founded on pragmatism. I guess if you ignore the dementia, that could be true. Somehow I would not describe someone searching for a bus route that will take them to center city so that they could use the death rays emitted by their eyes to destroy their enemies as being pragmatic, and that pretty much sums up Nazi ideology. It was doomed to fail. The shame is that ROW did not stop it before it took so many millions of lives.

I think that I had better stay off DU for sanity's sake.

But the rest of the world isn't much better. The one bright spot is that the CDC/state structure and the other public health initiatives set up to deal with a pandemic flu are working quite well. But of course, there has never been a way to stop a pandemic flu virus, so the success is limited. As of today, the virus is confirmed in seven countries.

It isn't time to panic yet, though. As long as they keep updating it, the time to panic will come when you see the upward rise on the CDC's MMWR (Mortality) compared to prior years. No one wants to get the flu, but it is not going to affect your life until there is enough of it around to generate deaths. Right now 09 mortalities are still low compared to 08.

It's also worth looking at MMWR Mortality to keep in perspective the reported deaths out of Mexico. Few Mexican cases have been confirmed (26 cases) - which is less than the confirmed caseload in the US. As for the death count, consider this. Mexico City is huge - it is comparable in size to New York City. In NYC, 08 weekly deaths from pneumonia/flu for the five preceding weeks (about the time the flu has been running in Mexico City) were in the 50s each week. So the expected death rate from pneumonia/flu in NYC for about 5 weeks prior would be somewhere around 220-275 in a normal year for this period. In a bad flu year, you'd expect to see considerably more deaths. There are yearly variations - this year, deaths have been running in the high 40s except for one pop to 61.

But still, if one is looking at the death count, I would expect to see far more pneumonia/flu deaths from a lethal pandemic virus than Mexico is reporting. For purposes of comparison, within the first month of the NYC 1918 flu epidemic more than 4,000 people died. Ninety years later we have a lot more firepower by way of medicine (especially antibiotics and antivirals) and medical technology, so deaths ought to be much less. But in a severe flu epidemic, Mexico City should be reporting at least 150 deaths per week after seven weeks. So it isn't severe. Not yet. It might become so, but right now heading toward the bomb shelter is a bit of an overreaction.

Aside from that one bright spot, isn't an awful lot of what's happening completely crazy? Take Waxman's description (on NPR, no less) of the pressing environmental danger he is seeking to avert with his plans to tax energy:

We're seeing the reality of a lot of the North Pole starting to evaporate, and we could get to a tipping point. Because if it evaporates to a certain point - they have lanes now where ships can go that couldn't ever sail through before. And if it gets to a point where it evaporates too much, there's a lot of tundra that's being held down by that ice cap.!!!! I just saw the flicker of Stupendous Man's red cape!!

If that gets released we'll have more carbon emissions and methane gas in our atmosphere than we have now.

There is, btw, a tremendously good and economically unassailable discussion by Peter Huber of the flaws of the "green economy" meme available at Mauldin's Outside The Box. I believe you will have to enter an email address to read this, but it is worth it:

Another argument commonly advanced is that getting over carbon will, nevertheless, be comparatively cheap, because it will get us over oil, too -- which will impoverish our enemies and save us a bundle at the Pentagon and the Department of Homeland Security. But uranium aside, the most economical substitute for oil is, in fact, electricity generated with coal. Cheap coal-fired electricity has been, is, and will continue to be a substitute for oil, or a substitute for natural gas, which can in turn substitute for oil. By sharply boosting the cost of coal electricity, the war on carbon will make us more dependent on oil, not less.It's comprehensive and sensible. The bottom line is that jacking up energy costs in the US is not going to change the global rise in carbon emissions, because countries that are very worried about their own internal economies cannot spare the energy to follow suit. For example, China proudly reported that they have implemented reforms cutting their environmental permits process from 60 to 5 days, and in some cases, 2 days as part of the economic stimulus program.

Which leaves US companies facing another severe competitive disadvantage, which shifts even more production to countries which use energy less efficiently, which overall, raises global carbon emissions. It also makes the US poorer, living less money left over for adaptation.

But if I look around, the picture becomes even more disturbing. It is natural for people to be somewhat upset about the swine flu. Very few of the public can have much perspective on the numbers, and we've all been warned about the dangers of a flu pandemic. Yet DU's flu performance, although most confounding and disturbing, looks remarkably sane compared to this NY Times editorial by Gregory Mankiw recommending achieving negative nominal interest rates (and real interest rates are already negative). He advances a remarkably bizarre suggestion to announce that the US will basically confiscate 1/10th of everyone's cash next year in order to overcome the reality that people will not lend money for negative interest rates.

I cannot write lucidly about this piece of epic insanity. I would need a whole lot of sedatives before I could attempt it. Or possibly an awful lot of really, really good sex.

Fortunately (since the Chief is away right now), I do not have to try to write lucidly about Mankiw's psychotic break with economic reality. Other people have noticed. Start with Robert Murphy's discussion of this editorial, and the disturbing academic mindset behind it:

Mankiw's article beautifully illustrates what is wrong with today's economics profession: it consists of very sharp guys (and gals) who can develop interesting models that spit out policy recommendations that would destroy the economy.Indeed. That's an understatement.

The problem is that we have theory without practice, and instead of responding to reality's corrections of our theoretical errors, we just keep coming up with wilder theories. That is what induced me to begin an extended meditation upon the Calvin & Hobbes cartoons. One thing about Calvin - he does not give up easily, and he always seems surprised by the predictable results.

Another few years of this, and the American people will be in the mood to kill all the environmentalists and the professors. Or at least fire the professors. I question whether having professors of economics is worthwhile any more.

Tuesday, April 21, 2009

I Digress

Take a look at Shrinkwrapped's post on the current AGW cant. The Shrink is responding to an odd but fashionable behavioral economics post claiming that Adam Smith's theories of a self-regulating marketplace are just all wrong. I always feel embarrassed to use a non-journalist's name when I am pointing out that someone's assertions are lunatic, so I won't cite the author's name. Instead, I will confer a charitable anonymity by using the sobriquet "Wonder Dummy" for the author henceforth.

The basic theme of Wonder Dummy's post:

Adam Smith first coined the term “The Invisible Hand” in his important book “The Wealth of Nations.” With this term he was trying to capture the idea that the marketplace would be self-regulating. The basic principle of the invisible hand is that though we may be unaware of it, an unseen hand is constantly prodding us along to act in line with what’s best for the whole economy. This means that when this invisible hand exists, when we all pursue our own interest, we end up promoting the public good, and often more effectively than if we had actually and directly intended to do so. This is a beautiful idea, but the question of course is how closely it represents reality.Of course the answer to the question is preordained by this careful miscast of Adam Smith's main assertion. That assertion is that economic efficiency is best for the economy, and that economic efficiency can best be attained by not interfering with prices in the marketplace. In fact, I suspect that Wonder Dummy has never read Adam Smith. I prefer to be charitable and assume that Wonder Dummy is not knowingly lying in order to lend credence to a meme that is currently popular, if completely wrong.

If you want to find out what Adam Smith (1723-1790) really said, you can find most of his writing online. Here is the overall page with links to his works online, and I recommend going directly to OnLine Library's Glasgow edition (7 vols). Volume I (link to Table of Contents) contains Smith's "The Theory of Moral Sentiments", which is an extended and realistic contemplation of what really motivates individuals and societal institutions. Adam Smith was no superficial thinker, and his economic musings were not based on an unrealistic view of mankind. Indeed, this quote from Section III, Chapter IV "Of the Nature of Self–deceit, and of the Origin and Use of general Rules" seems extremely apposite:

In order to pervert the rectitude of our own judgments concerning the propriety of our own conduct, it is not always necessary that the real and impartial spectator should be at a great distance. When he is at hand, when he is present, the violence and injustice of our own selfish passions are sometimes sufficient to induce the man within the breast to make a report very different from what the real circumstances of the case are capable of authorising.To which I must add, from a different section in context which I will leave the gentle reader to discover, my favorite Adam Smith quote:

What can be added to the happiness of the man who is in health, who is out of debt, and has a clear conscience?If you have never read Adam Smith's economic musings, I strongly recommend volume I and volume II of "An Inquiry into the Nature and Causes of the Wealth of Nations". But I digress. Coming back to the perturbed conclusions of Wonder Dummy:

In my mind this experience has taught us that Adam Smith ‘s version of invisible hand does not exist, but that a different version of the invisible hand that is very real, very active, and very dangerous if we don’t learn to recognize it. Perhaps a more accurate description of the invisible hand is that it represents human irrationality. In terms of irrationality the hand that guides our behavior is clearly invisible — after all recent events have demonstrated that we are largely blinded to the ways rationality plays in our lives and our institutions. Moreover it is also clear that irrationality does shape our behavior in many ways, pushing and prodding us along a path can lead to destruction. Whether we’re procrastinating on our medical check-ups, letting our emotions get the best of us, or letting conflicts of interest and short term time horizon ruin the financial market, irrationality is certainly involved.What a surprise. In fact, those who have actually read Adam Smith know that the "invisible hand" is used in the context of government control of trade, specifically, protectionist tariffs against foreign goods. The discussion is found in Chapter 2 of Book IV "Of Systems of Political Economy". Book IV begins with the following paragraph:

Political œconomy, considered as a branch of the science of a statesman or legislator, proposes two distinct objects; first, to provide a plentiful revenue or subsistence for the people, or more properly to enable them to provide such a revenue or subsistence for themselves; and secondly, to supply the state or commonwealth with a revenue sufficient for the publick services. It proposes to enrich both the people and the sovereign.In short, this is about what governments can and cannot accomplish. Chapter 2 begins as a discussion of government-granted monopolies to domestic industries, and continues as an explication of the harm that such monopolies cause to the general welfare, as in:

By restraining, either by high duties, or by absolute prohibitions, the importation of such goods from foreign countries as can be produced at home, the monopoly of the home–market is more or less secured to the domestick industry employed in producing them. Thus the prohibition1 of importing either live cattle or salt provisions from foreign countries secures to the graziers of Great Britain the monopoly of the home–market for butchers–meat. ...The invisible hand quote in context:

That this monopoly of the home–market frequently gives great encouragement to that particular species of industry which enjoys it, and frequently turns towards that employment a greater share of both the labour and stock of the society than would otherwise have gone to it, cannot be doubted. But whether it tends either to increase the general industry of the society, or to give it the most advantageous direction, is not, perhaps, altogether so evident.

No regulation of commerce can increase the quantity of industry in any society beyond what its capital can maintain. It can only divert a part of it into a direction into which it might not otherwise have gone; and it is by no means certain that this artificial direction is likely to be more advantageous to the society than that into which it would have gone of its own accord.The rest of the chapter is chiefly devoting to explicating when this general rule is false, such as when national defense is involved, or when tariffs are being imposed against your own goods.

....

What is the species of domestick industry which his capital can employ, and of which the produce is likely to be of the greatest value, every individual, it is evident, can, in his local situation, judge much better than any statesman or lawgiver can do for him. The stateman, who should attempt to direct private people in what manner they ought to employ their capitals, would not only load himself with a most unnecessary attention, but assume an authority which could safely be trusted, not only to no single person, but to no council or senate whatever, and which would nowhere be so dangerous as in the hands of a man who had folly and presumption enough to fancy himself fit to exercise it.16 11To give the monopoly of the home–market to the produce of domestick industry, in any particular art or manufacture, is in some measure to direct private people in what manner they ought to employ their capitals, and must, in almost all cases, be either a useless or a hurtful regulation. If the produce of domestick can be brought there as cheap as that of foreign industry, the regulation is evidently useless. If it cannot, it must generally be hurtful.

...

But the annual revenue of every society is always precisely equal to the exchangeable value of the whole annual produce of its industry, or rather is precisely the same thing with that exchangeable value.12 As every individual, therefore, endeavours as much as he can both to employ his capital in the support of domestick industry, and so to direct that industry that its produce may be of the greatest value; every individual necessarily labours to render the annual revenue of the society as great as he can.13 He generally, indeed, neither intends to promote the publick interest, nor knows how much he is promoting it. By preferring the support of domestick to that of foreign industry, he intends only his own security; and by directing that industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention.14 Nor is it always the worse for the society that it was no part of it. By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it. I have never known much good done by those who affected to trade for the publick good. It is an affectation, indeed, not very common among merchants, and very few words need be employed in dissuading them from it.

Proceeding onwards to a more close examination of the epically inane quality of Professor Wonder Dummy's post, let us remind ourselves of how this "market failure" occurred.

A. Three US companies were granted a government monopoly on debt rating by being named as NRSRO's. This consolidation of the market occurred in the 1990s by mergers. I have covered this topic before - search for NRSRO. Although, in theory, other such companies could apply to be certified as NRSROs, despite applications, these three had an effective monopoly on the market.

B. In US financial regulation, the importance of being an NRSRO is that only debt certified as being investment grade by an NRSRO may be held for investment. The significance is that lower-graded debt can be held in trading accounts, but it must be revalued based on market value. Some types of financial pools, such as pension funds, shouldn't be in this at all, and other types, such as banks, may hold lower-rated instruments in trading accounts but they will have to reserve against them and constantly revalue them to current market price levels. So an investment designed to return the same value would be far more saleable if it were investment-rated by one of the NRSROs.

C. In the US, until last year there was no NRSRO that was paid by investors. Instead, the financial interests generating the securities paid the NRSROs to rate them. A lot has been written about the opacity of some of these securities, and it has been well-founded.

Now if one had been able to call up Adam Smith on the Way-Back Phone in, say, 2005, the conversation might have gone something like this:

MoM: (Gives above facts, and continues) Sir, do you consider this as a market experiencing perfect liberty?

Adam Smith: My dear lady, that is a government monopoly which must inevitably tend to produce a market price far above the natural price, as I have described in Chapter 7, Book 1 of "An Inquiry into the Nature and Causes of the Wealth of Nations".

MoM: I've read it. Is this the section you mean?

But though the market price of every particular commodity is in this manner continually gravitating, if one may say so, towards the natural price, yet sometimes particular accidents, sometimes natural causes, and sometimes particular regulations of police, may, in many commodities, keep up the market price, for a long time together, a good deal above the natural price.12Adam Smith: Indeed! You seem uncommonly well educated for woman! (Authors always love it when they found out you've actually read their books.)21When by an increase in the effectual demand, the market price of some particular commodity happens to rise a good deal above the natural price, those who employ their stocks in supplying that market are generally careful to conceal this change. If it was commonly known, their great profit would tempt so many new rivals to employ their stocks in the same way, that, the effectual demand being fully supplied, the market price would soon be reduced to the natural price, and perhaps for some time even below it. If the market is at a great distance from the residence of those who supply it, they may sometimes be able to keep the secret for several years together, and may so long enjoy their extraordinary profits without any new rivals.13 Secrets of this kind, however, it must be acknowledged, can seldom be long kept; and the extraordinary profit can last very little longer than they are kept.

MoM: My father believed in book-larning. And, in your opinion, does this excess in market price over the natural price result from a particular regulation of the police?

Adam Smith: Exactly. This SEC you describe has a police function. By controlling the cost of holding these commoditized securities, it is controlling the relative price. Since a new ratings firm must be nationally recognized in order to qualify as an NRSRO according to the SEC, and since usage of the firm is dependent upon certification by the SEC, because otherwise the firm's ratings will confer no market advantage and are thus worthless, it would seem that there is an effective monopoly. Nor is it in the interest of the institutions generating the debt to sponsor a new firm even if their prices are lower, as long as the prices of the existing NRSROs can be constrained by such a threat. Thus, it is a closed system and it is to the interest of the participants to keep it that way. Naturally the guild members will impose the most stringent secrecy.

MoM: I see what you mean. In effect, this is another example of merchants and manufacturers lobbying for an effective tariff in order to create an effective monopoly to support their prices, as you describe in chapter 2 of "Of Systems of Political Economy"....

Adam Smith: Correct.

MoM: Well, I really appreciate your time. I think I'll bury some hard money somewhere and just wait for the apocalypse.

Adam Smith: Bury money? That would withdraw it from the true production of the country and cause loss of wealth. That should not be necessary, because the large debt guilds you describe know that they cannot keep selling their debt if the opacity disappears, which it will if those who buy the debt find that it is not repaid. They may sell slightly bad debt, but not very bad debt. Their own self-interest will prevent them from doing so.

MoM: Er... What if I told you that the last three times the debt became very bad, the large guilds went to the king and said that it would be harmful to the national defense and protection if they could not sell debt, so the king took money from the farmers and gave it to the guilds to cover their bad debts?

Adam Smith: Bury such of your specie as you cannot conceal about your person, and flee overseas. Then buy a farm. You can employ a trusted, well-paid messenger to gradually extract your buried gold and silver and bring it to you.

MoM: Thanks, I already have the farm. The kings everywhere are doing the same thing so there is no place left to run. I think I'll just wait it out here. When the peasants get hungry enough, they will rise and I'd like to be next to my ammo stockpiles when that happens.

To regress back to Wonder Dummy's post, if there is one obvious thing, it is that the problem here was created by government interference with free markets. The second salient point is that if human irrationality is a factor in non-governmental pursuits, it surely must be equally so in governmental pursuits. In all things, governments enjoy insulation from the real-world effects of their irrationality. Thus, they may continue in it longer than would be possible for any non-governmental actor.

Friday, April 17, 2009

To Round Out The Global Picture

The March figures were reported to be much more favorable, and supposedly industrial production in March was up 8.3% compared to the prior year. This is however a falling figure (+11.0% in February), and that doesn't support the theory that the Chinese economy was rebounding at the end of the quarter.

Historically there has been a strong correlation between Chinese GDP and power consumption figures. For more background, see this January post at the Global Economy Does Matter blog. I would say this equates to about a minimum 3-4% drop in GDP, annualized. It could be more.

For further comparison on a YoY basis, Chinese exports in December 08 were down 2.8% compared with March 09's YoY drop of 17.1%. That was up from the major drop in February (25.7%). YoY Chinese comparisons will be affected all this year by various odd factors affecting China's economy in 2008, which include major snowstorms in the spring which affected travel, energy production, industrial production and ag, the huge quake in the late spring, plus the Olympics and the measures taken to drop power consumption and pollution in advance of the main events. So quarterly averages are best, but are still erratic. Overall the disruptive snowstorms in Q1 08 should have biased 09's comparisons on the positive side.

The final data point is that China has adopted major stimulus measures. One item that seems to concern their own economists is the massive growth in bank loans in the first quarter, which have caused them to up their ALLL requirements on loans. One would expect this massive loan growth to be followed by some pretty severe consequent defaults and to result in a drag on growth in the future without the resumption of very strong expansion.

European industrial production is now falling faster than US industrial production. The latest figures are for February. There is no significant difference between Eurozone (-18.4% YoY) and EU (-17.5%). The decline was largest in capital goods. Both the monthly decline and the YoY declines were significantly higher than for the US. This may not be that surprising, but it is disappointing and it raises further worries about European banks. For comparison, US February industrial production dropped 11.2% (12.8% in March). The rise in European unemployment is very similar to unemployment in the US:

This is the Eurozone measure and it is calculated very similarly to the US official unemployment numbers.

There is now a very close correlation between GDP declines, freight declines, etc across the world's major industrialized nations. This increase in correlation is disturbing, because while it may increase one's confidence in the definition of current circumstances, it also tends to skew downwards any reasonable projections of future growth. Further, the close correlation between Eurozone power production (-3.6% YoY in February) and the Chinese and US figures suggest to me that there is something badly wrong with the official Chinese industrial production figures. I am prepared to believe many things, but not that industrial production is rising significantly over a year while power production is dropping significantly.

Thus we have a picture of a world with a very hefty trade slowdown, and the expectation of significant second order effects as capital and heavy industrial equipment supply businesses continue to substantially contract. Trichet is now on board the concept of "Do everything", but does not have consensus.

India was the last holdout, but its wholesale price inflation figures have dropped to about flat on the year. Only food is holding a real increase, and retail sales figures have continued to trend down by significant factors. India is still squeezing out a tiny rise in YoY power production, which would indicate that it is holding out better than China.

Food inflation in currency-depreciated economies (Poland and Mexico are examples) is further eroding worldwide consumptive power.

In the US, food prices in grocery stores seem to show that weakness in consumer spending power is continuing to grow. This is a very important measure of the economic potential in the near future, because it separates out the psychological factor. Households that are not cash-strapped, even if financially conservative, will continue to spend on their preferred food items even with mild inflation (and currently, these stores are showing an absolute roll-back in food prices from a year ago across all product lines). Households that are under genuine economic stress are forced to control food spending overall (these households tend to be lower-income, but may also be older households diverting their income to medical expenses or to help children and relatives).

Pricing trends in several supermarkets I check in relatively high-end markets over the spring so far have shown an absolute inability to raise prices, which strongly suggests that there is significant further downside to US consumer prices. I have been through bad recessions before, but I have never seen such an astonishing pattern in the US in grocery stores. The closest thing to it were trends during times of very high inflation. However, flattened profit margins were quickly recouped at least somewhat as overall inflation fell. This is not occurring.

By combining these numbers with the WalMart numbers, I have what should be a sample of a very broad majority of the US population. I can only account for the results by adding in demographic effects. In any case, the implications are that US consumer spending will be constrained for several years to come, and the March retail numbers appear to be not a flier, but more of a prediction.

So to sum up:

- The Japanese are waiting hopefully for the Chinese economy to rebound, and have much longer to wait.

- The Europeans think that the US may be rebounding, and that this will at least presage their rebound at the end of 2009. Fat chance.

- The Chinese want the US and Europe to start spending again, but have conceded that this is unlikely to happen to the needed extent, and are trying to implement medical coverage for the broad population in order to boost internal spending. That could start paying off 2-3 years from now, and if it pays off enough, it might help to defray the cost of funding the imploding banks.

- Many of the emerging countries are showing signs of escalating weakness, which is rough on SE Asia because they had been big consumers of electronics and appliances. See Singapore's Q1 annualized -19.7% GDP figure, and consider that Singapore's exports to Malaysia dropped over 20%.

- The Brits are standing around with a stiff upper lip, waiting to be introduced to the recovery, which British government officials maintain has something to do with windmills.

- Sarkozy is preparing to blame all of this on Obama (some things never change),because he refuses to attack Iran, and Bush, because he did attack Iraq.

- The Germans are preparing to expand their already expansive government job support program (see description at the end of this article), so that their big industrials can cut employment in order to maintain profitability (and the ability to pay on their loans).

- The initial effects of lower interest rates (implemented in most economies) on consumer spending for durables are on average fading after 3-5 months.

- In retrospect, some of the largest German financials are regretting their decision to invest in Austrian and Irish banks.

- In retrospect, some of the Austrian banks are regretting having the equivalent of 75% of their GDP lent out to the Central/Eastern exSoviet client bloc. Something about foreign currency loans, which are functionally equivalent to Option ARM loans in situations encompassing sudden currency devaluations. NOT THAT THERE HAVE BEEN ANY OF THOSE as far as the Austrian Economic Minister knows....

- The Austrian minister is very confident in the strength of Austrian banks, due to the stress test which was conducted (although Fitch is less confident, taking somewhat of a retrospective view. The best guess is that this is related to the latest projections of 28% losses on recent Option ARM vintages). Those audits were conducted by the Easter Bunny, right before the Easter Bunny stopped off to help the US banks conduct their own stress tests. That way the US can truthfully say that their external auditor has seen much worse banks and that the big 19 are not that badly off in comparison. It's all in how you present the data. I await May 4th with jovial anxiety.

- Obama of the US sees glimmers of hope for the economy aside from the continued job losses and economic contraction. These glimmers appear to be emanating from windmills and that cute little desktop thingie Obama got from the Austrian Economic Minister.

It further suggests that Chinese internal capital needs are going to grow for several years to come. I don't really know who we are going to get to fund our government borrowing.

I see the wall looming and an economic state change. There has never been anything remotely like this post WWII. The peak oil people are going to have to give it a rest for a few years. CF may hit his $18 crude mark yet if the Europeans can't get it together. The downturn is now too correlated across countries with financing problems (Spain, the US, etc) and countries that had strong balance sheets (China, Canada).

At this point the Europeans might as well pull the Eastern European blocs directly into the EU with a favorable currency conversion. There is not much downside left, and it would stabilize intra-European exports some what and put a floor on some of the bank losses.

Wednesday, April 15, 2009

Does Anyone Know?

And There's The Big Cliff

Retail sales. Germany and France - the latest figures are really bad. Of course European figures as a whole are also bad. The implications are that German GDP will drop very substantially for the first quarter. Japanese retail sales are also continuing to decline. The US March report was also quite bad, reversing the gains of the first two months of the quarter. It was SO bad that the only categories which gained YoY were drugstores and grocery stores, meaning that overall we are still eating and taking most of our medicine. The French retail sales figures showed substantial drops in revenue from food sales, to put it into perspective.

The primary factors affecting US retail March sales are the wholesale jacking up of CC rates and cutting of lines at the big banks, small business expectations, unemployment, the rise in gas prices, and Easter's shift relative to the prior year. The weekend before Easter was in April this year, whereas it was in March last year. So there should be some relative improvement in April from the Easter effect.

Substantial cuts in interest rates in China and India had boosted auto sales in both countries in the first quarter, but it will be very hard to replace Western consumption drops with consumption rises in these two countries in the near term.

Which leads us to the topic of industrial overcapacity. In the US, March industrial production racked up another 1.5% decline monthly, to match February's. On a YoY basis, industrial production has fallen 12.8% - which brings me back yesterday's grim musings about gross private domestic investment in the US, and the impossibility of a real recovery in 2009.

Capacity utilization (see above link) is at an astounding 69.3%. Manufacturing capacity utilization is reported to be 65.8%.

Globally:

The latest Brazilian figures (which are pretty trustworthy) for February show that industrial production for Jan/Feb dropped 17.2% in comparison to the same period of 2008. See this blog post for a nice survey of the 2008 stats for various significant countries. Indian industrial production has gone negative YoY. I find China's stats confusing, so I use energy consumption as a proxy. That is still negative on a YoY basis in the first quarter, but the YoY drop is reported to be much less for March than for the two prior months. Russian industrial production was reported to be down 14.3% in the first quarter on a YoY basis. For February, German industrial production was reported to have dropped 20.6% on the year, and Italian industrial production was reported to have dropped 20.7%. The Japanese industrial production numbers are shattering. For February, the YoY was -38.4%. The decline from January was 9.4%.

The Japanese figures bode ill for US and German manufacturing as well. The Japanese have a huge business in making high-end industrial production equipment, and the fall in building and operating factories is producing a gigantic drop in their figures. Until China recovers, it would appear that Japan is doomed to suffer terribly.

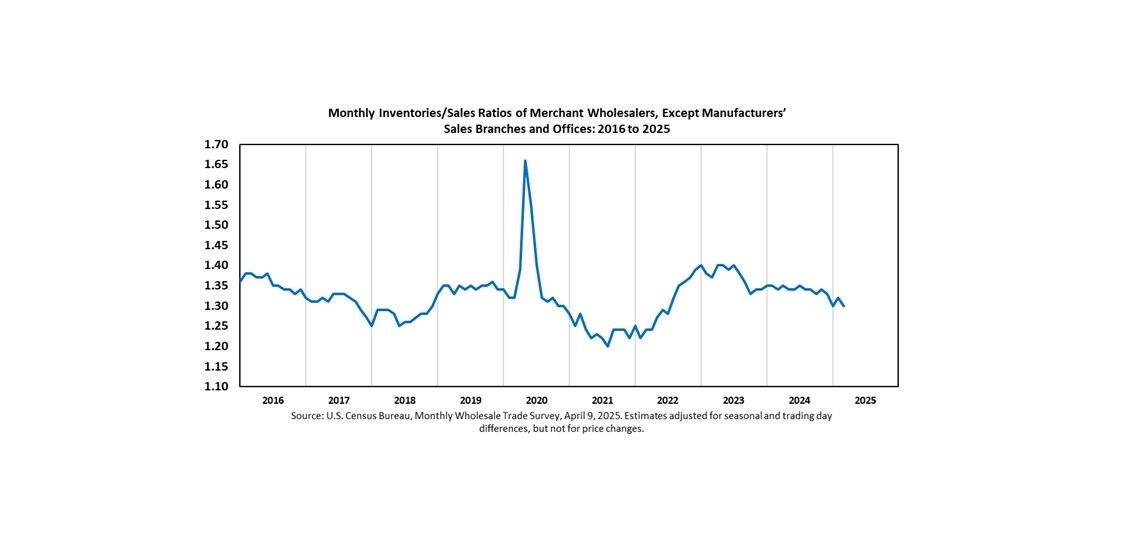

PS: I keep reading chirpy comments about inventory reductions. Well, what matters are current inventory/sales ratios. It looks to me like we've got considerably further to go:

Monday, April 13, 2009

Rumors Of My Demise Were Not Hugely Exaggerated

I've still got a bit of trouble with my eyes, but due to my brother's delivery of a Linux box, which I have set to large print, I should be back with you shortly.

I have spent a few hours catching up today by reading Fed releases and my regular news sources, and I am impressed by the official US ability to spin delusion. The BRIC bloc is in deep trouble, and there is little chance for the US to resume growth with carrying power this year.

For the US to resume real growth, gross private domestic investment would have to shift into the positive territory. Look at these numbers gleaned from recent Treasury Monthly statements:

March Corporate Income Tax (before refunds):The fiscal year started in October.

08: 37,997

09: 22,315 (-41%)

FYTD Corporate Income Tax (before refunds)

08: 158,940

09: 102,224 (-35.7%)

March Personal Income Tax (before refunds):

08: 100,049

09: 92,682 (-7.3%)

FYTD Personal Income Tax(before refunds):

08: 634,217

09: 579,139 (-8.7%)

Until corporate profits stabilize, money isn't going to be put into investment. It is at this point that one suspects that the Obama administration placed too much emphasis on talking about the economic downturn as a crisis as a way of passing out money to favored causes while simultaneously not taking the economic downturn seriously. I write this because it would truly have helped to have significant money dumped into infrastructure improvements ASAP, but the stimulus measures that have been passed are heavily weighted toward later years, economically nonessential payments to very narrow interests, and shoring up a feeble financial sector, while doing little to stimulate economic activity now.

The result will be higher unemployment, which will cause significantly higher credit defaults, which will negate at least part of the money being dumped into the larger financials.

This is Gross Private Domestic Investment since 2000, by quarter. As you can see, it fell in 2006, revived slightly in 2007, and has taken another cascade down in 2008.

This is Gross Private Domestic Investment since 2000, by quarter. As you can see, it fell in 2006, revived slightly in 2007, and has taken another cascade down in 2008.It defies all reason to expect it to head up substantially until the government throws massive stimulus into the real economy, or until corporate profits revive somewhat. Gross private domestic investment is the real driver of the US economy. Real gross private domestic investment fell 5.4% in 2007 (which was why I was so confident in stating that we were in a recession) and fell another 6.7% in 2008. The best we can hope for is a smaller decline in 2009, but we aren't going to rack up any annual growth.

With falling incomes and our current demographics, you are not going to get major boosts in consumer spending. It will revive somewhat as cars, clothing and appliances wear out, but you can't expect any huge jumps there until the employment situation improves. Unemployment can't improve this year, and no one is suggesting it will.

But with employment declining, and CRE busting so badly, and with corporate profits in a profound swoon, the fundamental economic choices facing a government are:

- The government lets the natural economic cycle run its course (and that natural economic cycle is for a depression-like event), or

- The government intervenes to bring needed infrastructure investments a few years forward, which puts a floor on the drop in economic activity, supports employment, and knocks the bottom off the cycle.

Thus, the claims by people like Roubini and CR that the "stress test" of banks is a farce are well-founded, and observations by industry analysts that rosy profit statements by various banks are often produced by under-reserving for future losses are also quite well-founded.

![]()

{kind=link}