MaxedOutMama

MaxedOutMama

Wednesday, April 15, 2009

And There's The Big Cliff

US crude inventories. Petroleum products up 11.2% ex SPR, and crude stocks up 16.5% (in comparison to a year ago). Petroleum import prices for February and March were $39.XX, and it is unlikely that those prices can be sustained over the course of this year.

Retail sales. Germany and France - the latest figures are really bad. Of course European figures as a whole are also bad. The implications are that German GDP will drop very substantially for the first quarter. Japanese retail sales are also continuing to decline. The US March report was also quite bad, reversing the gains of the first two months of the quarter. It was SO bad that the only categories which gained YoY were drugstores and grocery stores, meaning that overall we are still eating and taking most of our medicine. The French retail sales figures showed substantial drops in revenue from food sales, to put it into perspective.

The primary factors affecting US retail March sales are the wholesale jacking up of CC rates and cutting of lines at the big banks, small business expectations, unemployment, the rise in gas prices, and Easter's shift relative to the prior year. The weekend before Easter was in April this year, whereas it was in March last year. So there should be some relative improvement in April from the Easter effect.

Substantial cuts in interest rates in China and India had boosted auto sales in both countries in the first quarter, but it will be very hard to replace Western consumption drops with consumption rises in these two countries in the near term.

Which leads us to the topic of industrial overcapacity. In the US, March industrial production racked up another 1.5% decline monthly, to match February's. On a YoY basis, industrial production has fallen 12.8% - which brings me back yesterday's grim musings about gross private domestic investment in the US, and the impossibility of a real recovery in 2009.

Capacity utilization (see above link) is at an astounding 69.3%. Manufacturing capacity utilization is reported to be 65.8%.

Globally:

The latest Brazilian figures (which are pretty trustworthy) for February show that industrial production for Jan/Feb dropped 17.2% in comparison to the same period of 2008. See this blog post for a nice survey of the 2008 stats for various significant countries. Indian industrial production has gone negative YoY. I find China's stats confusing, so I use energy consumption as a proxy. That is still negative on a YoY basis in the first quarter, but the YoY drop is reported to be much less for March than for the two prior months. Russian industrial production was reported to be down 14.3% in the first quarter on a YoY basis. For February, German industrial production was reported to have dropped 20.6% on the year, and Italian industrial production was reported to have dropped 20.7%. The Japanese industrial production numbers are shattering. For February, the YoY was -38.4%. The decline from January was 9.4%.

The Japanese figures bode ill for US and German manufacturing as well. The Japanese have a huge business in making high-end industrial production equipment, and the fall in building and operating factories is producing a gigantic drop in their figures. Until China recovers, it would appear that Japan is doomed to suffer terribly.

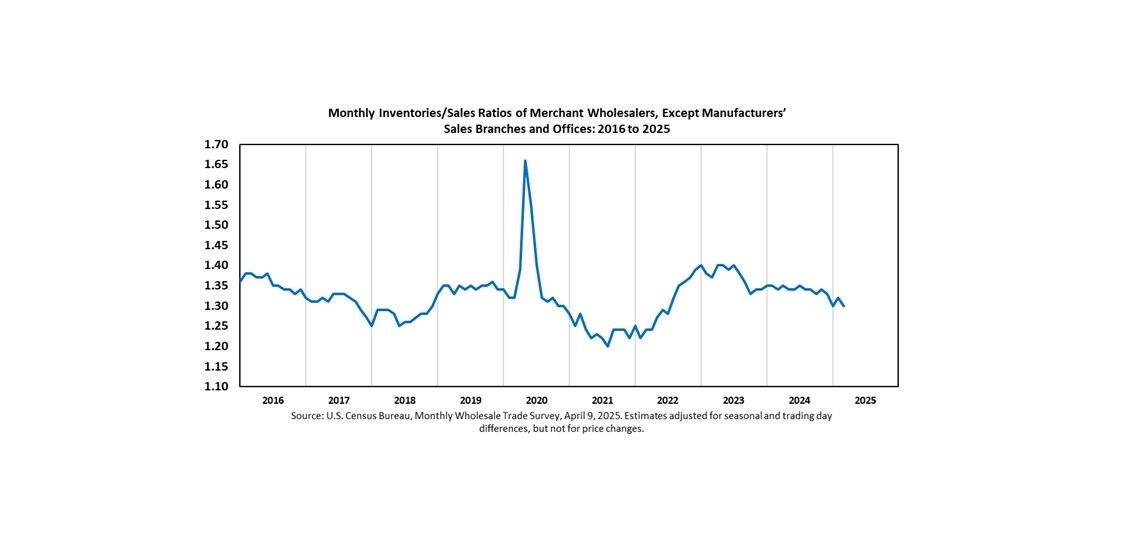

PS: I keep reading chirpy comments about inventory reductions. Well, what matters are current inventory/sales ratios. It looks to me like we've got considerably further to go:

Retail sales. Germany and France - the latest figures are really bad. Of course European figures as a whole are also bad. The implications are that German GDP will drop very substantially for the first quarter. Japanese retail sales are also continuing to decline. The US March report was also quite bad, reversing the gains of the first two months of the quarter. It was SO bad that the only categories which gained YoY were drugstores and grocery stores, meaning that overall we are still eating and taking most of our medicine. The French retail sales figures showed substantial drops in revenue from food sales, to put it into perspective.

The primary factors affecting US retail March sales are the wholesale jacking up of CC rates and cutting of lines at the big banks, small business expectations, unemployment, the rise in gas prices, and Easter's shift relative to the prior year. The weekend before Easter was in April this year, whereas it was in March last year. So there should be some relative improvement in April from the Easter effect.

Substantial cuts in interest rates in China and India had boosted auto sales in both countries in the first quarter, but it will be very hard to replace Western consumption drops with consumption rises in these two countries in the near term.

Which leads us to the topic of industrial overcapacity. In the US, March industrial production racked up another 1.5% decline monthly, to match February's. On a YoY basis, industrial production has fallen 12.8% - which brings me back yesterday's grim musings about gross private domestic investment in the US, and the impossibility of a real recovery in 2009.

Capacity utilization (see above link) is at an astounding 69.3%. Manufacturing capacity utilization is reported to be 65.8%.

Globally:

The latest Brazilian figures (which are pretty trustworthy) for February show that industrial production for Jan/Feb dropped 17.2% in comparison to the same period of 2008. See this blog post for a nice survey of the 2008 stats for various significant countries. Indian industrial production has gone negative YoY. I find China's stats confusing, so I use energy consumption as a proxy. That is still negative on a YoY basis in the first quarter, but the YoY drop is reported to be much less for March than for the two prior months. Russian industrial production was reported to be down 14.3% in the first quarter on a YoY basis. For February, German industrial production was reported to have dropped 20.6% on the year, and Italian industrial production was reported to have dropped 20.7%. The Japanese industrial production numbers are shattering. For February, the YoY was -38.4%. The decline from January was 9.4%.

The Japanese figures bode ill for US and German manufacturing as well. The Japanese have a huge business in making high-end industrial production equipment, and the fall in building and operating factories is producing a gigantic drop in their figures. Until China recovers, it would appear that Japan is doomed to suffer terribly.

PS: I keep reading chirpy comments about inventory reductions. Well, what matters are current inventory/sales ratios. It looks to me like we've got considerably further to go:

![]()

{kind=link}