MaxedOutMama

MaxedOutMama

Tuesday, May 26, 2015

I Wouldn't Call That Reassuring

I saw a perky headline about April's durable goods release. It didn't quite match the reality.

There are signs of a more structural slowdown in April's report. YoY, shipments are up and new orders are down. Total +3.5%/-1.3%. And so it goes, with autos being about the best category.

If this continues - which it may well not - we are in for a much slower economy the rest of this year than the Fed expects. You can make a case that the oil slowdown accounts for a lot of this, but it doesn't matter - if it persists, things will be difficult this fall. YoY YTD capital goods new orders are down 5.9% (-5.9%).

On the other hand, it might be that this clears out in May/June, and we pick up some impetus.

So far rail has not shown improvement - we have gone slightly negative on the YoY YTD in the last rail report, and we will have to wait two more weeks to see if that is real or will redress after the difference in the Memorial Day calendar works its way out of the figures. The weakness is in carloads, which generally does precede the decline in intermodal.

So far this year the economic data is stunningly equivocal, which makes me think that we'll stagger through with the help of construction. But in a month or two I may revise my thinking if there are no signs of life elsewhere.

The KC manufacturing index for May was frankly disturbing.

There are signs of a more structural slowdown in April's report. YoY, shipments are up and new orders are down. Total +3.5%/-1.3%. And so it goes, with autos being about the best category.

If this continues - which it may well not - we are in for a much slower economy the rest of this year than the Fed expects. You can make a case that the oil slowdown accounts for a lot of this, but it doesn't matter - if it persists, things will be difficult this fall. YoY YTD capital goods new orders are down 5.9% (-5.9%).

On the other hand, it might be that this clears out in May/June, and we pick up some impetus.

So far rail has not shown improvement - we have gone slightly negative on the YoY YTD in the last rail report, and we will have to wait two more weeks to see if that is real or will redress after the difference in the Memorial Day calendar works its way out of the figures. The weakness is in carloads, which generally does precede the decline in intermodal.

So far this year the economic data is stunningly equivocal, which makes me think that we'll stagger through with the help of construction. But in a month or two I may revise my thinking if there are no signs of life elsewhere.

The KC manufacturing index for May was frankly disturbing.

Tuesday, May 19, 2015

But Winter Must End!!!

Okay, not in Ice Ages, but currently we are in one of the balmy interludes, although I can concede that Bostonians may have wondered about that earlier this year.

New Residential Construction takes a really strong pop in April. Very nice. Very strong. In both permits and starts.

The economy may not be that strong, but it is getting its legs under it.

New Residential Construction takes a really strong pop in April. Very nice. Very strong. In both permits and starts.

The economy may not be that strong, but it is getting its legs under it.

Friday, May 15, 2015

The Real World Effect Of That Big Flaming Ball Of Gas In The Sky

Secondary to my previous post, here's the joy of it all.

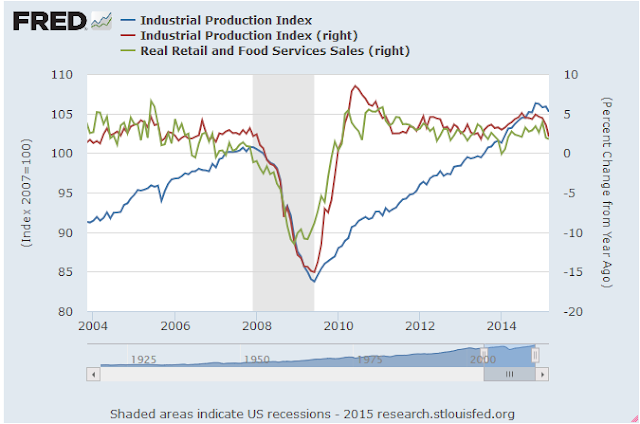

Industrial production was released today. Here's the result:

IP has been working down a bit for months. The blue line is the index, the red line is the YoY. The green line is real retail YoY. We're not QUITE in a recession yet, and hopefully we won't get there, but the reason we are not was the giveback on the gas. That gave consumers enough back to get them through another bad winter with more margin. But we are right on the line. I expect IP to rebound slightly in May - the latest report is

Rail confirms this but may be giving my May rebound theory the raspberry:

That blue line is just failing to green shoot, and this goes through May 9th. Rail was hard to read this year, because of course the port strike slowed things, and then there was a rebound, so one had to just sit and wait for all of that to work itself out of the system to confirm a trend.

Now, I still believe there is the economic space to get out of this without recession. Nor am I surprised, because honestly the direction of CMI does show tightness. But it is not the time to be loading the economy down with ANY more regulatory mandates, and ACA changes have truly had a very adverse effect on many families. Consumer Units.

This is all quite dire for China, which usually gets a May uplift from the US retail cycle, and may not get that much of one this year. China's economy looks really weak.

A close-up on that mug shot:

The red, graphed on the right scale, is IP YoY. The green real retail YoY.

The red, graphed on the right scale, is IP YoY. The green real retail YoY.

I was trying to find the reason for the real stresses seen in NACM CMI, and one of the things I came up with is the sharply increased electricity costs for some regions, combined with a bad winter.

In any case, if we want to scrape through this "soft" patch, we are going to have to do it ourselves. The only government policy that is helping at all this year is the drop in FHA premiums.

Industrial production was released today. Here's the result:

IP has been working down a bit for months. The blue line is the index, the red line is the YoY. The green line is real retail YoY. We're not QUITE in a recession yet, and hopefully we won't get there, but the reason we are not was the giveback on the gas. That gave consumers enough back to get them through another bad winter with more margin. But we are right on the line. I expect IP to rebound slightly in May - the latest report is

Rail confirms this but may be giving my May rebound theory the raspberry:

For the first 18 weeks of 2015, U.S. railroads reported cumulative volume of 5,043,559 carloads, down 1.8 percent from the same point last year; and 4,679,513 intermodal units, up 1.7 percent from last year. Total combined U.S. traffic for the first 18 weeks of 2015 was 9,723,072 carloads and intermodal units, a decrease of 0.1 percent compared to last year.Here's the graph - we've been weakening recently:

That blue line is just failing to green shoot, and this goes through May 9th. Rail was hard to read this year, because of course the port strike slowed things, and then there was a rebound, so one had to just sit and wait for all of that to work itself out of the system to confirm a trend.

Now, I still believe there is the economic space to get out of this without recession. Nor am I surprised, because honestly the direction of CMI does show tightness. But it is not the time to be loading the economy down with ANY more regulatory mandates, and ACA changes have truly had a very adverse effect on many families. Consumer Units.

This is all quite dire for China, which usually gets a May uplift from the US retail cycle, and may not get that much of one this year. China's economy looks really weak.

A close-up on that mug shot:

I was trying to find the reason for the real stresses seen in NACM CMI, and one of the things I came up with is the sharply increased electricity costs for some regions, combined with a bad winter.

In any case, if we want to scrape through this "soft" patch, we are going to have to do it ourselves. The only government policy that is helping at all this year is the drop in FHA premiums.

Thursday, May 14, 2015

Speaking of the Economic Weather Report

There is no question that bad winters are not helping the US economy. Admittedly, there are other problems, such as public debt at the state and local level. You simply cannot integrate a model with growing economies, constrained household incomes, and an ever-growing state and local tax burden. Something's got to give, and it is going to be real growth.

But as a sideline, and perhaps a gentle hint not to buy farmland too far north, I thought I'd look at a little bit of the climate data. I have remained a spectator in the carbon wars, watching with increasing fascination as the real world situation ameliorated and the human angst-o-sphere heated up to compensate. Now that we have the Pope piling in, I suspect that has reached its natural peak, unless the Chief Rabbi is waiting in the wings.

In the real world, colder northern winter temps will have an effect, and the angst-o-sphere will not compensate.

First, from the really excellent site WoodForTrees.org, a look at what happened when China dumped a massive amount of carbon into the atmosphere:

We have here the RSS lower troposphere temp data series. The benefit is that it is very, very accurate. The downside is that it is of short duration, though lengthening every year. We have a few trend lines - since 1998 it's obvious that it has been getting colder. Since 1995 (nearly 20 years!) the trend line is about flat, which surely means something.

We also have the monthly sunspots on a 20 year average, which I long ago figured out was the best predictor represented this way. (Note that this program charts means at the center point, so that is why the curve is shifted left on the graph.) And then we have the sharp upward trend of Mauna Loa CO2. One suspects that is not controlling global temperatures much.

It is evident that something changed in the late 1990s. The CO2 keeps going up and up, but it isn't driving temps up. There is a suspicious hint that solar activity is. That trend shifts, and lo and behold, so does the troposphere trend.

Yes, yes, I have read all that stuff about the heat hiding in the oceans. Really? One day the heat just looked up into the sky and screamed "OMG - Where are the sunspots?",and the heat dove deep into the ocean to hide from the implacable, frowning face of its solar master like Godzilla when the Japanese planes get too close? Nah. Not even a plausible fairy tale.

Solar activity does vary a lot over time, and it does seem to correlate with temps as observed, although it's well to note that in the past land temperature measurements were biased toward the northern hemisphere (and they still are today) and that they will be a lot less accurate than satellite data. So mentally stick in some large error bars:

Here we have HADCRUT3, which is a much longer running temp series, with AMO (the northern oscillation) and sunspots. Normalized and 10 year means. I'm not trying to pull tricks here.

Here we have HADCRUT3, which is a much longer running temp series, with AMO (the northern oscillation) and sunspots. Normalized and 10 year means. I'm not trying to pull tricks here.

As you can see, the historical record is that solar activity does vary a lot over time. There has seemed to be a correlation with climate. I added AMO, because I suspect part of the northern climate transition is driven by AMO, and that solar activity drives AMO

Note that I don't claim that CO2 has no effect on temperatures - I suspect that it does, but only a very weak one, and in part that effect is offset by changes in the distribution of water vapor in the atmosphere (a negative feedback rather than the theorized positive feedback).

I also suspect that the jagged AMO ridges when AMO is in transition are correlated with US dustbowls, which makes me a bit nervous.

This is pretty much the same thing, but I added in PDO (Pacific oscillation). Why? Just in case you wanted it. I think the ocean current shifts distribute the heat, but I think they may be largely influenced by solar shifts.

This is pretty much the same thing, but I added in PDO (Pacific oscillation). Why? Just in case you wanted it. I think the ocean current shifts distribute the heat, but I think they may be largely influenced by solar shifts.

A look at my theorized system during the time frame that we have concurrent data:

I think AMO loops within its own bounds, which is a natural regulator of solar changes. But the point is that AMO does seem to influence northern weather, which has several implications. For one, steeper roofs in Boston would be wise. For another, this cycle has only just begun, so I wouldn't expect these last winters to be flukes. I would expect the coming US northern climate to be far more akin to that of the tales told by my parents and grandparents when I was young. Winters used to be colder, they would say, and you know, they were right.

I think AMO loops within its own bounds, which is a natural regulator of solar changes. But the point is that AMO does seem to influence northern weather, which has several implications. For one, steeper roofs in Boston would be wise. For another, this cycle has only just begun, so I wouldn't expect these last winters to be flukes. I would expect the coming US northern climate to be far more akin to that of the tales told by my parents and grandparents when I was young. Winters used to be colder, they would say, and you know, they were right.

Last, a look at the above with a five year mean, just so you know I am not cheating:

One of the interesting things lost in the angst-o-sphere has been the remarkable similarity in the temperature sequence between the 1900-1940 shift and the late 1970s-2000 shift. I have a LOT of trouble accepting CO2 as a strong driver, especially since these shifts are, historically speaking, piddling. Picayune. Petty. Pipsqueaks:

I crack up when I read or hear stuff about how the melting Arctic is going to hand us Tatooine. Been there, done that. If in the climactic optimum the methane didn't fry us, it is not going to fry us now.

The Hans Tausen Iskappe in Greenland completely melted during the climactic optimum. It has formed since it started getting colder.

What we have to worry about in the near term are northern climate conditions that may be a little harsh, and will have an effect over the longer term on economic growth.

But as a sideline, and perhaps a gentle hint not to buy farmland too far north, I thought I'd look at a little bit of the climate data. I have remained a spectator in the carbon wars, watching with increasing fascination as the real world situation ameliorated and the human angst-o-sphere heated up to compensate. Now that we have the Pope piling in, I suspect that has reached its natural peak, unless the Chief Rabbi is waiting in the wings.

In the real world, colder northern winter temps will have an effect, and the angst-o-sphere will not compensate.

First, from the really excellent site WoodForTrees.org, a look at what happened when China dumped a massive amount of carbon into the atmosphere:

We have here the RSS lower troposphere temp data series. The benefit is that it is very, very accurate. The downside is that it is of short duration, though lengthening every year. We have a few trend lines - since 1998 it's obvious that it has been getting colder. Since 1995 (nearly 20 years!) the trend line is about flat, which surely means something.

We also have the monthly sunspots on a 20 year average, which I long ago figured out was the best predictor represented this way. (Note that this program charts means at the center point, so that is why the curve is shifted left on the graph.) And then we have the sharp upward trend of Mauna Loa CO2. One suspects that is not controlling global temperatures much.

It is evident that something changed in the late 1990s. The CO2 keeps going up and up, but it isn't driving temps up. There is a suspicious hint that solar activity is. That trend shifts, and lo and behold, so does the troposphere trend.

Yes, yes, I have read all that stuff about the heat hiding in the oceans. Really? One day the heat just looked up into the sky and screamed "OMG - Where are the sunspots?",and the heat dove deep into the ocean to hide from the implacable, frowning face of its solar master like Godzilla when the Japanese planes get too close? Nah. Not even a plausible fairy tale.

Solar activity does vary a lot over time, and it does seem to correlate with temps as observed, although it's well to note that in the past land temperature measurements were biased toward the northern hemisphere (and they still are today) and that they will be a lot less accurate than satellite data. So mentally stick in some large error bars:

As you can see, the historical record is that solar activity does vary a lot over time. There has seemed to be a correlation with climate. I added AMO, because I suspect part of the northern climate transition is driven by AMO, and that solar activity drives AMO

Note that I don't claim that CO2 has no effect on temperatures - I suspect that it does, but only a very weak one, and in part that effect is offset by changes in the distribution of water vapor in the atmosphere (a negative feedback rather than the theorized positive feedback).

I also suspect that the jagged AMO ridges when AMO is in transition are correlated with US dustbowls, which makes me a bit nervous.

A look at my theorized system during the time frame that we have concurrent data:

Last, a look at the above with a five year mean, just so you know I am not cheating:

One of the interesting things lost in the angst-o-sphere has been the remarkable similarity in the temperature sequence between the 1900-1940 shift and the late 1970s-2000 shift. I have a LOT of trouble accepting CO2 as a strong driver, especially since these shifts are, historically speaking, piddling. Picayune. Petty. Pipsqueaks:

I crack up when I read or hear stuff about how the melting Arctic is going to hand us Tatooine. Been there, done that. If in the climactic optimum the methane didn't fry us, it is not going to fry us now.

The Hans Tausen Iskappe in Greenland completely melted during the climactic optimum. It has formed since it started getting colder.

What we have to worry about in the near term are northern climate conditions that may be a little harsh, and will have an effect over the longer term on economic growth.

Wednesday, May 13, 2015

It's All About The Chickens Now

No, really, it is all about the chickens, aka bird flu. If it jumps to pigs, we're done. As it is, it's hard to see how poultry prices won't rise for the consumer, which is going to have a depressing effect August through the end of the year.

CA drought not helping either.

The headlines on the April retail report are rather dour, but the real picture is skewed by the Easter timing. The March report indeed was revised up, but that makes April look worse, because sales that are usually in April show up in March. These reports aren't adjusted for prices, and I think there is considerable strong-dollar effect in weaker prices, so the real picture is probably considerably better.

The actual report does show some weakness both YoY and in the rolling three-month SA. It's better to use the three-month totals in cases like this. Currently the Feb-Apr YoY is +1.5%, ex autos +0.4%. So that is not good. From the prior three months (Nov-Jan) it's -0.6%, ex autos -0.7%. But it's not like April sales just suddenly flat-lined.

Retail is weak, and very dependent on autos which are credit-related.

Groceries are a bit worrisome. That's what I am watching. However restaurants are doing well, which slightly offsets it. Wages are rising more slowly than expenditures on food, which, to be blunt, is never a good sign. Wages are left in the dust by costs for medicine, for example, which somewhat depresses other categories.

So we still have a price-sensitive consumer with wary spending behaviors on anything not paid for out of credit.

NFIB's Small Business report was somewhat encouraging yesterday. It rose after the decisive March fall; capital outlays looked encouraging and hiring looked encouraging. Sales are declining only slightly and earnings are up. Prices are constrained by reality. There is no inflationary pressure evident in the NFIB report except for wages/compensation. There is pressure there. In order to get decent employees increases are necessary (this comes through strongly), but the pricing power isn't there to compensate that well for it.

This month's survey is one of the large-sample months, so it is more reliable. There is no sign that we are losing momentum in it - just that epic expansion is not to be expected. But that is more normal than not.

Atlanta Fed Business Inflation Expectations agree well with NFIB's employment comp crunch - expected inflation is up to 1.9%, which would be encouraging if you are a Fed Head looking to raise rates. Two-thirds of polled firms are facing higher compensation costs, and the vast majority intend to raise prices to compensate. '

So who wins? If the chickens cooperate, inflation running about 2.3% over the course of the year. If the chickens don't cooperate, the ability to raise prices to consumers isn't there, and the strong dollar constrains export rises, so ...

Businesses are not behaving as if they expect real problems, and some of the inventory builds are just buying cheaply while they can. So I rate it continued expansion for six months.

Now those consumers!!! Those consumers may have to work a little harder, but the dollar shock should be over, the oil crunch should bottom out late second quarter or early third, and so as long as we keep buying motor vehicles, all should be well.

I do not have a clue as to whether the motor vehicle sales will hold up. Not a clue. I could argue it either way. The current suggestion is that the overall growth trajectory is slightly lower going into the third quarter, with second quarter being of course lifted by seasonal effects.

I would be sure we were out of the woods, except that the fourth month freight total isn't looking too fine, and rail has shown a very slight weakening in the last month, which is not what I expected. So I am still where I landed last October - the drop in fuel prices should have enough oomph to carry us over a naturally structurally soft patch.

And the threat to that is chickens, seriously. Nothing changes consumer behavior like difficulty covering the very basic expenses.

ACA and higher medical deductibles do show up in economic figures. Consumers facing higher medical costs are slow the first half of the year.

CA drought not helping either.

The headlines on the April retail report are rather dour, but the real picture is skewed by the Easter timing. The March report indeed was revised up, but that makes April look worse, because sales that are usually in April show up in March. These reports aren't adjusted for prices, and I think there is considerable strong-dollar effect in weaker prices, so the real picture is probably considerably better.

The actual report does show some weakness both YoY and in the rolling three-month SA. It's better to use the three-month totals in cases like this. Currently the Feb-Apr YoY is +1.5%, ex autos +0.4%. So that is not good. From the prior three months (Nov-Jan) it's -0.6%, ex autos -0.7%. But it's not like April sales just suddenly flat-lined.

Retail is weak, and very dependent on autos which are credit-related.

Groceries are a bit worrisome. That's what I am watching. However restaurants are doing well, which slightly offsets it. Wages are rising more slowly than expenditures on food, which, to be blunt, is never a good sign. Wages are left in the dust by costs for medicine, for example, which somewhat depresses other categories.

So we still have a price-sensitive consumer with wary spending behaviors on anything not paid for out of credit.

NFIB's Small Business report was somewhat encouraging yesterday. It rose after the decisive March fall; capital outlays looked encouraging and hiring looked encouraging. Sales are declining only slightly and earnings are up. Prices are constrained by reality. There is no inflationary pressure evident in the NFIB report except for wages/compensation. There is pressure there. In order to get decent employees increases are necessary (this comes through strongly), but the pricing power isn't there to compensate that well for it.

This month's survey is one of the large-sample months, so it is more reliable. There is no sign that we are losing momentum in it - just that epic expansion is not to be expected. But that is more normal than not.

Atlanta Fed Business Inflation Expectations agree well with NFIB's employment comp crunch - expected inflation is up to 1.9%, which would be encouraging if you are a Fed Head looking to raise rates. Two-thirds of polled firms are facing higher compensation costs, and the vast majority intend to raise prices to compensate. '

So who wins? If the chickens cooperate, inflation running about 2.3% over the course of the year. If the chickens don't cooperate, the ability to raise prices to consumers isn't there, and the strong dollar constrains export rises, so ...

Businesses are not behaving as if they expect real problems, and some of the inventory builds are just buying cheaply while they can. So I rate it continued expansion for six months.

Now those consumers!!! Those consumers may have to work a little harder, but the dollar shock should be over, the oil crunch should bottom out late second quarter or early third, and so as long as we keep buying motor vehicles, all should be well.

I do not have a clue as to whether the motor vehicle sales will hold up. Not a clue. I could argue it either way. The current suggestion is that the overall growth trajectory is slightly lower going into the third quarter, with second quarter being of course lifted by seasonal effects.

I would be sure we were out of the woods, except that the fourth month freight total isn't looking too fine, and rail has shown a very slight weakening in the last month, which is not what I expected. So I am still where I landed last October - the drop in fuel prices should have enough oomph to carry us over a naturally structurally soft patch.

And the threat to that is chickens, seriously. Nothing changes consumer behavior like difficulty covering the very basic expenses.

ACA and higher medical deductibles do show up in economic figures. Consumers facing higher medical costs are slow the first half of the year.

Friday, May 08, 2015

Quickie Update

Altogether this seems improved. The employment report is good, with substantial agreement between the household survey and the establishment survey, which surely should seem to reinforce the good news. Household comes in at +192K this onh. The establishment survey for March was revised down, so it is now closer to the household number, although still higher.

The two month household is 236 thousand. The monthly average for establishment is much higher, so I expect downward establishment revisions later. But still, not bad.

CMI for April was released with very substantial upward revisions for Feb/March. It is still on a declining pattern but now out of the into-the-wall version we saw last month. It is weaker YoY, but VERY IMPORTANTLY, now shows an uptick in credit granted for April.

The economy is weak and we won't see a great second quarter, but it's not flatlining.

The major weakness in the economy can be seen in the establishment survey, giving average hourly wages YoY having increased by 53 cents an hour. Doesn't buy you much! So there's tightness on the consumption end. However the employee-population ratio increased from 58.9 to 59.3 over the year, although it has been static for the last few months.

I see further ominous Drudge headlines about all the people not working. Well, we are going to see the retirees in our overall numbers, because all the people born through 1950 are either 65 or going to turn 65 this year. They are going to retire sooner or later. Get used to it. The household survey shows that the number of people working grew by 2.8 million YoY. That's not bad.

So far this quarter, rail is sticking to its pancake flat YoY pattern. But the economy could be picking up steam (and probably is) relative to the first quarter - we're just not going to turn in a nice large growth quarter in Q2 2015, whereas we did in 2014.

GDP in Q1 was mildly negative, which will show up later in revisions. So far it looks like this quarter will be mildly positive. Motor vehicle sales were a touch disappointing in April.

So right now, most the reports are pretty consistent with Employment - manufacturing slow or flat, services somewhat better, construction disappointing, and all things waiting on autos. As long as autos hold up ...

The establishment survey is forecasting better construction numbers coming up due to a hefty increase in employment. 32K of the 48K shown is in the Birth/Death adjustment, which doesn't mean that it didn't happen. Still, construction employment increased which is a good sign for May.

I think May will be better on most fronts. CMI is showing weakness, but not gathering storm clouds. A cautionary note is sounded by wholesale inventory/sales ratios, but while the overall number looks worrisome, when one digs into the details it's less disturbing because a decent amount of the seeming overage is in petroleum.I am a little concerned about grocery sales in this report - that's the line I am watching. They shouldn't have been that low in March. Maybe it will be revised up.

I expect fracking work to start picking up this summer. That should help us.

Autos - eh, I don't know. They are beginning to look a little topped out, but maybe we'll get our second wind this summer. Construction always generates truck sales, and there is probably some incentive room.

The two month household is 236 thousand. The monthly average for establishment is much higher, so I expect downward establishment revisions later. But still, not bad.

CMI for April was released with very substantial upward revisions for Feb/March. It is still on a declining pattern but now out of the into-the-wall version we saw last month. It is weaker YoY, but VERY IMPORTANTLY, now shows an uptick in credit granted for April.

The economy is weak and we won't see a great second quarter, but it's not flatlining.

The major weakness in the economy can be seen in the establishment survey, giving average hourly wages YoY having increased by 53 cents an hour. Doesn't buy you much! So there's tightness on the consumption end. However the employee-population ratio increased from 58.9 to 59.3 over the year, although it has been static for the last few months.

I see further ominous Drudge headlines about all the people not working. Well, we are going to see the retirees in our overall numbers, because all the people born through 1950 are either 65 or going to turn 65 this year. They are going to retire sooner or later. Get used to it. The household survey shows that the number of people working grew by 2.8 million YoY. That's not bad.

So far this quarter, rail is sticking to its pancake flat YoY pattern. But the economy could be picking up steam (and probably is) relative to the first quarter - we're just not going to turn in a nice large growth quarter in Q2 2015, whereas we did in 2014.

GDP in Q1 was mildly negative, which will show up later in revisions. So far it looks like this quarter will be mildly positive. Motor vehicle sales were a touch disappointing in April.

So right now, most the reports are pretty consistent with Employment - manufacturing slow or flat, services somewhat better, construction disappointing, and all things waiting on autos. As long as autos hold up ...

The establishment survey is forecasting better construction numbers coming up due to a hefty increase in employment. 32K of the 48K shown is in the Birth/Death adjustment, which doesn't mean that it didn't happen. Still, construction employment increased which is a good sign for May.

I think May will be better on most fronts. CMI is showing weakness, but not gathering storm clouds. A cautionary note is sounded by wholesale inventory/sales ratios, but while the overall number looks worrisome, when one digs into the details it's less disturbing because a decent amount of the seeming overage is in petroleum.I am a little concerned about grocery sales in this report - that's the line I am watching. They shouldn't have been that low in March. Maybe it will be revised up.

I expect fracking work to start picking up this summer. That should help us.

Autos - eh, I don't know. They are beginning to look a little topped out, but maybe we'll get our second wind this summer. Construction always generates truck sales, and there is probably some incentive room.

{kind=link}