MaxedOutMama

MaxedOutMama

Friday, March 12, 2010

Nobody Reads The Reports

That describes so much about our country's problems...

Bloomberg:

Let's take a look at the Jan-Feb 2010 change as compared to Jan-Feb of 2009. That total (see Table 1B in the release) grew a respectable 3.4%.

Now let's look at the Titanic graph which breaks down that 3.4% (nominal) gain by category:

Start humming "Nearer My God To Thee", because over 60% of the increase was in gasoline sales, which are pretty much flat in real terms.

People spent more at non-store retailers (catalog and online). Possibly that has something to do with all the sales tax hikes.

People spent more at pharmacies, and on groceries. People spent slightly more at auto dealers (+0.9%), which appears to be a real decrease? People did spend more on clothing, etc at general merchandise (+3.2%).

Given that the recession officially started over two years ago, at this point one would be expecting more of a rebound. These numbers are not good - what matters for the future growth of the economy are real increases and a divergence of spending into multiple channels, which tends to create new jobs. Grocery stores increased 2.3%; the food and beverage category (basically food plus alcohol) racked up a 2.1% increase. That is another indicator of tight money.

In general, real retail sales have to increase more than the population before the economy grows. Here we should check in with the last CPI release (January) to get a feel for what that YoY Jan+Feb of 3.4% really means. First, the headline CPI-W 12 month increase for January was 3.3%, so right there contemplation ensues. Apparel was +1.2%. Motor fuel and gasoline + 50% (this will be a bit less in Feb). Food at home dropped 2%, whereas food away from home rose 1.6%. Medical care commodities (includes drugs) rose 3.5%. New vehicles rose 4.0%; used vehicles rose 11.6%.

Overall, we are still going nearly sideways in real retail sales. This does not imply growth.

This is particularly worrisome because according to this week's reports, we are right at the end of the inventory cycle and now most growth has to come from a steady flow of retail sales. These reports include:

Manufacturing and Trade Inventories/Sales:

Manufacturing shipments, inventories and orders. The most significant part of the preliminary were the shipment trends for primary and fabricated metals, which indicate that we have cleared the initial inventory cycle.

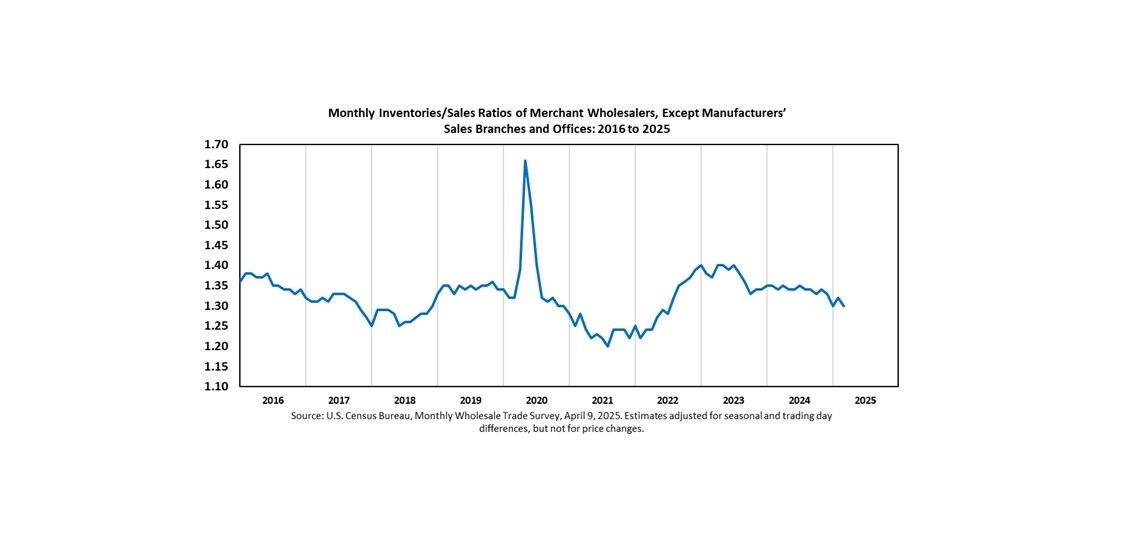

Monthly Wholesale Inventories/Sales:

Looking at the detail in this report, the negative YoY January sales numbers for lumber, metals and machinery leaped out.

One can look at the graphs above and just see that we have cleared inventory. If retail sales were rising, growth would increase. If retail sales are flat, growth will be flat. So we'd better hope that March's retail report is a bit more vivacious!

PS: Please see also two excellent CR posts covering the same themes, with nice graphs and probably clearer explanations.

Bloomberg:

Sales at U.S. retailers unexpectedly climbed in February as shoppers braved blizzards to get to the malls, signaling consumers will contribute more to economic growth. Purchases increased 0.3 percent, the fourth gain in the past five months, Commerce Department figures showed today in Washington. Figures for the prior two months were revised down, taking some of the shine off of today’s data. Sales excluding autos rose 0.8 percent, exceeding all estimates.What a remarkable vision - desperate shoppers climbing over three feet snowdrifts to get to their local mall. Does it have anything to do with reality?

Let's take a look at the Jan-Feb 2010 change as compared to Jan-Feb of 2009. That total (see Table 1B in the release) grew a respectable 3.4%.

Now let's look at the Titanic graph which breaks down that 3.4% (nominal) gain by category:

Start humming "Nearer My God To Thee", because over 60% of the increase was in gasoline sales, which are pretty much flat in real terms.

People spent more at non-store retailers (catalog and online). Possibly that has something to do with all the sales tax hikes.

People spent more at pharmacies, and on groceries. People spent slightly more at auto dealers (+0.9%), which appears to be a real decrease? People did spend more on clothing, etc at general merchandise (+3.2%).

Given that the recession officially started over two years ago, at this point one would be expecting more of a rebound. These numbers are not good - what matters for the future growth of the economy are real increases and a divergence of spending into multiple channels, which tends to create new jobs. Grocery stores increased 2.3%; the food and beverage category (basically food plus alcohol) racked up a 2.1% increase. That is another indicator of tight money.

In general, real retail sales have to increase more than the population before the economy grows. Here we should check in with the last CPI release (January) to get a feel for what that YoY Jan+Feb of 3.4% really means. First, the headline CPI-W 12 month increase for January was 3.3%, so right there contemplation ensues. Apparel was +1.2%. Motor fuel and gasoline + 50% (this will be a bit less in Feb). Food at home dropped 2%, whereas food away from home rose 1.6%. Medical care commodities (includes drugs) rose 3.5%. New vehicles rose 4.0%; used vehicles rose 11.6%.

Overall, we are still going nearly sideways in real retail sales. This does not imply growth.

This is particularly worrisome because according to this week's reports, we are right at the end of the inventory cycle and now most growth has to come from a steady flow of retail sales. These reports include:

Manufacturing and Trade Inventories/Sales:

Manufacturing shipments, inventories and orders. The most significant part of the preliminary were the shipment trends for primary and fabricated metals, which indicate that we have cleared the initial inventory cycle.

Monthly Wholesale Inventories/Sales:

Looking at the detail in this report, the negative YoY January sales numbers for lumber, metals and machinery leaped out.

One can look at the graphs above and just see that we have cleared inventory. If retail sales were rising, growth would increase. If retail sales are flat, growth will be flat. So we'd better hope that March's retail report is a bit more vivacious!

PS: Please see also two excellent CR posts covering the same themes, with nice graphs and probably clearer explanations.

Comments:

<< Home

Connecting economic growth to global prosperity becomes oxymoronic as time goes on. The economy cannot grow forever, especially when the richest upper crust are in financial auto pilot and the mere act of breathing creates more wealth for the ultra wealthy than than all other economic classes combined.

The above will only change when interest rate payout dividends are reversed. The more one deposits, the less interest they make, not more.

People with 100,000 dollars or less in deposits should be getting 7% interest. from 100,000 to 500,000, 6%, from 500,000 to 1,000,000, 5%,

from 1,000,000 to 5,000,000 4%, from 5,000,000 to 10,000,000, 3.5%, 10,000,000 to 100,000,000, 3%.

One billion and over 2%, 2 billion and over 1%.

This would res hift monies more evenly, which would actually be a good thing at this point.

The above will only change when interest rate payout dividends are reversed. The more one deposits, the less interest they make, not more.

People with 100,000 dollars or less in deposits should be getting 7% interest. from 100,000 to 500,000, 6%, from 500,000 to 1,000,000, 5%,

from 1,000,000 to 5,000,000 4%, from 5,000,000 to 10,000,000, 3.5%, 10,000,000 to 100,000,000, 3%.

One billion and over 2%, 2 billion and over 1%.

This would res hift monies more evenly, which would actually be a good thing at this point.

The media being advertising driven normally pushes a positive spin on financial reporting. During the Vietnam War the term "light at the end of the tunnel" was often used by the administration and media, and we all know how the war actually ended.

M.O.M.,

Nobody Reads The Reports

That's why misleading headlines are so effective!

Nobody Reads The Reports

That's why misleading headlines are so effective!

# posted by  : 2:18 PM

: 2:18 PM

: 2:18 PM

MOM,

"Now let's look at the Titanic graph which breaks down that 3.4%..."

Your chart is certainly "listing" reasons to be concerned.

From 2007...

Stricken Antarctic ship evacuated

http://news.bbc.co.uk/2/hi/uk_news/7108835.stm

The M/S Explorer has been listing for hours

As seen in the picture, the ice to ship ratio was not entirely favorable.

"Now let's look at the Titanic graph which breaks down that 3.4%..."

Your chart is certainly "listing" reasons to be concerned.

From 2007...

Stricken Antarctic ship evacuated

http://news.bbc.co.uk/2/hi/uk_news/7108835.stm

The M/S Explorer has been listing for hours

As seen in the picture, the ice to ship ratio was not entirely favorable.

Nothing more than income tax refunds being spent.

Come April, when those that have to pay get hit,

sales will drop. Not enough layers of the economy

to increase the velocity of money.

Sporkfed

Come April, when those that have to pay get hit,

sales will drop. Not enough layers of the economy

to increase the velocity of money.

Sporkfed

# posted by : 3:30 PM

: 3:30 PM

This will come as no great surprise, but Larry Kudlow just referred to retail sales as a terrific sign.

The economy cannot grow forever, especially when the richest upper crust are in financial auto pilot and the mere act of breathing creates more wealth for the ultra wealthy than than all other economic classes combined.

Well, Alessandro, that's about the dumbest thing I've read on the Internets in months.

Well, Alessandro, that's about the dumbest thing I've read on the Internets in months.

Mark, my view is that for every Krugman, there is an equal and partisan-opposite Kudlow ...

Two V's make a W. Three V's shouldn't trouble you. Or is that a V and an L?

Two V's make a W. Three V's shouldn't trouble you. Or is that a V and an L?

John - I think that's why I stopped reading either quite some time ago.

IMO economics is a science, but it is always a science with a lot of unknowns, and very often a science with a majority of unknowns. Approached with that in mind, one can generate useful results as long one is willing to say "I don't know" a lot. Without the willingness to acknowledge that one is a fool who knows nothing on a fairly frequent basis, I think one is likely to do more harm than good.

I think that individual and national ideologies should guide proposals about how to cope with reality, but that the process of determining (or, in economics, estimating) reality must be ideologically neutral. So when you get your ideology into it, you get your sensor readings all messed up.

One of my brothers sent me a Kudlow article from last year that really makes Krugman look great. I was never able to figure out what the article was about really - it made that little sense except that he wanted to complain about Obama. But the conclusion was that US citizens ought to be able to spend and save as much as they liked.

How that works in reality I do not know. I have rarely met anyone who is both spending all they liked and saving all they liked. Personally I would like to save 500% of my current income and spend 600% of it. Perhaps that is where the urge to insanely borrow comes in....

If you look at both sides of the ideological spectrum, they both now seem to be advocating policies that would drive our national borrowing up massively. Most of the difference is how they want to spend it - both want to BORROW it.

But neither ideological wing appears to be able to come to grips with the ugly reality that we are reaching our limits of borrowing, so advocating borrowing much more in the near future is likely to destroy THEIR OWN FUTURE PROSPECTS. They are advocating self-defeat of THEIR OWN AGENDA in a decade or at most fifteen years.

That is where the broader public must step in.

IMO economics is a science, but it is always a science with a lot of unknowns, and very often a science with a majority of unknowns. Approached with that in mind, one can generate useful results as long one is willing to say "I don't know" a lot. Without the willingness to acknowledge that one is a fool who knows nothing on a fairly frequent basis, I think one is likely to do more harm than good.

I think that individual and national ideologies should guide proposals about how to cope with reality, but that the process of determining (or, in economics, estimating) reality must be ideologically neutral. So when you get your ideology into it, you get your sensor readings all messed up.

One of my brothers sent me a Kudlow article from last year that really makes Krugman look great. I was never able to figure out what the article was about really - it made that little sense except that he wanted to complain about Obama. But the conclusion was that US citizens ought to be able to spend and save as much as they liked.

How that works in reality I do not know. I have rarely met anyone who is both spending all they liked and saving all they liked. Personally I would like to save 500% of my current income and spend 600% of it. Perhaps that is where the urge to insanely borrow comes in....

If you look at both sides of the ideological spectrum, they both now seem to be advocating policies that would drive our national borrowing up massively. Most of the difference is how they want to spend it - both want to BORROW it.

But neither ideological wing appears to be able to come to grips with the ugly reality that we are reaching our limits of borrowing, so advocating borrowing much more in the near future is likely to destroy THEIR OWN FUTURE PROSPECTS. They are advocating self-defeat of THEIR OWN AGENDA in a decade or at most fifteen years.

That is where the broader public must step in.

PS: I do not want the V and the L. I think we should all start thinking hard about that potential L. The W we could stand; an L with our deficits would be truly awful.

Agreed, we can stand two V's or even three V's, but the L will ruin us. Unfortunately, the Krugman and Kudlow Kool-Aid crowd that runs things in DC will ruin us even if the L doesn't.

MOM,

"Approached with that in mind, one can generate useful results as long one is willing to say "I don't know" a lot. Without the willingness to acknowledge that one is a fool who knows nothing on a fairly frequent basis, I think one is likely to do more harm than good."

"I don't know" was a favorite saying of mine as a lead software engineer. It really helped my career too. It doesn't take many wrong answers for management to distrust a programmer.

We needed some puzzle generation programming done out of house. I wrote up a design document. The outside programmers actually laughed at my requirements. They said what I asked of them was trivial.

That "trivial" fixed bid task turned into a nightmare for them. They went from making me look bad in front of my boss to making me look very good. She was especially pleased that I had thought to put it in writing that it can't take more than 8 hours to generate the puzzles. She asked me how I knew it would take that long. "I didn't know." All I knew was that if their solution took a supercomputer a year then we'd no doubt be shipping the product very late.

"Approached with that in mind, one can generate useful results as long one is willing to say "I don't know" a lot. Without the willingness to acknowledge that one is a fool who knows nothing on a fairly frequent basis, I think one is likely to do more harm than good."

"I don't know" was a favorite saying of mine as a lead software engineer. It really helped my career too. It doesn't take many wrong answers for management to distrust a programmer.

We needed some puzzle generation programming done out of house. I wrote up a design document. The outside programmers actually laughed at my requirements. They said what I asked of them was trivial.

That "trivial" fixed bid task turned into a nightmare for them. They went from making me look bad in front of my boss to making me look very good. She was especially pleased that I had thought to put it in writing that it can't take more than 8 hours to generate the puzzles. She asked me how I knew it would take that long. "I didn't know." All I knew was that if their solution took a supercomputer a year then we'd no doubt be shipping the product very late.

MoM,

Seems to me that the optimists would say, "the inventory to sales is down to its lows, so companies have finished drawing down inventories, which means they now have to restock them."

I see it the way you put it (that a "normal" ratio implies the adjustment is over), but I can understand the differing view point.

How would you answer the view that a low ratio means restocking is needed? Another way to pose the question is, how should this indicator behave over the course of the cycle? The data is inconclusive as cyclical influences seem to have been swamped by the secular trend towards a lower ratio.

Seems to me that the optimists would say, "the inventory to sales is down to its lows, so companies have finished drawing down inventories, which means they now have to restock them."

I see it the way you put it (that a "normal" ratio implies the adjustment is over), but I can understand the differing view point.

How would you answer the view that a low ratio means restocking is needed? Another way to pose the question is, how should this indicator behave over the course of the cycle? The data is inconclusive as cyclical influences seem to have been swamped by the secular trend towards a lower ratio.

# posted by : 2:11 PM

: 2:11 PM

David - I want to be an optimist, but right now the world is filled with caution. It's true they have to restock, but only at the rate at which the stuff moves out the door.

The reason why I started with retail sales and the graph about where we are registering YoY growth in retail is because from now on growth will be dependent on those sales. The inventory reading is somewhat neutral - all it means is that now growth will come from the sales trend rather than the whole inventory cycle.

Because the prior trend was down I don't think the current levels are a poor indicator. They do look somewhat cautious, don't they?

Spring is coming. Hopefully people will be paying less for heat, and the cooling season won't kick in for a few months, providing a bit more margin. We have to hope that this little bonus along with the Census hiring and the real improvement over the last six months will keep us nudging along in growth territory over the next six months.

I keep wanting to claim that car sales have to pick up, because the car fleet is aging. But I remember the 70s and the 80s too well. There were an awful lot of very old vehicles on the roads back then, and today most cars are somewhat better in quality.

Still, time is our friend in some ways at least.

Post a Comment

The reason why I started with retail sales and the graph about where we are registering YoY growth in retail is because from now on growth will be dependent on those sales. The inventory reading is somewhat neutral - all it means is that now growth will come from the sales trend rather than the whole inventory cycle.

Because the prior trend was down I don't think the current levels are a poor indicator. They do look somewhat cautious, don't they?

Spring is coming. Hopefully people will be paying less for heat, and the cooling season won't kick in for a few months, providing a bit more margin. We have to hope that this little bonus along with the Census hiring and the real improvement over the last six months will keep us nudging along in growth territory over the next six months.

I keep wanting to claim that car sales have to pick up, because the car fleet is aging. But I remember the 70s and the 80s too well. There were an awful lot of very old vehicles on the roads back then, and today most cars are somewhat better in quality.

Still, time is our friend in some ways at least.

<< Home

![]()