MaxedOutMama

MaxedOutMama

Thursday, January 13, 2011

An Awful Post

This, folks, is the post I never wanted to write. This is the post that makes me want to quit blogging.

Expletive, expletive, expletive. I am sorry, but here are the numbers:

A) Medicare wage tax for December.

I got back from the hospital (routine appointment for the Chief) about 10:45 and therefore got a late start on the day's news. After the bad Treasury figures, I gulped, reminded myself that at least the pace of initial claims had dropped, and marched my disconsolate butt over to the Dept of Labor's website.

And that is when things truly got ominous, because....

In late December 2009 initial claims were reported much lower than they really were. Later the DOL folks revised the figures, and it is the revised figures everyone has been working off.

But if you look at the original releases for a true YoY comparison:

DOL released a statement attributing some of the jump to special factors, such as a delay in initial claims processing. This is true, but the same appeared for last year which is why DOL went back and revised the numbers quite significantly.

It's not a strong trajectory at the moment. Maybe by the end of January the flukiness will straighten out and we'll find that the YoY comparisons look better. Maybe not. Right now it does not appear that the January employment report is going to be all that encouraging.

Tomorrow there is a plethora of nuts and bolts releases. December retail sales, the CPI, Industrial Production and Business Inventories will clarify. Right now it appears that production companies are in something of a squeeze - they are paying higher materials costs but don't want or are not able to pass all those costs along to the end-buyer. This may be affecting employment.

I find the current round of reports puzzling. Freight was pretty good in December, and the economy should be generating more jobs than it is.

PS: Regarding the nominal vs real income thang:

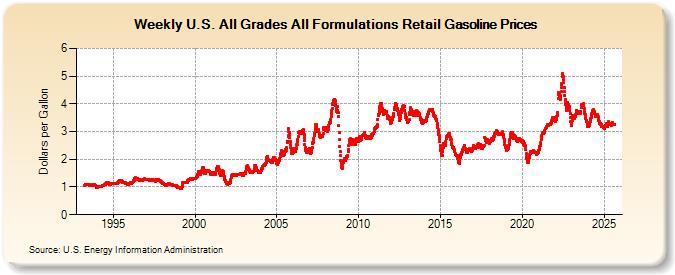

Fortunately, gas prices at current levels caused absolutely no harm to the economy in 2007:

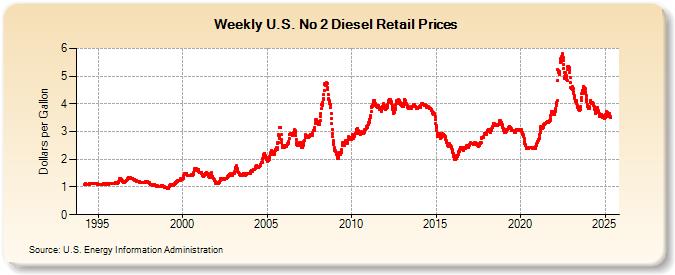

Nor did diesel prices cause any problem back then. I'm sure the last few weeks can have no negative implications whatsoever:

And food prices at 2008 levels caused nothing but a few measly riots back then in Countries That Do Not Count, so I'm sure we need not be concerned now. That is, unless you are an unemployed person who has lost or is about to lose unemployment benefits. Those food stamps won't be going as far, will they?

And I'm sure that stocks are a great value now, because gee, the indexes are still way below their previous peaks (look at the five year) and even Mark has to agree that there are great, great values out there. Personally I get nervous when I look at stock indexes and the little Walmart smiley face thingie starts bouncing up and down. It's looking like another sell season later this year. There's some space left for the nonce. The Fed is not taking their foot off the gas pedal until we pry their cold, dead feet from the floor of the Tin Lizzie or Congress wakes up and gets real, which clearly is not happening this year. (That sentence should get me another of those FBI site visits.)

One of the beyootiful things about high finance (the type you get when everyone involved is high) is that when the Fed opens the floodgate, stocks WILL go up. For a while. It's particularly amusing to watch the prices go up as sales and profits decrease. The recession started between the 2nd and 3rd quarter of 2007, when tax receipts started their epic fall. And that is when stocks reached their peak.

A good site to track trucking stuff is here. It's not just tonnage. It's also capacity, etc. EIA petroleum total demand is always worth a look. It runs a few months behind. This is really product supplied, but if you average a few months you get the overall demand figure. AAR is the site for rail. It is also a very slow-loading site, so early in the morning or late at night.

Expletive, expletive, expletive. I am sorry, but here are the numbers:

A) Medicare wage tax for December.

2009:Not only did the YoY decline again, but it is worse than November's decline (about 1.2%). This means that total wages and salaries paid is still declining compared to a year ago and the gap kept widening. The second ironclad conclusion is that the real decline is larger. Above you see only the nominal decline. And lastly, I must remind you that Social Security recipients had no increase again this year, so their real incomes are declining, except for those few who have money in stuff like stocks.

Wages: 17,018

Self: 165

2010:

Wages: 16,788 (-1.35%)

Self: 170

I got back from the hospital (routine appointment for the Chief) about 10:45 and therefore got a late start on the day's news. After the bad Treasury figures, I gulped, reminded myself that at least the pace of initial claims had dropped, and marched my disconsolate butt over to the Dept of Labor's website.

And that is when things truly got ominous, because....

In late December 2009 initial claims were reported much lower than they really were. Later the DOL folks revised the figures, and it is the revised figures everyone has been working off.

But if you look at the original releases for a true YoY comparison:

Dec 26, 2009 Advance:Now this year's sequence:

SA: 432,000

NSA: 557,155

Jan 2, 2010 Advance:

SA: 434,000

NSA: 645,571

Jan 9, 2010 Advance:

SA: 444,000

NSA: 801,086

Dec 25,2010 Advance:An unpleasant trajectory is evident. It's also evident from comparing recent household survey numbers to the initial claims numbers that fewer job losers are filing for initial claims because apparently more of them are in the temp/contract categories who do not qualify for unemployment.

SA: 388,000

NSA: 521,834

Jan 1, 2011 Advance:

SA: 409,000

NSA: 577,279

Jan 8, 2011 Advance:

SA: 445,000

NSA: 770,413

DOL released a statement attributing some of the jump to special factors, such as a delay in initial claims processing. This is true, but the same appeared for last year which is why DOL went back and revised the numbers quite significantly.

It's not a strong trajectory at the moment. Maybe by the end of January the flukiness will straighten out and we'll find that the YoY comparisons look better. Maybe not. Right now it does not appear that the January employment report is going to be all that encouraging.

Tomorrow there is a plethora of nuts and bolts releases. December retail sales, the CPI, Industrial Production and Business Inventories will clarify. Right now it appears that production companies are in something of a squeeze - they are paying higher materials costs but don't want or are not able to pass all those costs along to the end-buyer. This may be affecting employment.

I find the current round of reports puzzling. Freight was pretty good in December, and the economy should be generating more jobs than it is.

PS: Regarding the nominal vs real income thang:

Fortunately, gas prices at current levels caused absolutely no harm to the economy in 2007:

Nor did diesel prices cause any problem back then. I'm sure the last few weeks can have no negative implications whatsoever:

And food prices at 2008 levels caused nothing but a few measly riots back then in Countries That Do Not Count, so I'm sure we need not be concerned now. That is, unless you are an unemployed person who has lost or is about to lose unemployment benefits. Those food stamps won't be going as far, will they?

And I'm sure that stocks are a great value now, because gee, the indexes are still way below their previous peaks (look at the five year) and even Mark has to agree that there are great, great values out there. Personally I get nervous when I look at stock indexes and the little Walmart smiley face thingie starts bouncing up and down. It's looking like another sell season later this year. There's some space left for the nonce. The Fed is not taking their foot off the gas pedal until we pry their cold, dead feet from the floor of the Tin Lizzie or Congress wakes up and gets real, which clearly is not happening this year. (That sentence should get me another of those FBI site visits.)

One of the beyootiful things about high finance (the type you get when everyone involved is high) is that when the Fed opens the floodgate, stocks WILL go up. For a while. It's particularly amusing to watch the prices go up as sales and profits decrease. The recession started between the 2nd and 3rd quarter of 2007, when tax receipts started their epic fall. And that is when stocks reached their peak.

A good site to track trucking stuff is here. It's not just tonnage. It's also capacity, etc. EIA petroleum total demand is always worth a look. It runs a few months behind. This is really product supplied, but if you average a few months you get the overall demand figure. AAR is the site for rail. It is also a very slow-loading site, so early in the morning or late at night.

Comments:

<< Home

I had the same read on the medicare receipts as you did. Hard to understand all the bullishness and strength in retail when incomes are going nowhere.

As an aside, how do you deal with these huge prior year adjustments that frequently show up on these reports? Makes me wonder if the current numbers are really comparable.

As an aside, how do you deal with these huge prior year adjustments that frequently show up on these reports? Makes me wonder if the current numbers are really comparable.

# posted by  : 9:36 AM

: 9:36 AM

: 9:36 AM

If a period has huge adjustments, I mark it on a calendar along with other exceptional circumstances like catastrophes, and then I modify the comparisons, or wait until a truly comparable period arrives. Error bars are important, and every time series will run into periods that are not truly reflective.

I don't know how to do it otherwise. Comparing the raw data helps to compensate a bit, but the reality is that we won't really know until the end of January.

We're still seeing some base-level improvement, but the correlation with the employment reports is weakening.

In February, Medicare wage receipts won't be valid because there was a large snow effect.

My jaw just dropped on those wage receipts. I expected to see a YoY drop, but on the order of three quarters of a percentage point. Not this.

I don't know how to do it otherwise. Comparing the raw data helps to compensate a bit, but the reality is that we won't really know until the end of January.

We're still seeing some base-level improvement, but the correlation with the employment reports is weakening.

In February, Medicare wage receipts won't be valid because there was a large snow effect.

My jaw just dropped on those wage receipts. I expected to see a YoY drop, but on the order of three quarters of a percentage point. Not this.

QE2 brings the credit spurt pushing auto and home sales with so called once in a lifetime credit terms but the basic longterm labor trends in the economy continue. Local political leaders continue to push various construction bond measures for transportation/schools but otherwise the building trades have small remodel projects but a local city has finally invited Wall Mart in thereby insuring the destruction of its small retail really a zero sum game at best. Pushing greater debt levels onto the consumer via slack credit terms ends in tears nor does increased M$A activity provide any meaningful jobs other then spike up a stock price. Economic thinking needs a jolt of reality and it doesn't seem to be coming anytime soon.

I'm trying to understand the reasonably good retail numbers we saw for December, in light of the decrease in wages. Is this an effect of the divergence between low-end goods and high-end goods? Meaning retailers are hurting on the low end items, but the higher-dollar items (that provide most of the revenue, if not most of the profit) are doing just fine, until trickle-up poverty works its way through the system.

Neil,

FWIW, I saw a recent interview with a long-time retail analyst who reasoned that the top 30% of the population is driving retail sales. Here is where you see a true wealth effect as stock market gains effect consumer behavior somewhat. It also explains why you see such great comps for high-end retailers and flat to negative comps for Walmart.

FWIW, I saw a recent interview with a long-time retail analyst who reasoned that the top 30% of the population is driving retail sales. Here is where you see a true wealth effect as stock market gains effect consumer behavior somewhat. It also explains why you see such great comps for high-end retailers and flat to negative comps for Walmart.

# posted by : 11:04 AM

: 11:04 AM

Neil - after the December retail report, we'll know more. I really want to see that.

With the caveat, of course, that it is nominal and that there is some margin of error in the advance report.

A very bright spot for retail and for production has been autos. I think this is structural, given the increasing age of licensed cars. Another factor is that the burden of debt on consumers has been lightened. A lot of revolving credit is gone - we are back to 2004 levels as of November. Many mortgages are being paid at lower rates, releasing more income to be spent, and many mortgages have gone to the graveyard.

Because auto buying is very related to credit, it is related to income. However auto credit has been loosening lately.

In any case, after tomorrow's report I'll run through a three month sequence to look at patterns.

The strongest long-term forecasting method I know is to concentrate on incomes. It is very important to also concentrate on company incomes. If company incomes are tightening, companies usually reduce their purchases and try to cut costs, which tends to produce a drop in other company incomes, and which tends to propagate through to employee incomes.

Export prices increased more than import prices. The Fed's attempt to devalue the US dollar is producing some positive effect for at least some companies.

Will that effect and delayed consumption overpower the trickle-up effect of reduced real incomes for retirees and the bottom 40% of wage earners? We'll have to see.

Some of the Medicare wage disparity with freight undoubtedly results from cuts in government employment and the very significant pay disparity between public and private workers.

It certainly is going to make the Social Security/Medicare income/outgo gap look very bad in 2011.

With the caveat, of course, that it is nominal and that there is some margin of error in the advance report.

A very bright spot for retail and for production has been autos. I think this is structural, given the increasing age of licensed cars. Another factor is that the burden of debt on consumers has been lightened. A lot of revolving credit is gone - we are back to 2004 levels as of November. Many mortgages are being paid at lower rates, releasing more income to be spent, and many mortgages have gone to the graveyard.

Because auto buying is very related to credit, it is related to income. However auto credit has been loosening lately.

In any case, after tomorrow's report I'll run through a three month sequence to look at patterns.

The strongest long-term forecasting method I know is to concentrate on incomes. It is very important to also concentrate on company incomes. If company incomes are tightening, companies usually reduce their purchases and try to cut costs, which tends to produce a drop in other company incomes, and which tends to propagate through to employee incomes.

Export prices increased more than import prices. The Fed's attempt to devalue the US dollar is producing some positive effect for at least some companies.

Will that effect and delayed consumption overpower the trickle-up effect of reduced real incomes for retirees and the bottom 40% of wage earners? We'll have to see.

Some of the Medicare wage disparity with freight undoubtedly results from cuts in government employment and the very significant pay disparity between public and private workers.

It certainly is going to make the Social Security/Medicare income/outgo gap look very bad in 2011.

dis737 - It's definitely restricted to the top 50% of the population, and maybe when you separate out autos and furnishings it might be the top 30%.

The problem is that if this is true, the end result could be a new downturn. The incomes of the top 30% are really dependent upon the spending of the bottom 50%.

It's also true that not every American is a spendthrift, and that we have an older population with some savings, so that some delayed consumption effect could be picking up and carrying us through.

Among the things I want to check in tomorrow's CPI is the disparity between new and used car inflation.

The Fed can goose stocks any time it wants by doing what it is doing, but the problem is that there is a natural end point. It is not an eternally open system. For a while, yes. Then it all catches up with you.

Because a lot of families did their Christmas shopping earlier, December's comps may not be valid for the economy as a whole.

The problem is that if this is true, the end result could be a new downturn. The incomes of the top 30% are really dependent upon the spending of the bottom 50%.

It's also true that not every American is a spendthrift, and that we have an older population with some savings, so that some delayed consumption effect could be picking up and carrying us through.

Among the things I want to check in tomorrow's CPI is the disparity between new and used car inflation.

The Fed can goose stocks any time it wants by doing what it is doing, but the problem is that there is a natural end point. It is not an eternally open system. For a while, yes. Then it all catches up with you.

Because a lot of families did their Christmas shopping earlier, December's comps may not be valid for the economy as a whole.

I watched Meredith Whitney on CNBC yesterday.

She stuck by her call on municipal defaults - controversial to Calculated Risk, not because of the predicted frequency of default but because of the degree.

They pressed her on equity markets, and she vaguely concluded that the bear will be back in the spring because the US consumer simply can't keep it up.

She stuck by her call on municipal defaults - controversial to Calculated Risk, not because of the predicted frequency of default but because of the degree.

They pressed her on equity markets, and she vaguely concluded that the bear will be back in the spring because the US consumer simply can't keep it up.

# posted by : 2:55 PM

: 2:55 PM

MOM,

"...and the economy should be generating more jobs than it is."

Here's my take on it for what it is worth.

Home Equity vs. The Trade Deficit

Adjusted for inflation, we now have a $10 trillion cumulative trade deficit. That is money that has left America and has created jobs elsewhere.

It isn't just China and India. We even import twice as much from the PIIGS as we export to them.

Trading with the PIIGS

"...and the economy should be generating more jobs than it is."

Here's my take on it for what it is worth.

Home Equity vs. The Trade Deficit

Adjusted for inflation, we now have a $10 trillion cumulative trade deficit. That is money that has left America and has created jobs elsewhere.

It isn't just China and India. We even import twice as much from the PIIGS as we export to them.

Trading with the PIIGS

Another downer, the dry Baltic index:

http://www.minyanville.com/dailyfeed/the-baltic-dry-index-is/

Oil and gas prices are another headwind. Ag prices as well.

I don't get the people who think rising energy and ag prices are a sign of recovery.

So, is the market rise about to end? The tea leaves are certainly the color of a brown bear.

http://www.minyanville.com/dailyfeed/the-baltic-dry-index-is/

Oil and gas prices are another headwind. Ag prices as well.

I don't get the people who think rising energy and ag prices are a sign of recovery.

So, is the market rise about to end? The tea leaves are certainly the color of a brown bear.

# posted by : 3:30 PM

: 3:30 PM

Hearing rumors that the Post Office is going to

offer an early out to some employees and possibly

a RIF (layoff). This would impact every town in the

country by reducing the number of middle class jobs.

I'm guessing that the FEDGov wants to create some

openings for returning vets and the Post Office has

long been a safety valve for their employment.

offer an early out to some employees and possibly

a RIF (layoff). This would impact every town in the

country by reducing the number of middle class jobs.

I'm guessing that the FEDGov wants to create some

openings for returning vets and the Post Office has

long been a safety valve for their employment.

# posted by : 3:44 PM

: 3:44 PM

I did my part to share your doom and gloom today.

Jumping the Curbs!

I also found one of the most painful looking videos to go with it.

Jumping the Curbs!

I also found one of the most painful looking videos to go with it.

MOM,

How many people have gotten out of the job market and started to take Social Security early? I know this is not productive income, but we are concerned that today's numbers show there are less dollars for spending. An increase in total social security outlays, while a long term problem, might mitigate these numbers? Probably not enough to fix anything, but maybe enough to help. Maybe?

How many people have gotten out of the job market and started to take Social Security early? I know this is not productive income, but we are concerned that today's numbers show there are less dollars for spending. An increase in total social security outlays, while a long term problem, might mitigate these numbers? Probably not enough to fix anything, but maybe enough to help. Maybe?

# posted by : 5:27 PM

: 5:27 PM

This is the one I like, Mark.

Buy now or forever be priced out!

Meanwhile, the price of gas has reached the point at which it crashed the economy in 2007.

Buy now or forever be priced out!

Meanwhile, the price of gas has reached the point at which it crashed the economy in 2007.

Anon - yes, there has been a clear upward trend in retirements, many early.

In June 2010, all types of Social Security recipients including disabled numbered 53,397,574.

Looking at the most recent figures (November 2010), the new total is 53,934,000. This is not a huge number - the last I looked monthly benefits were about 1.3K for primary retirees.

I am surprised by how little the number has recently grown, but my guess is that after people fall off unemployment there will be another spike in 2011.

Link 1, look at Table 2.

Link 2, look at graph and the following table.

One of the reasons I was so interested in the study on the workers who had lost jobs was that I wanted a hint as to the likely retirement trajectory in 2011 and 2012.

In December 2009 the total OASDI recipients were 52,522,819, (Scroll down to table 5.A1). So we are about on pace to rack up about 1.5 million more recipients this year.

If you scroll down a little more on that last link, you'll see a table for 2009 beneficiaries by age. As you can see, there is a significant early retirement penalty. I think older people with savings are choosing to draw them down because of the increased benefit they expect when they start receiving Social Security.

I have some graphs to post from bank deposits on that topic.

I do think early retirements from state and local government employees are likely to be shooting through the roof, and that would probably be more of a consideration right now. On average, they receive far more in benefits and they can generally retire on full benefits much earlier. Also, there is some legal advantage to being retired when the cost-cutting axe starts swinging.

In June 2010, all types of Social Security recipients including disabled numbered 53,397,574.

Looking at the most recent figures (November 2010), the new total is 53,934,000. This is not a huge number - the last I looked monthly benefits were about 1.3K for primary retirees.

I am surprised by how little the number has recently grown, but my guess is that after people fall off unemployment there will be another spike in 2011.

Link 1, look at Table 2.

Link 2, look at graph and the following table.

One of the reasons I was so interested in the study on the workers who had lost jobs was that I wanted a hint as to the likely retirement trajectory in 2011 and 2012.

In December 2009 the total OASDI recipients were 52,522,819, (Scroll down to table 5.A1). So we are about on pace to rack up about 1.5 million more recipients this year.

If you scroll down a little more on that last link, you'll see a table for 2009 beneficiaries by age. As you can see, there is a significant early retirement penalty. I think older people with savings are choosing to draw them down because of the increased benefit they expect when they start receiving Social Security.

I have some graphs to post from bank deposits on that topic.

I do think early retirements from state and local government employees are likely to be shooting through the roof, and that would probably be more of a consideration right now. On average, they receive far more in benefits and they can generally retire on full benefits much earlier. Also, there is some legal advantage to being retired when the cost-cutting axe starts swinging.

MOM,

"Meanwhile, the price of gas has reached the point at which it crashed the economy in 2007."

Haven't you heard? We're far less reliant on energy now.

From December 2007:

Here's the proof!

We are reliant on sarcasm though. No doubt about that.

"Meanwhile, the price of gas has reached the point at which it crashed the economy in 2007."

Haven't you heard? We're far less reliant on energy now.

From December 2007:

Here's the proof!

We are reliant on sarcasm though. No doubt about that.

Early retirement, after a fashion, will be me. The thing to keep in mind is that a lot of these folks are being forced down into low paying or part time jobs anyway. Since you can earn a certain amount without affecting benefits, it may not look that bad to those already on the bottom. And, if you've got assets that have already been eroded, it may look like time to use it or lose it. The downside is being under the government's thumb to a certain extent, but I expect a vibrant cash economy will follow.

Yes, like others I'm pretty convinced that auto sales are thanks to a release of pent-up demand. For one thing, individuals and businesses can only defer replacement for so long, and a lot of people kept cars for several years after they would normally have replaced them because of economic conditions and concerns. That was me; I kept my old car until increasing unreliability concerns prompted replacement in April last year.

Plus, tightened credit really hurt car sales. A lot of people couldn't buy even if they wanted to, certainly not at a rate they were willing to pay. That's relaxed a lot recently.

Post a Comment

Plus, tightened credit really hurt car sales. A lot of people couldn't buy even if they wanted to, certainly not at a rate they were willing to pay. That's relaxed a lot recently.

<< Home

![]()