MaxedOutMama

MaxedOutMama

Thursday, June 23, 2011

Oh, THURSDAY

Initial claims 429,000; last week's initial claims revised up to 420,000 from 414,000. Four week moving average on initial claims is 426,250. But there was a higher-than-expected lack of reporting, so there could be big revisions next week either way.

CFNAI MA3 weakening still. June would have to be quite positive to stop the slide in this number.

Tomorrow Q1 GDP final. It looks like Q2 is going to be worse than Q1. New Home Sales later today, but why bother? It's the same old, same old bouncing on the bottom. It ain't gonna get no worse because it can't, and it doesn't seem to be able to get much better due to competition from existing home sales. Next year in Jerusalem, folks. On condos, these supply figures can't be trusted either on existing or new, because there is a lot of inventory out there that shifts from rental to sale and back in some areas.

Asia greeted the downward revisions for projected US GDP with some dismay, and commodities trading turned quite negative. Chinese prelim PMI was reported about at "stall", so that is not helping the situation, money is moving into the risk currencies like the yen, the Swiss franc, and yes, the good 'ol USD. Perhaps the ECB should have laid less stress on "risk" yesterday. The Germans are rounding up investors and having a little meeting about "voluntary" rollovers. "Zo, Hans, Ve haf vays to obtain your cooperation ..." These meetings are completely confidential.

The brightest news out there is that TEPCO has perhaps found the problem with the water filtration system and may be able to fix it. One story. Another story. Who knows? Maybe today they'll get it working, maybe not, because this more detailed story doesn't sound quite right when read with the other two.

Let's see - the Sniffies (do you realize that we fund this stuff?) are crusading against potato chips and French fries. The Ivy Medical Sniffies appear to be chasing well-paid irrelevance - just think what a tremendous help this will be to all the doctors out there who up till now, were recommending a diet of potato chips and French fries for their patients who need to lose weight.

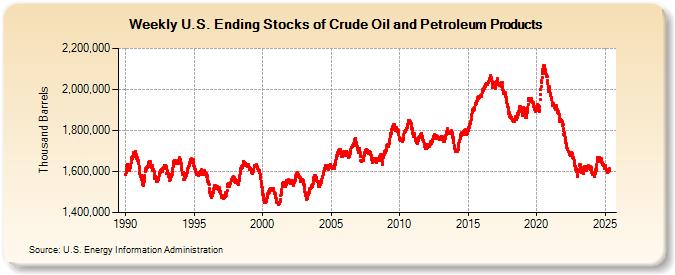

I had a good laugh over some of the oil articles. These are stocking levels:

Quite high, wouldn't you say? But even higher when one looks at consumption and capacity measures.

PS: On Meredith and munis:

Note: If it walks like a duck.....

European leading edge predictors don't look so hot. Germany is not in trouble, but there is growing wariness. Paradoxically, France is going to profit from the German decision to bag nuclear power so its economic growth trend should be adjusted upward. IEA's oil moves may not help Europe much.

CFNAI MA3 weakening still. June would have to be quite positive to stop the slide in this number.

Tomorrow Q1 GDP final. It looks like Q2 is going to be worse than Q1. New Home Sales later today, but why bother? It's the same old, same old bouncing on the bottom. It ain't gonna get no worse because it can't, and it doesn't seem to be able to get much better due to competition from existing home sales. Next year in Jerusalem, folks. On condos, these supply figures can't be trusted either on existing or new, because there is a lot of inventory out there that shifts from rental to sale and back in some areas.

Asia greeted the downward revisions for projected US GDP with some dismay, and commodities trading turned quite negative. Chinese prelim PMI was reported about at "stall", so that is not helping the situation, money is moving into the risk currencies like the yen, the Swiss franc, and yes, the good 'ol USD. Perhaps the ECB should have laid less stress on "risk" yesterday. The Germans are rounding up investors and having a little meeting about "voluntary" rollovers. "Zo, Hans, Ve haf vays to obtain your cooperation ..." These meetings are completely confidential.

The brightest news out there is that TEPCO has perhaps found the problem with the water filtration system and may be able to fix it. One story. Another story. Who knows? Maybe today they'll get it working, maybe not, because this more detailed story doesn't sound quite right when read with the other two.

Let's see - the Sniffies (do you realize that we fund this stuff?) are crusading against potato chips and French fries. The Ivy Medical Sniffies appear to be chasing well-paid irrelevance - just think what a tremendous help this will be to all the doctors out there who up till now, were recommending a diet of potato chips and French fries for their patients who need to lose weight.

I had a good laugh over some of the oil articles. These are stocking levels:

Quite high, wouldn't you say? But even higher when one looks at consumption and capacity measures.

PS: On Meredith and munis:

U.S. state and local governments will need to raise taxes by $1,398 per household every year for the next 30 years if they are to fully fund their pension systems, a study released on Wednesday said.The details vary hugely per plan. Obviously the above figures are an estimate. Some plans are in far worse shape and some are in far better shape. One rule of thumb is to look at demographics (growing or not?). The blue state government workers are about to see their worst nightmare take flesh and stalk the legislatures. This is why I posted all that stuff about the NJ plan, which cuts COLAs to eventually achieve a balance. There will be much more of these sorts of moves in many states, because many of these plans cannot be supported under any feasible scenario at all. This public pension bubble is very large indeed, but fortunately can be adjusted.

Note: If it walks like a duck.....

European leading edge predictors don't look so hot. Germany is not in trouble, but there is growing wariness. Paradoxically, France is going to profit from the German decision to bag nuclear power so its economic growth trend should be adjusted upward. IEA's oil moves may not help Europe much.

Comments:

<< Home

Gordon - I put in the stuff on Sniffies and spuds just for you.

The story of the day is not anything to do with homes, it is the crack in commodities which is really worth watching.

Let's just say the prelim Chinese PMI put a lid on it. We've broken back to the Feb range, and the sixties are the limit on crude now. The Japan/China thing is determinative.

The story of the day is not anything to do with homes, it is the crack in commodities which is really worth watching.

Let's just say the prelim Chinese PMI put a lid on it. We've broken back to the Feb range, and the sixties are the limit on crude now. The Japan/China thing is determinative.

Or you could just watch Treasury yields drop.

In the future, Europe and the US must make an agreement not to allow the ECB head and the Fed head to speak on the same day.

Between fundamentals and talking heads, the markets have been thrown into the collywobbles.

In the future, Europe and the US must make an agreement not to allow the ECB head and the Fed head to speak on the same day.

Between fundamentals and talking heads, the markets have been thrown into the collywobbles.

That $1398 per household is misleading, because not every household pays significant taxes. Based on the fact that over half the employed pay no income tax, shouldn't that figure be twice as large,at a minimum?

# posted by  : 12:50 PM

: 12:50 PM

: 12:50 PM

It would naturally be scaled to income levels because the primary method to raise revenue at the sub-state level is property tax.

Of course, after many have retired their incomes will diminish, and there is no possible way that households could sustain such a tax bill.

But your point is valid - wealthier households would pay double or triple.

Of course, after many have retired their incomes will diminish, and there is no possible way that households could sustain such a tax bill.

But your point is valid - wealthier households would pay double or triple.

"U.S. state and local governments will need to raise taxes by $1,398 per household every year for the next 30 years"

That appears to be some very sloppy writing. (At least, I hope it is.) What it technically says is that if average taxes are $N per household per year now, then they will be $N+1398 the first year, $N+2*1398 the 2nd year, ... and $N+30*1398 the 30th year. That's very different from a one time increase of $1,398/household/year that will apply to each of the next 30 years (which is what I am guessing they meant).

That appears to be some very sloppy writing. (At least, I hope it is.) What it technically says is that if average taxes are $N per household per year now, then they will be $N+1398 the first year, $N+2*1398 the 2nd year, ... and $N+30*1398 the 30th year. That's very different from a one time increase of $1,398/household/year that will apply to each of the next 30 years (which is what I am guessing they meant).

# posted by : 2:30 PM

: 2:30 PM

Foo - I found the paper.

We calculate the increases in state and local revenues required to achieve full funding of state

and local pension systems in the U.S. over the next 30 years. Without policy changes, contributions to these systems would have to immediately increase by a factor of 2.5, reaching 14.2% of the total own-revenue generated by state and local governments (taxes, fees and charges). This represents a tax increase of $1,398 per U.S. household per year, above and beyond revenue generated by expected economic growth. In thirteen states the necessary increases are more than $1,500 per household per year, and in five states they are more than $2,000 per household per year. Shifting all new employees onto defined contribution plans and Social Security still leaves required increases at an average of $1,223 per household. Even with a hard freeze of all benefits at today’s levels, contributions still have to rise by more than $800 per U.S. household to achieve full funding in 30 years.

Accounting for endogenous shifts in the tax base in response to tax increases or spending cuts increases the dispersion in required incremental contributions among states.

*

Post a Comment

We calculate the increases in state and local revenues required to achieve full funding of state

and local pension systems in the U.S. over the next 30 years. Without policy changes, contributions to these systems would have to immediately increase by a factor of 2.5, reaching 14.2% of the total own-revenue generated by state and local governments (taxes, fees and charges). This represents a tax increase of $1,398 per U.S. household per year, above and beyond revenue generated by expected economic growth. In thirteen states the necessary increases are more than $1,500 per household per year, and in five states they are more than $2,000 per household per year. Shifting all new employees onto defined contribution plans and Social Security still leaves required increases at an average of $1,223 per household. Even with a hard freeze of all benefits at today’s levels, contributions still have to rise by more than $800 per U.S. household to achieve full funding in 30 years.

Accounting for endogenous shifts in the tax base in response to tax increases or spending cuts increases the dispersion in required incremental contributions among states.

*

<< Home

![]()