MaxedOutMama

MaxedOutMama

Friday, July 08, 2011

What's Happening In A Nutshell

We all know about the recent high inflation centered in the unavoidable expenditures of life. Maybe the hedonics of the iPad are favorable, but can you afford to drive to work to earn the money to buy the iPad? An increasing number of people who ARE working are finding it hard to cover their basic expenditures.

By May, consumers were so strapped that they had to cut back spending. We saw this in a very poor retail sales report, in which spending at grocery stores actually dropped and spending at pharmacies was almost flat. Today we got May's consumer credit report. The CW on this is that increasing revolving balances are a sign of consumer confidence. Not so. They are a sign of consumers not being able to pay for their monthly basic needs out of their paychecks. This is rather clear when you look at the non-revolving credit and at May retail sales.

Now, put yourself in the position of one of those consumers who finds herself unable to pay the utility bill (May is just about the average yearly low), gas charged on the credit card, and food charged on the credit card. You abruptly cut back on your spending, don't you? Because with half a year gone, you are strapped already, every time you go in the stores the prices are rising, and you are rather worried about covering your bills for the rest of the year, much less paying for Thanksgiving dinner, heating your home, and covering holiday gifts.

So you pull back, and we see that is just what happened when we look at bank deposits:

This graph is of seasonally adjusted Other Deposits from the H.8 release through June 29th.

This graph is predicting very bad summer retail sales, because it shows an abrupt change in the behavior of consumers and businesses.

We also should check consumer revolving credit at banks to see how consumers are doing:

Well, the curve isn't bending back, and this means that our sorrow will continue.

It also means that banks have to escalate their monitoring on CC risk - under these circumstances, if you let borrowers jack up their credit balances too much, you will face increasing defaults down the road.

As I look at this, I see that our situation has not eased and that instead we are just entering into the worst of it. Food prices and prices for everything are going up. Over the year, May CPI-W was up 4.1% and CPI-U was 3.6%. But the traveling pace of inflation over a few months was much higher, with the CPI-U quarterly inflation rate at 4.6% and the six-month inflation rate at 5.1%. For lower income households, those two rates are higher. CPI-U is the overall consumer inflation rate - CPI-W is for lower income workers, and it is running substantially above CPI-U. These households can't afford the hedonics. Also rural inflation is much higher, and rural CPI-W inflation is over 5% in many places. Look at the regional and urban/suburban/non-metro splits here.

So, now we have a situation at which small business revenues are mostly threatened, and large service business revenues are in trouble too, so service businesses have to raise prices to cover the increase in their basic costs, but will inevitably see dropping revenues as a result!

And then we are slowly losing jobs, which will not help real incomes. Oil prices are sharply up, and gas costs will increase again. The transmission of price increases through to the end-user is not nearly complete. We could see inflation over 6% if we get unlucky, because the Fed is cowering in its ivory tower and is too afraid to intervene.

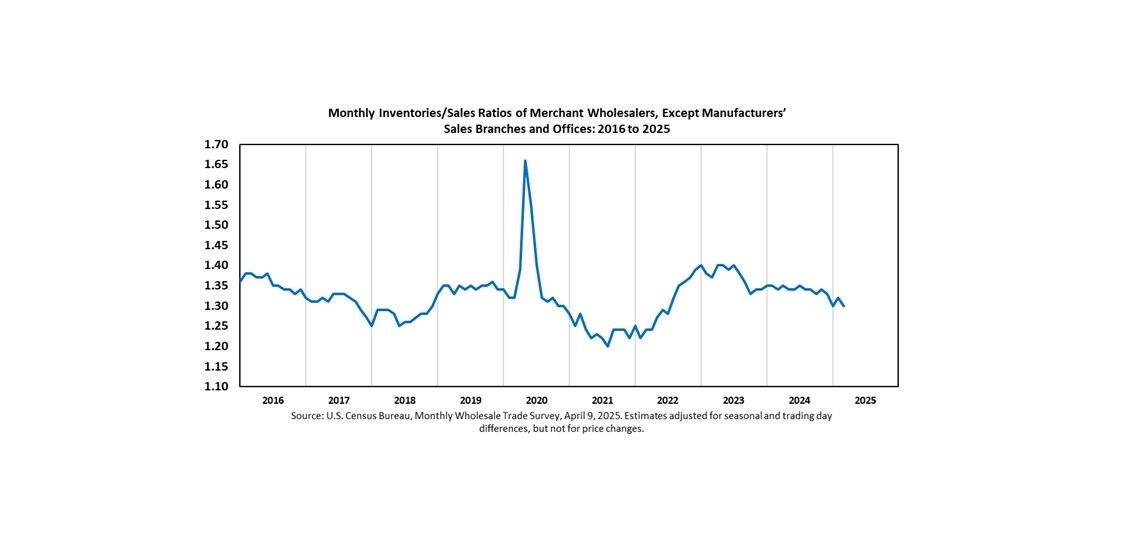

Last, but not least, is that we are going to see the inevitable build of inventories at wholesalers with the inevitable result of declining orders. The first hints of that process are seen in May's report:

This downturn began in April, but will probably be dated by NBER as starting in May or June. It is acute, but it will not be as deep as the previous downturn because less spending from credit is involved.

The only possible fix for this is to knock money out of the system to redress the pricing imbalance, which means the Fed should start raising interest rates. It won't, so don't expect anything to change very quickly.

The shape of this one will look more similar to older recession patterns - there will be a sharp build in inventory, a relatively steep decline in jobs, a bunch of small businesses will just shut down, prices will collapse, and then inventory will clear as production slows deeply and there will be a sharper relative emergence out of it.

But the problem is that this one is coming at a time when all the money has been blown on Keynesian policies already, so the relative contribution from countermeasures will be very minimal.

By May, consumers were so strapped that they had to cut back spending. We saw this in a very poor retail sales report, in which spending at grocery stores actually dropped and spending at pharmacies was almost flat. Today we got May's consumer credit report. The CW on this is that increasing revolving balances are a sign of consumer confidence. Not so. They are a sign of consumers not being able to pay for their monthly basic needs out of their paychecks. This is rather clear when you look at the non-revolving credit and at May retail sales.

Now, put yourself in the position of one of those consumers who finds herself unable to pay the utility bill (May is just about the average yearly low), gas charged on the credit card, and food charged on the credit card. You abruptly cut back on your spending, don't you? Because with half a year gone, you are strapped already, every time you go in the stores the prices are rising, and you are rather worried about covering your bills for the rest of the year, much less paying for Thanksgiving dinner, heating your home, and covering holiday gifts.

So you pull back, and we see that is just what happened when we look at bank deposits:

This graph is of seasonally adjusted Other Deposits from the H.8 release through June 29th.

This graph is predicting very bad summer retail sales, because it shows an abrupt change in the behavior of consumers and businesses.

We also should check consumer revolving credit at banks to see how consumers are doing:

Well, the curve isn't bending back, and this means that our sorrow will continue.

It also means that banks have to escalate their monitoring on CC risk - under these circumstances, if you let borrowers jack up their credit balances too much, you will face increasing defaults down the road.

As I look at this, I see that our situation has not eased and that instead we are just entering into the worst of it. Food prices and prices for everything are going up. Over the year, May CPI-W was up 4.1% and CPI-U was 3.6%. But the traveling pace of inflation over a few months was much higher, with the CPI-U quarterly inflation rate at 4.6% and the six-month inflation rate at 5.1%. For lower income households, those two rates are higher. CPI-U is the overall consumer inflation rate - CPI-W is for lower income workers, and it is running substantially above CPI-U. These households can't afford the hedonics. Also rural inflation is much higher, and rural CPI-W inflation is over 5% in many places. Look at the regional and urban/suburban/non-metro splits here.

So, now we have a situation at which small business revenues are mostly threatened, and large service business revenues are in trouble too, so service businesses have to raise prices to cover the increase in their basic costs, but will inevitably see dropping revenues as a result!

And then we are slowly losing jobs, which will not help real incomes. Oil prices are sharply up, and gas costs will increase again. The transmission of price increases through to the end-user is not nearly complete. We could see inflation over 6% if we get unlucky, because the Fed is cowering in its ivory tower and is too afraid to intervene.

Last, but not least, is that we are going to see the inevitable build of inventories at wholesalers with the inevitable result of declining orders. The first hints of that process are seen in May's report:

This downturn began in April, but will probably be dated by NBER as starting in May or June. It is acute, but it will not be as deep as the previous downturn because less spending from credit is involved.

The only possible fix for this is to knock money out of the system to redress the pricing imbalance, which means the Fed should start raising interest rates. It won't, so don't expect anything to change very quickly.

The shape of this one will look more similar to older recession patterns - there will be a sharp build in inventory, a relatively steep decline in jobs, a bunch of small businesses will just shut down, prices will collapse, and then inventory will clear as production slows deeply and there will be a sharper relative emergence out of it.

But the problem is that this one is coming at a time when all the money has been blown on Keynesian policies already, so the relative contribution from countermeasures will be very minimal.

Comments:

<< Home

Here's what's happening in a nutcase. Sigh.

Wow! My word verification is an actual word this time.

vastly

Something's vastly. No doubt about it.

Wow! My word verification is an actual word this time.

vastly

Something's vastly. No doubt about it.

I just read your comment from the previous thread.

Sorry to hear about the bees. I too have been in a Benadryl state due to pollen being off the charts here.

I feel your pain.

Ouch.

Sorry to hear about the bees. I too have been in a Benadryl state due to pollen being off the charts here.

I feel your pain.

Ouch.

So to sum up our situation: We've got a credit recession, being dragged out into a depression via bad monetary, fiscal and policy decisions, and in the middle of that we're going to have an inventory recession. You might have to start including maps with your posts so we don't get lost.

"It is acute, but it will not be as deep as the previous downturn because less spending from credit is involved."

But the credit recession hasn't been allowed to run its course yet. It's hard to know when that is going to happen, and when it does it will be large. Maybe this inventory recession (combined with our debt problems) will be the trigger. (Though if the debt ceiling gets lifted I'm expecting truly *massive* rates of QE whether they call it that or not as the Treasury issues boat-loads of new debt and the fed feels it has to buy it up to keep rates low.)

"Here's what's happening in a nutcase."

Mark, while I appreciate the play on words, you're only advancing the nutcase's true cause (making money prostituting himself) by giving him more page hits.

"CW" = "Conventional Wisdom" (took me a while to figure that out even with the help of http://www.acronymfinder.com/CW.html)

"It is acute, but it will not be as deep as the previous downturn because less spending from credit is involved."

But the credit recession hasn't been allowed to run its course yet. It's hard to know when that is going to happen, and when it does it will be large. Maybe this inventory recession (combined with our debt problems) will be the trigger. (Though if the debt ceiling gets lifted I'm expecting truly *massive* rates of QE whether they call it that or not as the Treasury issues boat-loads of new debt and the fed feels it has to buy it up to keep rates low.)

"Here's what's happening in a nutcase."

Mark, while I appreciate the play on words, you're only advancing the nutcase's true cause (making money prostituting himself) by giving him more page hits.

"CW" = "Conventional Wisdom" (took me a while to figure that out even with the help of http://www.acronymfinder.com/CW.html)

# posted by  : 8:13 PM

: 8:13 PM

: 8:13 PM

foo,

Mark, while I appreciate the play on words, you're only advancing the nutcase's true cause (making money prostituting himself) by giving him more page hits.

Sigh. Guilty as charged.

Mark, while I appreciate the play on words, you're only advancing the nutcase's true cause (making money prostituting himself) by giving him more page hits.

Sigh. Guilty as charged.

Great blog entry M.O.M. I always look forward to your well constructed economic analysis grounded in fact.

Re: May Consumer Credit Report (section "Federal Government 6":

Whew!

Keep stuffing student loan debt down the throats of the young and there will be no one left to buy a home or a car!

Whew!

Keep stuffing student loan debt down the throats of the young and there will be no one left to buy a home or a car!

# posted by : 12:41 PM

: 12:41 PM

Jill, yup. That is the next bubble to burst, and it will create vast disruption.

We've jerked the next generation around quite enough, thank you.

And if you are worried about asset values, dumping the next generation out there with 40-75K of college loans plus the requirement for a downpayment plus declining real salaries means they won't be able to buy the old fart's houses.

A lot of these loans don't go away in BK. There are people now have student loan repayments deducted from their SS checks.

We've jerked the next generation around quite enough, thank you.

And if you are worried about asset values, dumping the next generation out there with 40-75K of college loans plus the requirement for a downpayment plus declining real salaries means they won't be able to buy the old fart's houses.

A lot of these loans don't go away in BK. There are people now have student loan repayments deducted from their SS checks.

College loans for jobs that are being off shored ?

Sounds like a plan. The young can't afford to buy

Assets of their elders because there are no jobs and

The elders can't retire because the young can't buy their

Assets. I know many here don't want to hear it, but it

is time we put our citizens ahead multinational corporations,

even if it means serious pain in the short run.

Sporkfed

Sounds like a plan. The young can't afford to buy

Assets of their elders because there are no jobs and

The elders can't retire because the young can't buy their

Assets. I know many here don't want to hear it, but it

is time we put our citizens ahead multinational corporations,

even if it means serious pain in the short run.

Sporkfed

# posted by : 1:50 PM

: 1:50 PM

MoM,

There's some funny stuff going on in the H.8 report this year: subs of foreign chartered banks have escalating cash levels, and I wonder if their "Other Deposits" may not be climbing on the liability side. According to the report, the Excess Reserves of the system have shifted to these foreign subs. In effect, they have repatriated loans to foreign affiliates into cash. Not sure it affects your thesis, but maybe its best to just look at the domestically chartered banks.

There's some funny stuff going on in the H.8 report this year: subs of foreign chartered banks have escalating cash levels, and I wonder if their "Other Deposits" may not be climbing on the liability side. According to the report, the Excess Reserves of the system have shifted to these foreign subs. In effect, they have repatriated loans to foreign affiliates into cash. Not sure it affects your thesis, but maybe its best to just look at the domestically chartered banks.

# posted by : 3:59 PM

: 3:59 PM

David - I think we are seeing a range of effects, but when you take the CCs, the deposits and the retail reports, they are showing a remarkably synced effect. In other words, it is real.

My guess is that a lot of service businesses on the small side felt the hit and have curbed their spending, which would account for a lot of this.

My guess is that a lot of service businesses on the small side felt the hit and have curbed their spending, which would account for a lot of this.

Also, David, deposits aren't bank reserves - the Other Deposits figure literally is deposits, and not jumbo deposits either. If you look at page 19 in H.8, you'll see that foreign-related Other Deposits are so small that they cannot possibly account for this effect.

Interestingly, large time deposits at foreign related are dropping so hard that they are more than overcoming the June pop in Other Deposits at foreign-related.

There is nothing to keep a foreign institution from placing its reserves on deposit in a US branch or subdivision, but reserves would generally be in large time deposits, not other deposits.

On page 7 you'll see that domestic charters SA Other Deposits for May was 6,265.7, and June 29th is listed as 6,433.7. This is real.

I usually look at total, Small Domestic Charters, Large Domestic Charters, and then Foreign-related. I don't know why, really, I've always tracked large and small separately.

I went out and did two grocery stores myself today. I would say that the floor is cracking under us right now. The indicators have been getting worse all year, but now things just look squirrelly and haggard.

Interestingly, large time deposits at foreign related are dropping so hard that they are more than overcoming the June pop in Other Deposits at foreign-related.

There is nothing to keep a foreign institution from placing its reserves on deposit in a US branch or subdivision, but reserves would generally be in large time deposits, not other deposits.

On page 7 you'll see that domestic charters SA Other Deposits for May was 6,265.7, and June 29th is listed as 6,433.7. This is real.

I usually look at total, Small Domestic Charters, Large Domestic Charters, and then Foreign-related. I don't know why, really, I've always tracked large and small separately.

I went out and did two grocery stores myself today. I would say that the floor is cracking under us right now. The indicators have been getting worse all year, but now things just look squirrelly and haggard.

David - one last thing about the foreign-related. Do you know why there would be a big drop in large time deposits there?

That was what I noticed this month. Large time deposits at domestic-chartered came down a touch, but at foreign-related they have plummeted:

Domestics, all, SA:

Large time deposits:

May: 728

June 29th: 721.6

Foreign-related, SA:

Large time deposits:

May: 1,075.3

June 29th: 1035.5

We'll see if it holds (there is sampling error in these reports), but it is a big change. Some of these foreign-related aren't really banks - this is what the Fed has to say about it:

"Foreign-related institutions include U.S. branches and agencies of foreign banks as well as Edge Act and agreement corporations. "

Edge Act corporations are chartered by the FRB for international banking, i.e. moving money. Because so much of the commodity prices have seemed to me to be related to currency fluctuations this year, I was wondering if a lot of money isn't being moved around to do this. Edge Act corps do take deposits and they do lend, but they only do so in transactions related to international banking.

I know they hold a lot of deposits for international trade purposes, which is why their large time deposits are so big compared to domestics.

That was what I noticed this month. Large time deposits at domestic-chartered came down a touch, but at foreign-related they have plummeted:

Domestics, all, SA:

Large time deposits:

May: 728

June 29th: 721.6

Foreign-related, SA:

Large time deposits:

May: 1,075.3

June 29th: 1035.5

We'll see if it holds (there is sampling error in these reports), but it is a big change. Some of these foreign-related aren't really banks - this is what the Fed has to say about it:

"Foreign-related institutions include U.S. branches and agencies of foreign banks as well as Edge Act and agreement corporations. "

Edge Act corporations are chartered by the FRB for international banking, i.e. moving money. Because so much of the commodity prices have seemed to me to be related to currency fluctuations this year, I was wondering if a lot of money isn't being moved around to do this. Edge Act corps do take deposits and they do lend, but they only do so in transactions related to international banking.

I know they hold a lot of deposits for international trade purposes, which is why their large time deposits are so big compared to domestics.

David, you are a bad influence on me. Now I'm going to bore everyone with foreign-related and trade.

Stop me before I chase away the last four readers....

Stop me before I chase away the last four readers....

I've read that you can't discharge student loans when permanently disabled. (I know that you can theoretically, but am talking real life here.) Add to that the fact that Sallie Mae really does not want to work with debtors and you have a very ugly situation. It took me a year to have them discharge Jeffrey's part of our student loan after his death.

MoM,

Thanks for the responses. Those foreign subs are a mystery to me. Why should they account for so much of Excess Reserves? Best I can guess is that it has something to do with the problems in the European banking system.

I hear you on your overall view. I think we are seeing the effects of an unabated "strip mall recession". The lower tier of the two-tier economy is rearing its head, bent on revenge. The technocrats would like to respond with yet more stimulus/debt, but their hands are tied by the Tea Party here and previous can-kicking in Europe. Woe are they...

Post a Comment

Thanks for the responses. Those foreign subs are a mystery to me. Why should they account for so much of Excess Reserves? Best I can guess is that it has something to do with the problems in the European banking system.

I hear you on your overall view. I think we are seeing the effects of an unabated "strip mall recession". The lower tier of the two-tier economy is rearing its head, bent on revenge. The technocrats would like to respond with yet more stimulus/debt, but their hands are tied by the Tea Party here and previous can-kicking in Europe. Woe are they...

# posted by : 12:32 PM

: 12:32 PM << Home

![]()