MaxedOutMama

MaxedOutMama

Wednesday, June 26, 2013

Nope, Not Dead

Just sort of feeling like it.

I am, however, laughing my butt off at the bond reversion, the hysterics over the Fed comments, and the pathetic hope that a final 1.8% Q1 annualized GDP created in the hearts of the Fed-dependent investing class, which after so many years now comprises a startlingly high percentage of the younger financial traders. Many of these guys have never seen a normal market without the Fed put.

First quarter GDP is not going to make a lick of difference to the Fed, because the Fed is clearly concentrating on a QE total that they can "afford" rather than on economic numbers, and they are bound to that because of the necessity to reserve firepower for later fiscal consolidation and the next recession.

In February Mishkin et al published a paper on the exit (Crunch Time, Fiscal Crises and the Role of Monetary Policy) and its risks. It lays out in some detail the unhappy position of the Fed:

Oops. The ten-year is now where they projected it to be in 2013. And, as they carefully presented, their loss forecasts are dependent on interest rates - higher changes in rates, higher losses:

Oops. The ten-year is now where they projected it to be in 2013. And, as they carefully presented, their loss forecasts are dependent on interest rates - higher changes in rates, higher losses:

So they can't really sell much of their asset load, which leaves the Fed sitting on a boatload of excess reserves which it must somehow prevent from blasting into monetary circulation.The Fed has created a spring-loaded mechanism which it has only a few methods to control.

So they can't really sell much of their asset load, which leaves the Fed sitting on a boatload of excess reserves which it must somehow prevent from blasting into monetary circulation.The Fed has created a spring-loaded mechanism which it has only a few methods to control.

One of those methods - and the one they will now likely be forced into implementing by 2014, unless we are tipping into outright recession by then - would be to demand higher reserves, thus converting some of the excess reserves into required reserves. This will likely be done under the rubric of financial stability. However when they do this in combination with higher rates, they will have to pay a certain amount still on those reserves (to avoid tipping some of the larger institutions into trouble, which will be politically unpopular and will increase their losses.

The Fed is not going to sell its accumulated QE assets. It will instead let them run off. It must therefore limit current QE, because nobody at the Fed believes we are going to go another five years without a recession! The Fed needs to leave room for further QE to offset future problems and any feeble federal attempts at redressing our fiscal imbalances.

Neil, this is for you: In this paper the authors discuss how the Fed accounting will work in the case of recognized losses. They quietly changed accounting procedures in I think 2011? so that they will stick them in a deferred asset account, which is essentially a claim on future profits. In order to cover operating cash flow, the Fed will create new reserves just as it now does when QEing.

But here's the problem: The theory that the Federal government can just keep borrowing and that the Fed can just keep buying the market excess of Treasuries, thus preventing a fiscal crisis in which US bond yields abruptly spike, is dependent on the idea that the additional Treasures the Fed buys will essentially be null borrowing, because the Fed will return the interest payments to the Treasury. The Fed can only do so if it is making a profit, which it cannot do under current circs. As interest rates rebound even somewhat and the economy stays out of recession, even the Fed's net interest margin begins to get pretty crappy and slim.

The other way in which the debt can be financed is that the Fed keeps buying and creating excess reserves, but the federal government keeps raising taxes so the net borrowing in the economy can't increase much, therefore controlling inflation by essentially depressing the circulation of money. In this scenario, asset prices can stay pretty high for quite a while, but the Main Street economy begins to look more and more Japanese (and not in a good way). Ultimately this probably ends up at the same Argentinian-type endpoint unless entitlement programs are sharply cut (deflationary, Japanese endpoint), because entitlement programs are now so cohesive that there is a growing Fed subsidy of constantly declining real wages for the bottom half of the population (Japanese-ish). Thus in the low-growth labor slack internal devaluation, the Fed has to keep borrowing to subsidize living costs for the great unwashed masses, who have guns (more Argentinian than Japanese).

It's worth noting that this year's tax increase seems to be fueling consumer borrowing to cover living costs (see revolving consumer credit).

Mortgage rates have risen very dramatically in less than two months. At over 4.5%, the FHA cost is nearing 6% when the annual insurance premiums is added. We cannot afford too much more of this without suppressing first time purchasers. There has been a huge jump in mortgage rates since the FOMC meeting and the shock, awe and horror moment. Before the conference they were still hanging in at about 4.1%. As of now, 30 year fixeds have risen about 100 basis points (1 percent) since the end of April. By the end of the summer the effect on home sales should be showing up (existing home sales clock about six or seven weeks after contract.).

The rebound in the housing market is compensating for the flattening out of the auto sales market and keeping us off the economic floor. If you are the Fed, you are not going to like these rates.

But the Fed heads will be contemplating the nasty possibility that if the retract and Uncle Ben promises that the Fed credit card will be paid in full through 2014, the next attempt to exit might create a much worse shock. Nor is it clear that rates will go down that much even if the Fed now publicly repents - the rate shock impends and this week gave all the Mr. Market types a preview of what they might be facing.

I am, however, laughing my butt off at the bond reversion, the hysterics over the Fed comments, and the pathetic hope that a final 1.8% Q1 annualized GDP created in the hearts of the Fed-dependent investing class, which after so many years now comprises a startlingly high percentage of the younger financial traders. Many of these guys have never seen a normal market without the Fed put.

First quarter GDP is not going to make a lick of difference to the Fed, because the Fed is clearly concentrating on a QE total that they can "afford" rather than on economic numbers, and they are bound to that because of the necessity to reserve firepower for later fiscal consolidation and the next recession.

In February Mishkin et al published a paper on the exit (Crunch Time, Fiscal Crises and the Role of Monetary Policy) and its risks. It lays out in some detail the unhappy position of the Fed:

The Fed could cut its effective drain on the Treasury significantly by putting off asset sales and delaying policy rate increases. But such a response would presumably feed rising inflation expectations. In brief, the combination of a massively expanded central bank balance sheet and an unsustainable public debt trajectory is a mix that has the potential to substantially reduce the flexibility of monetary policy. This mix could induce a bias toward slower exit or easier policy, and be seen as the first step toward fiscal dominance. It could thereby be the cause of longer-term inflation expectations and raise the risk of inflation overall.But here's the thing - this paper was way too optimistic. See, for example interest rate projections vs reality:

One of those methods - and the one they will now likely be forced into implementing by 2014, unless we are tipping into outright recession by then - would be to demand higher reserves, thus converting some of the excess reserves into required reserves. This will likely be done under the rubric of financial stability. However when they do this in combination with higher rates, they will have to pay a certain amount still on those reserves (to avoid tipping some of the larger institutions into trouble, which will be politically unpopular and will increase their losses.

The Fed is not going to sell its accumulated QE assets. It will instead let them run off. It must therefore limit current QE, because nobody at the Fed believes we are going to go another five years without a recession! The Fed needs to leave room for further QE to offset future problems and any feeble federal attempts at redressing our fiscal imbalances.

Neil, this is for you: In this paper the authors discuss how the Fed accounting will work in the case of recognized losses. They quietly changed accounting procedures in I think 2011? so that they will stick them in a deferred asset account, which is essentially a claim on future profits. In order to cover operating cash flow, the Fed will create new reserves just as it now does when QEing.

But here's the problem: The theory that the Federal government can just keep borrowing and that the Fed can just keep buying the market excess of Treasuries, thus preventing a fiscal crisis in which US bond yields abruptly spike, is dependent on the idea that the additional Treasures the Fed buys will essentially be null borrowing, because the Fed will return the interest payments to the Treasury. The Fed can only do so if it is making a profit, which it cannot do under current circs. As interest rates rebound even somewhat and the economy stays out of recession, even the Fed's net interest margin begins to get pretty crappy and slim.

The other way in which the debt can be financed is that the Fed keeps buying and creating excess reserves, but the federal government keeps raising taxes so the net borrowing in the economy can't increase much, therefore controlling inflation by essentially depressing the circulation of money. In this scenario, asset prices can stay pretty high for quite a while, but the Main Street economy begins to look more and more Japanese (and not in a good way). Ultimately this probably ends up at the same Argentinian-type endpoint unless entitlement programs are sharply cut (deflationary, Japanese endpoint), because entitlement programs are now so cohesive that there is a growing Fed subsidy of constantly declining real wages for the bottom half of the population (Japanese-ish). Thus in the low-growth labor slack internal devaluation, the Fed has to keep borrowing to subsidize living costs for the great unwashed masses, who have guns (more Argentinian than Japanese).

It's worth noting that this year's tax increase seems to be fueling consumer borrowing to cover living costs (see revolving consumer credit).

Mortgage rates have risen very dramatically in less than two months. At over 4.5%, the FHA cost is nearing 6% when the annual insurance premiums is added. We cannot afford too much more of this without suppressing first time purchasers. There has been a huge jump in mortgage rates since the FOMC meeting and the shock, awe and horror moment. Before the conference they were still hanging in at about 4.1%. As of now, 30 year fixeds have risen about 100 basis points (1 percent) since the end of April. By the end of the summer the effect on home sales should be showing up (existing home sales clock about six or seven weeks after contract.).

The rebound in the housing market is compensating for the flattening out of the auto sales market and keeping us off the economic floor. If you are the Fed, you are not going to like these rates.

But the Fed heads will be contemplating the nasty possibility that if the retract and Uncle Ben promises that the Fed credit card will be paid in full through 2014, the next attempt to exit might create a much worse shock. Nor is it clear that rates will go down that much even if the Fed now publicly repents - the rate shock impends and this week gave all the Mr. Market types a preview of what they might be facing.

Comments:

It seems to me that the intention behind immigration amnesty is to aggregate power to The Party. Per M_O_M's comment, taking these people out of the underground cash economy and bringing them into the legal minimum wage/welfare economy can only worsen the Fed's predicament. Of course, once the gravy train explodes, amnesty won't serve its purpose anymore.

Likewise, if the Fed were really serious about keeping their power as an independent institution, I would think they'd have been more wary of subsidizing the Treasury. At this point, it seems to me they're lashed to the mast of the Treasury market and will have to do whatever is required to keep it afloat.

I'm sure that does make them nervous, but I don't see what they're going to do about it beyond hope that something turns up.

<< Home

Ah, you read my mind. However:

"The Fed can only do so without creating more new reserves if it is making a profit, which it cannot do under current circs."

FIFY.

The Fed has apparently abandoned the old-fashioned concept of money as a store of value. That's the only way they could possibly justify keeping rates so artificially low for so long.

Having abandoned that principle, why not just create money as a convenience, as a way to keep the gravy train running? Money is now simply a tool for aggregating resources to the Party. Party on!

Glad you're still around, M_O_M.

"The Fed can only do so without creating more new reserves if it is making a profit, which it cannot do under current circs."

FIFY.

The Fed has apparently abandoned the old-fashioned concept of money as a store of value. That's the only way they could possibly justify keeping rates so artificially low for so long.

Having abandoned that principle, why not just create money as a convenience, as a way to keep the gravy train running? Money is now simply a tool for aggregating resources to the Party. Party on!

Glad you're still around, M_O_M.

MoM, Is there a link (url) missing after "Neil, this is for you: In this paper..." ? What paper ??

p.s. welcome back to posting, and thank you for your good work.

p.s. welcome back to posting, and thank you for your good work.

Missed you...your Blog is one of the best on real world economics...Thank You for posting!

# posted by  : 5:16 AM

: 5:16 AM

: 5:16 AM

Joseph, it's the Miskin et al paper. Mishkin was a member of the Board of Governors of the Fed in the run up to the late great recession. Most famously, he predicted a recovery in the housing market before it had collapsed.

The paper is worth a read (you can skip all the math in the first part if it is repulsive) because it is a genuine look at the Fed's predicament.

The paper is worth a read (you can skip all the math in the first part if it is repulsive) because it is a genuine look at the Fed's predicament.

Neil, LOL. When they say "fiat" currency they really DO MEAN IT.

The impediment to further Fed actions is not to preserve the value of money, or even their own profitability. They will only be stopped when they perceive a significant risk that they are achieving small current leverage at the cost of losing large future leverage.

In short, the Fed is, like all institutions, self-preserving. It will attempt to act to preserve its own power.

Yes, they can create infinite reserves, but they cannot do so without losing some degree of future control over monetary policy. The path they have been following does have consequences, and they are somewhat nervous about them.

The impediment to further Fed actions is not to preserve the value of money, or even their own profitability. They will only be stopped when they perceive a significant risk that they are achieving small current leverage at the cost of losing large future leverage.

In short, the Fed is, like all institutions, self-preserving. It will attempt to act to preserve its own power.

Yes, they can create infinite reserves, but they cannot do so without losing some degree of future control over monetary policy. The path they have been following does have consequences, and they are somewhat nervous about them.

"Ultimately this probably ends up at the same Argentinian-type endpoint unless entitlement programs are sharply cut (deflationary, Japanese endpoint), because entitlement programs are now so cohesive that there is a growing Fed subsidy of constantly declining real wages for the bottom half of the population (Japanese-ish). Thus in the low-growth labor slack internal devaluation, the Fed has to keep borrowing to subsidize living costs for the great unwashed masses"

Well then, that explains the rush to hurry through another 11 million new citizens and a guest-worker program for the next 11 million. No?

Well then, that explains the rush to hurry through another 11 million new citizens and a guest-worker program for the next 11 million. No?

# posted by : 9:18 AM

: 9:18 AM It seems to me that the intention behind immigration amnesty is to aggregate power to The Party. Per M_O_M's comment, taking these people out of the underground cash economy and bringing them into the legal minimum wage/welfare economy can only worsen the Fed's predicament. Of course, once the gravy train explodes, amnesty won't serve its purpose anymore.

Likewise, if the Fed were really serious about keeping their power as an independent institution, I would think they'd have been more wary of subsidizing the Treasury. At this point, it seems to me they're lashed to the mast of the Treasury market and will have to do whatever is required to keep it afloat.

I'm sure that does make them nervous, but I don't see what they're going to do about it beyond hope that something turns up.

Neil and Allan - Wouldn't it be the only possible strategy to retain a coalition?

The other side of the Fed predicament is the federal budgetary predicament, and there the federal government is going to have to be cutting benefits to the average person instead of promising new ones. To bring in a new class of people who can be granted new benefits is one way of making the electoral math work.

The other side of the Fed predicament is the federal budgetary predicament, and there the federal government is going to have to be cutting benefits to the average person instead of promising new ones. To bring in a new class of people who can be granted new benefits is one way of making the electoral math work.

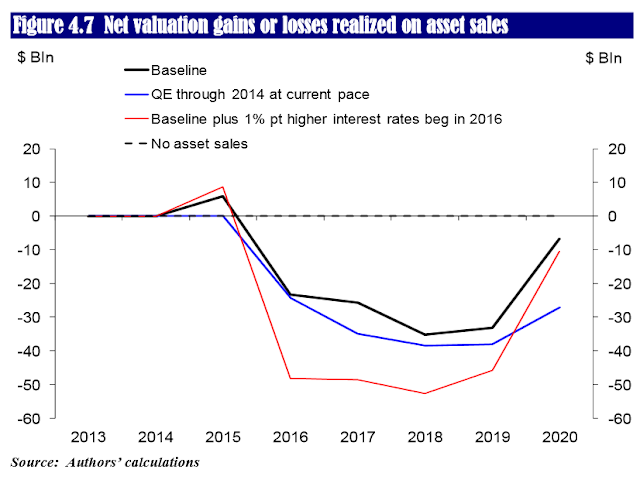

I wonder how Figure 4.7 is arrived at. Since the case with no asset sales is 0 the whole way, it seems to me they're not including the positive carry on the position which is substantial. If that's the case the numbers would look a whole lot better if you included that.

# posted by : 3:14 PM

: 3:14 PM

CF - I THINK they are just trying to figure what would go into the deferred assets account under various scenarios.

On page 71 you'll see a very different graph, which projects expenses and income. Of course the accumulated assets all carry interest, and the net if they don't sell is just fine.

Which is why I don't believe they will sell assets. The paper assumes they do.

If they don't sell assets, they either have to wait for the federal government to tighten via taxation or they have to hike interest rates on those reserves.

The baseline assumption in this paper is that asset purchases at the current level continue until the end of 2013, and are stopped after that, that principal reinvestment continues through all of 2014, and that the Fed gradually sells off the MBS mostly from 2016 to 2019, while holding on to the Treasuries.

Because the Fed is going to continue buying at least something into 2014 and because rate assumptions were too low, the Fed is going to end up with assets above the 3.6T level, which implies excess reserves at around 2.5T. See figure 4.3 on external page 69.

On page 71 you'll see a very different graph, which projects expenses and income. Of course the accumulated assets all carry interest, and the net if they don't sell is just fine.

Which is why I don't believe they will sell assets. The paper assumes they do.

If they don't sell assets, they either have to wait for the federal government to tighten via taxation or they have to hike interest rates on those reserves.

The baseline assumption in this paper is that asset purchases at the current level continue until the end of 2013, and are stopped after that, that principal reinvestment continues through all of 2014, and that the Fed gradually sells off the MBS mostly from 2016 to 2019, while holding on to the Treasuries.

Because the Fed is going to continue buying at least something into 2014 and because rate assumptions were too low, the Fed is going to end up with assets above the 3.6T level, which implies excess reserves at around 2.5T. See figure 4.3 on external page 69.

CF - one thing I don't understand about the Fed speak is the seeming belief that raising interest rates can safely be divorced from the end of QE.

Certainly paying interest on excess reserves is going to have to be tightly calibrated.

The property loans being made alone strongly suggest that those excess reserves are more mobile than the Fed now believes. If investors believe they can buy, hold for a few years, and sell for a net of 10-15%, the recent rates cited at 5% or thereabouts make total sense. What's to prevent this money from bursting out into play?

Certainly paying interest on excess reserves is going to have to be tightly calibrated.

The property loans being made alone strongly suggest that those excess reserves are more mobile than the Fed now believes. If investors believe they can buy, hold for a few years, and sell for a net of 10-15%, the recent rates cited at 5% or thereabouts make total sense. What's to prevent this money from bursting out into play?

Glad to see you're still among the living, MOM.

The touchstone I've learned from the past six years is that things can go on for far longer than I expected. Still, with every episode of "kick the can down the road" we see, the global system gets weaker and weaker. One of these times, something big enough (Japan?) is going to break and everything will tear loose at once.

The touchstone I've learned from the past six years is that things can go on for far longer than I expected. Still, with every episode of "kick the can down the road" we see, the global system gets weaker and weaker. One of these times, something big enough (Japan?) is going to break and everything will tear loose at once.

M_O_M: Does the Mike Tyson quote "Everyone's got a plan till they get hit" seem appropriate here?

This is all very complicated and obviously path dependent. Nice to see the Hubris of Academia coming thru here. The (Ben and Co) Fed have no fcking clue how they're going to behave in 12 months time. I agree most likely outcome is not selling securities and paying interest on reserves. The money markets are not big enough to handle the Reverse Repos necessary to get the rate to go up otherwise.

This is all very complicated and obviously path dependent. Nice to see the Hubris of Academia coming thru here. The (Ben and Co) Fed have no fcking clue how they're going to behave in 12 months time. I agree most likely outcome is not selling securities and paying interest on reserves. The money markets are not big enough to handle the Reverse Repos necessary to get the rate to go up otherwise.

# posted by : 6:02 PM

: 6:02 PM

As to your point about raising rates/end of QE- total Ivory Tower stuff. The is no possible way to manage a smooth transition into a normal rate environment from where we're at. Every bit as ignorant as the thinking that adding 10% to the demand of health care and keeping the supply the same would lower costs.

# posted by : 6:08 PM

: 6:08 PM

CF - that's my conclusion. There can be no smooth exit. It's a spring-loaded Rube Goldberg machine.

Under the theory that FRBNY is really going to be setting Fed policy, regardless of who gets the official nod, I suspect the real outcome will be a series of notches as the Fed is forced to reinstitute MBS buying several times, at least.

Under the theory that FRBNY is really going to be setting Fed policy, regardless of who gets the official nod, I suspect the real outcome will be a series of notches as the Fed is forced to reinstitute MBS buying several times, at least.

Just say "there is no exit". What little GDP we have is contingent upon continued QE. They must continue until it stops working altogether.

It's morphine for the cancer patient; you keep upping the dose until either the patient dies from the disease or an overdose.

It's morphine for the cancer patient; you keep upping the dose until either the patient dies from the disease or an overdose.

Cancer patients never die of an overdose. That would be unethical. They die from predictable side effects of treatment. No difference in outcome to the patient, but avoids lawsuits if you chart it right.

Post a Comment

# posted by : 4:27 AM

: 4:27 AM << Home

![]()