MaxedOutMama

MaxedOutMama

Friday, November 13, 2015

The Fed WANTS Us To Think It Will Raise in December

Which is interesting. I think the Fed was refusing to raise rates until some sort of budget deal was struck, not that they want to come out and say that. Instead they are talking about how nice and strong the economy is.

Industrial Production YoY:

That's, um, really encouraging.

Rail (from AAR.org)

We have gone through a seesaw this year, with about the first 18 weeks being decent, then a soft path until week 33, after which things hung in just a bit below last year, and then around week 39 things started falling out and they aren't quitting.

Carloads haven't really worsened from the soft patch earlier in the year, though they had rebounded and then sank again.

It's intermodal that followed carloads. You can see how it has slowly been weakening YoY in the second half.

It's intermodal that followed carloads. You can see how it has slowly been weakening YoY in the second half.

Some individuals might think that this suggests that the economy is NOT weathering the manufacturing slowdown.

Trucking peaked in January, a few months after IP peaked last fall. From Truckinginfo.com:

It doesn't look like trucking will pull out a YoY even or better in January. Because, what, precisely, would trucking be shipping?

Inventories are pretty high and sales have been low. We're not set up for a strong rebound. Business inventory/sales ratios through September explain why rail is so slow:

Inventories are pretty high and sales have been low. We're not set up for a strong rebound. Business inventory/sales ratios through September explain why rail is so slow:

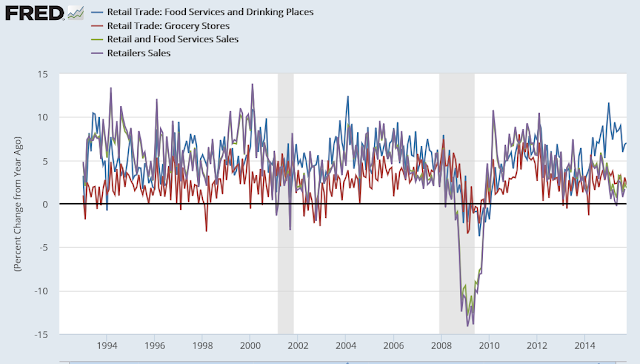

But I gather that retail is supposed to save us because goods are going to be shooting out of the stores so fast!

But retail, except for restaurants and bars, is distinctly so-so right now.

The first thing I thought when I did the first retail graph above was "food costs". Restaurants generally have contracts, and if you have food inflation it delays, and you can get that shift.

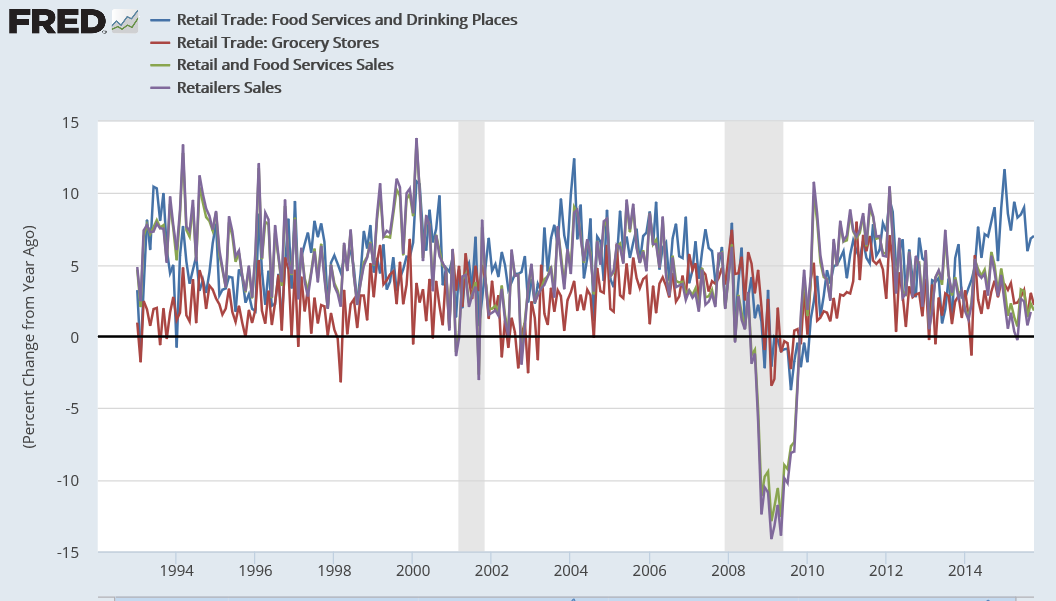

But in this second graph below, we see combining retail and food services doesn't look too hot. And so when I saw that, I thought, "Oh, the cross!" Grocery stores are the standout.

And we do see the cross - grocery store sales exceed retail sales in growth patterns YoY. Common at the beginning or just before recessions. Otherwise, not. It's the Death Cross for economic expansions.

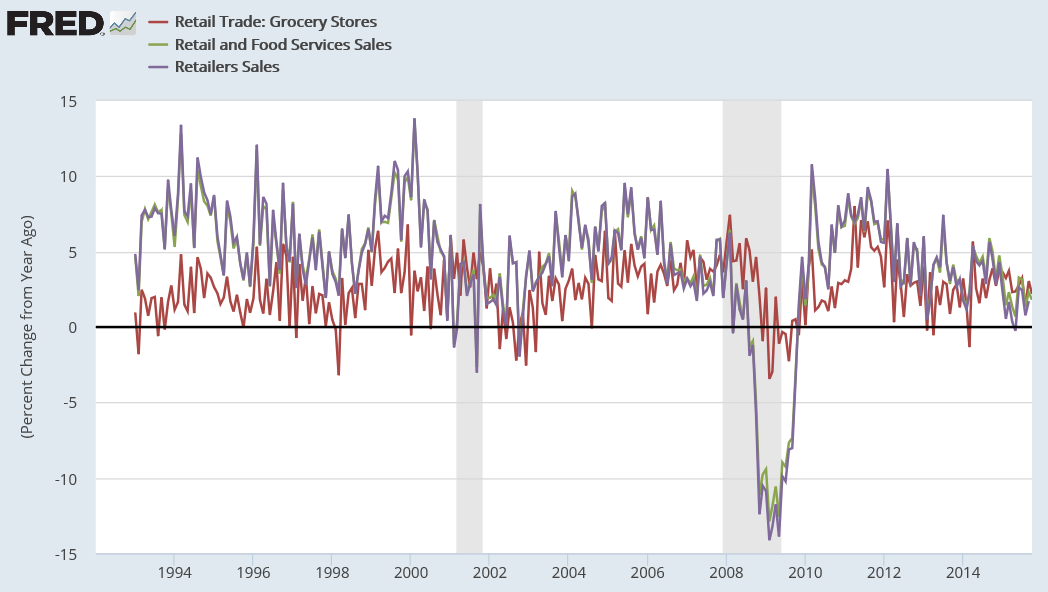

Death Cross up close and personal:

Cool that I did that in Christmas colors, right??? I'm sure the retailers are planning major discounts. MAJOR discounts.

So far, I would say that the only reason we are not already in an obvious recession is strikingly easy credit. So now the Fed says it is going to tighten.

Now, I believed that the Fed should have made this first tiny baby step toward normalization in the spring, because at that time I knew we would carry through on credit-fuelled housing and auto sales (esp. light trucks, which go strong and steady in expanding construction).

Now we are in a weaker position, facing winter. Consumer credit usage is up, manufacturing is in a very weak trend, and I suspect housing is a bit long in the tooth. By next spring I am not sure that it won't be stalled.

Housing prices are just too high for first-time purchasers, and some of the structural steps that were taken this year to help them on no/low downpayment purchase mortgages will have mostly worked their way through the system by next June. Multi-unit (apartments) have been good and usually are durable in the pipeline, but some of the underlying data there has been looking like it's getting a bit aged, and will be vulnerable to protracted weakness. Rents have risen a lot, and it will be hard to cut them because of funding, but rents are rising far too steeply for incomes.

I have always believed that recessions only occur when there is no possible path out, and I would have preferred that the Fed kicked the can a bit earlier this year to give us a little bit less impetus so that we'd buy some time this next year. We're getting close to the "no possible path" zone.

According to most the weather people, this winter could be easier. That would help.

There is no raise for SS in 2016. That's going to hurt us. Health insurance is not going to be an asset, and that's a big understatement.

I am not totally certain that we are going into a recession, but now I am convinced that if we do fall in, we are are going to have a very long European-style recession. It's not a very comforting outlook.

Industrial Production YoY:

That's, um, really encouraging.

Rail (from AAR.org)

We have gone through a seesaw this year, with about the first 18 weeks being decent, then a soft path until week 33, after which things hung in just a bit below last year, and then around week 39 things started falling out and they aren't quitting.

Carloads haven't really worsened from the soft patch earlier in the year, though they had rebounded and then sank again.

Some individuals might think that this suggests that the economy is NOT weathering the manufacturing slowdown.

Trucking peaked in January, a few months after IP peaked last fall. From Truckinginfo.com:

It doesn't look like trucking will pull out a YoY even or better in January. Because, what, precisely, would trucking be shipping?

But I gather that retail is supposed to save us because goods are going to be shooting out of the stores so fast!

But retail, except for restaurants and bars, is distinctly so-so right now.

The first thing I thought when I did the first retail graph above was "food costs". Restaurants generally have contracts, and if you have food inflation it delays, and you can get that shift.

But in this second graph below, we see combining retail and food services doesn't look too hot. And so when I saw that, I thought, "Oh, the cross!" Grocery stores are the standout.

And we do see the cross - grocery store sales exceed retail sales in growth patterns YoY. Common at the beginning or just before recessions. Otherwise, not. It's the Death Cross for economic expansions.

Death Cross up close and personal:

Cool that I did that in Christmas colors, right??? I'm sure the retailers are planning major discounts. MAJOR discounts.

So far, I would say that the only reason we are not already in an obvious recession is strikingly easy credit. So now the Fed says it is going to tighten.

Now, I believed that the Fed should have made this first tiny baby step toward normalization in the spring, because at that time I knew we would carry through on credit-fuelled housing and auto sales (esp. light trucks, which go strong and steady in expanding construction).

Now we are in a weaker position, facing winter. Consumer credit usage is up, manufacturing is in a very weak trend, and I suspect housing is a bit long in the tooth. By next spring I am not sure that it won't be stalled.

Housing prices are just too high for first-time purchasers, and some of the structural steps that were taken this year to help them on no/low downpayment purchase mortgages will have mostly worked their way through the system by next June. Multi-unit (apartments) have been good and usually are durable in the pipeline, but some of the underlying data there has been looking like it's getting a bit aged, and will be vulnerable to protracted weakness. Rents have risen a lot, and it will be hard to cut them because of funding, but rents are rising far too steeply for incomes.

I have always believed that recessions only occur when there is no possible path out, and I would have preferred that the Fed kicked the can a bit earlier this year to give us a little bit less impetus so that we'd buy some time this next year. We're getting close to the "no possible path" zone.

According to most the weather people, this winter could be easier. That would help.

There is no raise for SS in 2016. That's going to hurt us. Health insurance is not going to be an asset, and that's a big understatement.

I am not totally certain that we are going into a recession, but now I am convinced that if we do fall in, we are are going to have a very long European-style recession. It's not a very comforting outlook.

Comments:

So food costs are rising quickly enough that chain restaurants with long-term food contracts right now are relatively a better deal for the consumer? Did I understand that correctly?

Interestingly, meat does not seem to be getting more expensive anymore. I'm wondering if price inflation has moved more to the prepared-foods segment.

<< Home

So food costs are rising quickly enough that chain restaurants with long-term food contracts right now are relatively a better deal for the consumer? Did I understand that correctly?

Interestingly, meat does not seem to be getting more expensive anymore. I'm wondering if price inflation has moved more to the prepared-foods segment.

Mama you don't stop by nearly often enough.

I think the Fed might raise in December because even a 1/2 basis point would be negligible in all reality. If the economy can't take that its doomed anyway. It could go either way but this is their last chance before a recession takes hold and I am guessing their banking cartel is not being helped by this ZIRP state of affairs.

I think the Fed might raise in December because even a 1/2 basis point would be negligible in all reality. If the economy can't take that its doomed anyway. It could go either way but this is their last chance before a recession takes hold and I am guessing their banking cartel is not being helped by this ZIRP state of affairs.

At this point, i wouldn't put it past the Fed to raise rates AND do QE at the same time. Essentially running in place, but even the exercise will shake out some weak hands. As it is now, the only price discovery going on is in commodities and, well with the Fed propping up every sector it could, the only price discovery to be had is downward anyway. From where I sit, outside of perishables there is over-supply in nearly everything except possibly multi-family housing.

By the way, I find it interesting that I have never seen a 3- or 6-flat built in my adult lifetime. One would think with rents rising the small investor would consider such projects. But housing laws, zoning laws, and finance have all seemed to converge to prevent such projects.

By the way, I find it interesting that I have never seen a 3- or 6-flat built in my adult lifetime. One would think with rents rising the small investor would consider such projects. But housing laws, zoning laws, and finance have all seemed to converge to prevent such projects.

# posted by  : 7:52 AM

: 7:52 AM

: 7:52 AM

And urban planners want high density housing. Doesn't matter if anyone else wants to live like that.

What we get instead are folks renting out rooms in houses, sometimes for $5-600 a month.

What we get instead are folks renting out rooms in houses, sometimes for $5-600 a month.

It's fitting that your expectation is that if we fall into recession, it will be a long European recession. After all, we've had a long European recovery.

We have already been tightening relative to most of the world. QE3 ended in October 2014. Check out what the shadow rate has done since then:

https://www.frbatlanta.org/cqer/research/shadow_rate.aspx?panel=1

Oct 2014: -2.8%

Oct 2015: -0.53%

Diff: 227bp over 12 months

Note: lowest shadow rate was May 2014 at -2.99%

Diff from bottom (May 2014) to Oct 2015: 246bp over 18 months

Since 1983, the average fed rate hike cycle lasts 414 days or almost 14 months. The Fed increases interest rates by an average of 281bp over the rate hike cycle. Since 1983, the minimum duration of the rate hike cycle has been 262 days and maximum 729 days. The minimum interest rate increase has been 1.375% and the maximum 4.25%.

WSJ Dollar Index:

May 2014: 72

Oct 2014: 78

Now: 90

There is a strong case to be made that the rate hike cycle (or really monetary tightening cycle) has already begun and interest rates do not have a high probability of exceeding 1-2% FFR during this rate hike cycle. Looking at the shadow rate bottom of -2.99 to a 1% FFR would mean a 399bp increase, nearing the maximum interest rate increase during any cycle since 1983.

http://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20150917.pdf

Fed dot plot from September 2015 has the Fed projecting the FFR to range from 1-2% in 2016, 2-4% in 2017, and 3-4% in 2018 and beyond. When looking at various shadow rate models, this would blow way past both the maximum duration and maximum rate increase in any interest rate cycle since 1983.

Lower, slower, for a lot longer than many people think. We are further along than most economists and market experts think. The Fed President in Minneapolis, Narayana Kocherlakota, is the sole dissenter in the dot plot projecting the need for negative rates next year and 1% in 2017. I’m not sold on negative rates at this time, but see a much higher probability of continued easing measures before we see 2% FFR.

ECB looking at more easing by Q1 2016. Japan in another recession and likely to ease further. PBOC looking at easing measures. The world is tightening for the U.S. Why exacerbate the issue by raising the FFR in a low and stable inflationary environment?

Post a Comment

https://www.frbatlanta.org/cqer/research/shadow_rate.aspx?panel=1

Oct 2014: -2.8%

Oct 2015: -0.53%

Diff: 227bp over 12 months

Note: lowest shadow rate was May 2014 at -2.99%

Diff from bottom (May 2014) to Oct 2015: 246bp over 18 months

Since 1983, the average fed rate hike cycle lasts 414 days or almost 14 months. The Fed increases interest rates by an average of 281bp over the rate hike cycle. Since 1983, the minimum duration of the rate hike cycle has been 262 days and maximum 729 days. The minimum interest rate increase has been 1.375% and the maximum 4.25%.

WSJ Dollar Index:

May 2014: 72

Oct 2014: 78

Now: 90

There is a strong case to be made that the rate hike cycle (or really monetary tightening cycle) has already begun and interest rates do not have a high probability of exceeding 1-2% FFR during this rate hike cycle. Looking at the shadow rate bottom of -2.99 to a 1% FFR would mean a 399bp increase, nearing the maximum interest rate increase during any cycle since 1983.

http://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20150917.pdf

Fed dot plot from September 2015 has the Fed projecting the FFR to range from 1-2% in 2016, 2-4% in 2017, and 3-4% in 2018 and beyond. When looking at various shadow rate models, this would blow way past both the maximum duration and maximum rate increase in any interest rate cycle since 1983.

Lower, slower, for a lot longer than many people think. We are further along than most economists and market experts think. The Fed President in Minneapolis, Narayana Kocherlakota, is the sole dissenter in the dot plot projecting the need for negative rates next year and 1% in 2017. I’m not sold on negative rates at this time, but see a much higher probability of continued easing measures before we see 2% FFR.

ECB looking at more easing by Q1 2016. Japan in another recession and likely to ease further. PBOC looking at easing measures. The world is tightening for the U.S. Why exacerbate the issue by raising the FFR in a low and stable inflationary environment?

# posted by : 8:58 AM

: 8:58 AM << Home

![]()