MaxedOutMama

MaxedOutMama

Friday, February 29, 2008

Oh, Things Could Certainly Be Better

Maybe the reason that the three top presidential candidates seem to be economic illiterates is that only economic illiterates would run at a time like this. It's hard to figure that we won't be electing a one-term president in November with numbers like these.

Chicago PMI came in at 44.5, well into recessionary territory. Not the beginning of a recession, but part way in. Employment is at 33.5, which also is a reading that should be associated with a later stage of recession.

From the commentary on the release:

Please note the florid language in the commentary to the release. We are all stretched to describe the economic situation. Words like "ghastly" and "collapsing" are the new in thing in economics.

Real PCE for the last three months came in at 0.2, 0.0 and 0.0 (November, December, January). Personal Income and Outlays. Real personal income for the same months clocked in at -0.4, 0.1, 0.1. That's kind of the death knell. Consumers have already dropped to recessionary levels of real spending, and the business indices are falling fast.

It seems that gross private domestic investment will continue to contract in 2008. Overall, the severity of this recession is matching up a lot better with the early 90's than with 2001. My guess is that we will make it to the 80's ultimately.

Japanese production fell 2.0% in January:

Chicago PMI came in at 44.5, well into recessionary territory. Not the beginning of a recession, but part way in. Employment is at 33.5, which also is a reading that should be associated with a later stage of recession.

From the commentary on the release:

Like a siren warning of the approach of a tornado, the 7 point drop in the February Business Barometer sent a warning of the destructive winds of a shrinking US Economy. As the Barometer dove into retreat, the Prices Paid index continued to roar its warning of destructive inflation. The specter of recflation, recession and inflation, provides consumers, business professionals, policymakers, and politicians with a host of challenges and no simple answers.Yep. We now get to pay for all the playing with debt.

Please note the florid language in the commentary to the release. We are all stretched to describe the economic situation. Words like "ghastly" and "collapsing" are the new in thing in economics.

Real PCE for the last three months came in at 0.2, 0.0 and 0.0 (November, December, January). Personal Income and Outlays. Real personal income for the same months clocked in at -0.4, 0.1, 0.1. That's kind of the death knell. Consumers have already dropped to recessionary levels of real spending, and the business indices are falling fast.

It seems that gross private domestic investment will continue to contract in 2008. Overall, the severity of this recession is matching up a lot better with the early 90's than with 2001. My guess is that we will make it to the 80's ultimately.

Japanese production fell 2.0% in January:

Companies plan to cut production in February as well, the report showed. Manufacturers see output sliding 2.9 percent from January, worse than the 2.2 percent drop they earlier anticipated. Output will rebound 2.8 percent next month, the companies said.Consumer spending is very soft in Europe, which does not help matters. If the predictions hold, Japanese manufacturing output will contract in the first quarter. Consumer spending in Japan is impacted by inflation and tight wages.

Wednesday, February 27, 2008

MoM Theory

A bad January durables report. The worst was nondefense capital goods:

If you look at the full advance report (pdf), while shipments are rising inventories are generally high. Fabricated metals orders were down 4.1% after December's 1.2% increase. Shipments of fabricated metals rose 1.0% after two months of declines. Machinery shipments and new orders were down 1.7% and 1.5% respectively, but that came after strong increases in December. Overall, durable shipments are up sharply YoY. It does seem as if there is some life in manufacturing somewhere. Last year YoY shipments mostly declined and that made me very nervous. It could also be that price increases account for the rise, and that volume is largely down.

On a YoY basis, motor vehicles and parts shipments declined 5.7%, and orders declined 7.6%. However unfilled orders are down 13.2% and inventories are down 6.2%, so we are getting closer to increased volume.

The manufacturing issue is becoming increasingly urgent, because mortgage rates are zooming up on risk and (I believe) increased competition from ARS munis trying to roll into longer durations.

MBA:

At 10:00 AM the new home sales report is due to be released, but at this point it hardly matters. At these rates, sales and/or prices of new and existing homes are due to drop significantly. The question is whether this will be a temporary phenomenon or not, and my guess is that it will not be truly temporary, although I expect some fluctuation as each segment unwinds and then gets absorbed.

Greenspan's famous conundrum about the oddity of low long rates combined with high short rates, was, I believe, largely an artifact of long-short financial gearing carried out on a nearly global scale. So much long paper was shifted to finance short-term money that the supply of long paper was constrained and caused it to be sold for a relatively high price (high price = low rate). And now I believe that this trend is due to reduce on a global scale and produce an era in which the effect diminishes broadly.

The ARS muni market is over 300 billion. If 30 percent of it goes longer, that's a lot of increased demand on longer money. The effect will continue, because newer muni issues are less likely to go auction rate. And many other short-term bundling vehicles are breaking down at the same time.

I want to stress that my assertion about the basic mechanism underlying Greenspan's conundrum is not widely shared AFAIK. You are reading my opinion here. I do feel relatively certain that I am correct. I never bought the idea that a "glut of worldwide savings" was at one and the same time producing a nearly global bubble in building and real property (financed by debt) and low long rates financed by savings. The shift in production from high to low-cost areas did cause something of a worldwide drop in inflationary pressures, which clearly was a factor in the beginning of Greenspan's "virtuous" cycle.

Again, this is my theory:

I believe long paper being sold as short allowed investors to pretend that long risk did not exist. But that is a farce, and it was always destined to break down at some point.

Long risks are compounded from several elements. The first is unknowability and change. No matter how carefully you grant credit, as time wears on the condition of your borrowers will change. The financial situation of some will improve, and the financial situation of some will decline. Borrowers whose financial situation has improved are always more likely to refinance out of your credit and into cheaper credit, and therefore the trend for all long credit portfolios over time is worsening credit quality. For that, you charge extra.

The second risk, of course, is that overall rates will rise and you will be stuck with below-market rates, which will reduce the value of your portfolio. However there is some compensating effect, because your credit quality will not diminish nearly as fast in this situation. Your good borrowers are more likely to remain with you, and your intermediate borrowers may be able to refi out and will in order to take on more debt even if they have to pay higher rates to do so.

Auction rate munis, SIVs, and the like were all used to shift rates from long to short. However the end consumers of this credit weren't paying for the risk, and as liquidity on the underlying long instruments drops out, abruptly the risk starts getting priced back in. This causes overall rates to rise, which causes debt servicing costs to rise, which worsens the underlying credit condition of the borrowers who have variable rate long debt. Which causes rates to rise again.... So as far as Mom theory is concerned, the "worldwide glut in savings" was really a worldwide glut of ignoring and underpricing risk.

Nondefense new orders for capital goods in January decreased $6.6 billion or 8.1 percent to $74.6 billion.Ouch! Overall new orders decreased 5.3%.

If you look at the full advance report (pdf), while shipments are rising inventories are generally high. Fabricated metals orders were down 4.1% after December's 1.2% increase. Shipments of fabricated metals rose 1.0% after two months of declines. Machinery shipments and new orders were down 1.7% and 1.5% respectively, but that came after strong increases in December. Overall, durable shipments are up sharply YoY. It does seem as if there is some life in manufacturing somewhere. Last year YoY shipments mostly declined and that made me very nervous. It could also be that price increases account for the rise, and that volume is largely down.

On a YoY basis, motor vehicles and parts shipments declined 5.7%, and orders declined 7.6%. However unfilled orders are down 13.2% and inventories are down 6.2%, so we are getting closer to increased volume.

The manufacturing issue is becoming increasingly urgent, because mortgage rates are zooming up on risk and (I believe) increased competition from ARS munis trying to roll into longer durations.

MBA:

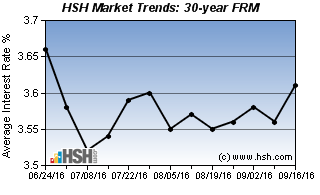

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.27 percent from 6.09 percent, with points increasing to 1.15 from 1.10 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.However this understates the real rise, because an awful lot of mortgages are for LTVs over 80%. HSH publishes true average rates in their weekly trends report:

The average contract interest rate for 15-year fixed-rate mortgages increased to 5.77 percent from 5.55 percent, with points decreasing to 1.01 from 1.08 (including the origination fee) for 80 percent LTV loans.

The average contract interest rate for one-year ARMs increased to 5.84 percent from 5.72 percent, with points decreasing to 0.86 from 0.91 (including the origination fee) for 80 percent LTV loans.

At 10:00 AM the new home sales report is due to be released, but at this point it hardly matters. At these rates, sales and/or prices of new and existing homes are due to drop significantly. The question is whether this will be a temporary phenomenon or not, and my guess is that it will not be truly temporary, although I expect some fluctuation as each segment unwinds and then gets absorbed.

Greenspan's famous conundrum about the oddity of low long rates combined with high short rates, was, I believe, largely an artifact of long-short financial gearing carried out on a nearly global scale. So much long paper was shifted to finance short-term money that the supply of long paper was constrained and caused it to be sold for a relatively high price (high price = low rate). And now I believe that this trend is due to reduce on a global scale and produce an era in which the effect diminishes broadly.

The ARS muni market is over 300 billion. If 30 percent of it goes longer, that's a lot of increased demand on longer money. The effect will continue, because newer muni issues are less likely to go auction rate. And many other short-term bundling vehicles are breaking down at the same time.

I want to stress that my assertion about the basic mechanism underlying Greenspan's conundrum is not widely shared AFAIK. You are reading my opinion here. I do feel relatively certain that I am correct. I never bought the idea that a "glut of worldwide savings" was at one and the same time producing a nearly global bubble in building and real property (financed by debt) and low long rates financed by savings. The shift in production from high to low-cost areas did cause something of a worldwide drop in inflationary pressures, which clearly was a factor in the beginning of Greenspan's "virtuous" cycle.

Again, this is my theory:

I believe long paper being sold as short allowed investors to pretend that long risk did not exist. But that is a farce, and it was always destined to break down at some point.

Long risks are compounded from several elements. The first is unknowability and change. No matter how carefully you grant credit, as time wears on the condition of your borrowers will change. The financial situation of some will improve, and the financial situation of some will decline. Borrowers whose financial situation has improved are always more likely to refinance out of your credit and into cheaper credit, and therefore the trend for all long credit portfolios over time is worsening credit quality. For that, you charge extra.

The second risk, of course, is that overall rates will rise and you will be stuck with below-market rates, which will reduce the value of your portfolio. However there is some compensating effect, because your credit quality will not diminish nearly as fast in this situation. Your good borrowers are more likely to remain with you, and your intermediate borrowers may be able to refi out and will in order to take on more debt even if they have to pay higher rates to do so.

Auction rate munis, SIVs, and the like were all used to shift rates from long to short. However the end consumers of this credit weren't paying for the risk, and as liquidity on the underlying long instruments drops out, abruptly the risk starts getting priced back in. This causes overall rates to rise, which causes debt servicing costs to rise, which worsens the underlying credit condition of the borrowers who have variable rate long debt. Which causes rates to rise again.... So as far as Mom theory is concerned, the "worldwide glut in savings" was really a worldwide glut of ignoring and underpricing risk.

Monday, February 25, 2008

The Major Economic Quandary

Looking at federal tax receipts tells me one thing. Everything else tells me another.

What if what I'm seeing on federal tax receipts is actually the replacement of illegal employees with legal employees?

The picture would be more consistent, but a lot worse.

What if what I'm seeing on federal tax receipts is actually the replacement of illegal employees with legal employees?

The picture would be more consistent, but a lot worse.

Sunday, February 24, 2008

More On McCain's FEC Problem

As I wrote below, McCain has probably locked himself into the public financing system for the primaries. His lawyer says he's out regardless of what the FEC says. This seems reckless to me - McCain is flirting with a 5 year prison term, although of course he would never serve it. But the Republicans are now in a huge fix.

Here is the relevant page of the loan agreement. I have manually typed below (there could be minor errors) the relevant paragraph:

If you disagree, please explain why?

Also I would like to cite a portion of a comment at the prior post by Daniel Newby:

I think the only valid argument that McCain's lawyers can make to assert that he did not pledge the matching funds as collateral is that the agreement is not legally enforceable. That would would make this a loan gained under false pretexts and bad faith, which does not seem better to me. I don't like it if Casey Serin does it, and I don't like it if John McCain does it. At least I am consistent.

The FEC has a major problem here, because of course if they pass this, any candidate could do the same, thus effectively nullifying the "no pledge" rule. Usually courts will not construe even regulatory law in a way that would nullify a provision, unless, of course, the provision is unconstitutional.

Just to clarify, if his lawyers were to make this argument he could find himself in a deposition saying that although the agreement was executed, he knew that the bank could not force him to remain in the public funds system so he never intended to keep his promise. And to what, I ask you, would he be confessing if he did so?

Here is my original post regarding my inability to vote for McCain. And Teri, I would say this is a case of McCain not believing that the same rules hold for the officers as the enlisted pukes!

PS: Here is McCain's withdrawal letter, and here is the FEC's response asking him to explain his claim of not having pledged the funds as security. This is a link to the Dec 17th loan modification. See also the paragraph on page 2 that reads:

Here is the relevant page of the loan agreement. I have manually typed below (there could be minor errors) the relevant paragraph:

Additional Requirement: Borrower and Lender agree that if Borrower withdraws from the public matching funds program, but John McCain then does not win the next primary or caucus in which he is active (which can be any primary or caucus won the same day) or does not place at least within 10 percentage points of the winner of that primary or caucus, Borrower will cause John McCain to remain an active political candidate and Borrower will, within thirty (30) days of said primary or caucus, (i) reapply for matching funds, (ii) grant to Lender, as additional collateral for the Loan, a first priority perfected security interest in and to all of Borrower's right, title and interest in and to the public matching funds program, and (iii) execute and deliver to Lender such documents, interests and agreements as Lender may require with respect to the foregoing. Borrower and Lender agree that Borrower will provide oral or written notice to Lender at least 24 hours before notice of withdrawal from the matching funds program is provided by Borrower or John McCain to the Federal Election Commission.Okay, so my claim is that this is a constructive pledging of the funds as collateral for a bank loan, which should disqualify McCain from withdrawing during the primary election. I am basing this on the interpretations of what would be considered a pledging of retirement accounts. The bottom line is that the loan would not have been granted without this provision. If you included a similar clause in a loan agreement to try to get a loan by using your IRA funds as security without actually paying the taxes on the funds, I think you'd lose that battle!

If you disagree, please explain why?

Also I would like to cite a portion of a comment at the prior post by Daniel Newby:

Certainly McCain would make a magnificent Caesar. His willingness to fight for his people is beyond doubt, and he seems to have a real distaste for intrigue. He would likely pick competent proconsuls, unlike the walking disaster Bush sent to Iraq.I thought this was well stated. I also think the apparent arrogance of McCain's saying that he is withdrawing whether the SEC lets him do so or not is highly disturbing. Certainly it should raise doubts in his supporters' minds.

But does that make him loyal? For me, the heart of the American philosophy is that we keep our political interests out in the open. We put our churches and Klansmen and animal rights activists and everybody else in parades so folks will see plainly what they look like and how they act. The McCain-Feingold Act drives that underground. It teaches free men to either act from the shadows or give up, it quenches solidarity and shared interests among people who work together. I believe these predictable results are corrosive to civil society, and therefore profoundly disloyal.

I think the only valid argument that McCain's lawyers can make to assert that he did not pledge the matching funds as collateral is that the agreement is not legally enforceable. That would would make this a loan gained under false pretexts and bad faith, which does not seem better to me. I don't like it if Casey Serin does it, and I don't like it if John McCain does it. At least I am consistent.

The FEC has a major problem here, because of course if they pass this, any candidate could do the same, thus effectively nullifying the "no pledge" rule. Usually courts will not construe even regulatory law in a way that would nullify a provision, unless, of course, the provision is unconstitutional.

Just to clarify, if his lawyers were to make this argument he could find himself in a deposition saying that although the agreement was executed, he knew that the bank could not force him to remain in the public funds system so he never intended to keep his promise. And to what, I ask you, would he be confessing if he did so?

Here is my original post regarding my inability to vote for McCain. And Teri, I would say this is a case of McCain not believing that the same rules hold for the officers as the enlisted pukes!

PS: Here is McCain's withdrawal letter, and here is the FEC's response asking him to explain his claim of not having pledged the funds as security. This is a link to the Dec 17th loan modification. See also the paragraph on page 2 that reads:

COMPLIANCE WITH THE FEDERAL ELECTION COMMISSION'S MATCHING FUNDS PROGRAM. Borrower agrees and covenants with Lender that while this Agreement is in effect, Borrower shall not, without Lender's prior written consent, exceed overall or state spending limits imposed under the Federal Matching Funds Program, irrespective of whether Borrower is subject to such program as of any applicate date of determination.Read the whole thing. It stinks. On the one hand the campaign covenants to pay back from matching funds if necessary, and on the other hand all the collateral descriptions are rewritten to exclude campaign matching funds.

Saturday, February 23, 2008

Ooh, Bankers Lobbying Congress

It turns out that Bank of America has a nice little plan to solve the mortgage mess, which they have been submitting to your Congress Critters while y'all have been out there working to pay your mortgages. BofA, of course, has the little problem of the CW loans it just bought to deal with, and Congress Critters are relatively cheap in comparison to deeply underwater loans. Tanta's got the story.

A brief summary:

If the American public is willing to let Congress do this, the American public deserves what it is going to get. Remember, it is an election year. Congress Critters are cheap for businesses, but only human beings vote.

My alternate proposal is that we let the current creditors and banks write down these mortgages, and that when the banks fail we pay off the depositors, and then inject money into the system as needed by giving reserve and necessary capital to the most viable banks. In exchange, the federal government (that's you) will take a partial ownership position (stock) in the banks. That ownership position should be put into a fund that is assigned to pay all its profits to the SS/Medicare trust funds. Believe me; whatever money we get out of it we will need later to pay these benefits.

My proposal has the following benefits:

A brief summary:

- BofA will buy the Congress Critters. It is an election year and money is tight, so it will get them at a deep discount.

- The Congress Critters will pass a law saying that the Federal Government (that's you) will buy bad mortgage loans at a "deep discount".

- Then the Federal Government will write the loans down to where the people can afford to pay them (you will pay the unaffordable excess of their mortgage balances.) Don't forget to keep paying on your own mortgage while you are paying theirs!

- The borrowers will keep their homes, but now they will owe less because you will have paid it off to where they can afford it.

- The federal government (that's you!) will now guarantee the loans so they can be sold back to the banks at FMV. If the new loans go bad, the federal government (that's you!) will pay the noteholders off. If they perform, the noteholders (not you) will get the profit.

- It seems unlikely that the original deep discount will actually be the appropriate discount. First, there is no government agency that has the staff to determine what the actual secured value of these mortgages now are. Therefore it seems that the entities selling the bad mortgage loans to the federal government (that's you) will determine what the appropriate "deep discount" will be.

- Since the bad loans are concentrated in high LTV, stated/low-doc mortgages, there is no way to know what they can really pay. Thus the government guarantee is the real meat of this proposal. You will guarantee the banks and their shareholders to pay off their bad mortgages.

If the American public is willing to let Congress do this, the American public deserves what it is going to get. Remember, it is an election year. Congress Critters are cheap for businesses, but only human beings vote.

My alternate proposal is that we let the current creditors and banks write down these mortgages, and that when the banks fail we pay off the depositors, and then inject money into the system as needed by giving reserve and necessary capital to the most viable banks. In exchange, the federal government (that's you) will take a partial ownership position (stock) in the banks. That ownership position should be put into a fund that is assigned to pay all its profits to the SS/Medicare trust funds. Believe me; whatever money we get out of it we will need later to pay these benefits.

My proposal has the following benefits:

- It is cheaper. For one thing, we don't have to cover the cost of purchasing the Congress Critters.

- Banks and other creditors will take the first round of losses, so they will have a high incentive to correct bad lending practices and work out loans. They have the expertise to do this. A chunk of the costs will be paid by private interests, which will save you money.

- You are going to be paying for the excess deposit insurance payouts anyway.

- The money you invest to keep the banking system running will eventually come back to you when you most need it.

- We will recognize the losses now, thus correcting the market and destroying debt.

- There is no need to set up another big government agency, which will save you money right off the bat.

- You will get the banking stock cheap and eventually it will be worth more. Remember, buy low, sell high. The bank proposal is for you to buy high and sell low back to them, plus pay any future losses.

- My proposal would be infinitely better for the economy. The debt overhang is what will drag the economy down for years to come. The only way out is to destroy the bad debt ASAP. So under my proposal, you will enjoy years of higher GDP and lower taxes in about a decade. The deflationary impact will be short and relatively painful, but the lower inflation associated with it will be far better for the average American for many years.

Friday, February 22, 2008

The Mark Of McCain-Feingold

I'm shattered, I tell you! It seems McCain is having a little problemo with campaign financing rules. Seems he promised a bank that he would use public election dollars if need be to pay back a campaign loan, which may be a problem now that he wants to opt out of the primary spending limits after having earlier applied for public financing.

Oh, the injustice! O the horror! Somebody, call the Supreme Court! Oh, the tragedy! It would seem that Mr. McCain_Bipartisan_Feingold, who does not want the little pukes to be able to mention a S_n_t_r's name in vain during the campaign season might be gored by an ox of his own feeding called the FEC.

Speechnow.org should be extremely cheerful at the moment. That is a link to the cached version, since it seems their actual website just vanished.

PS: If you were to put in writing to a bank that you would pay back a loan, if necessary, with your 401K funds or IRA funds and the bank granted the loan using that promise as collateral, under federal law you'd have to pay taxes on the amount used as collateral. It would be treated as a withdrawal. The same principle should hold for McCain. He did use his ability to get the money as collateral according to the article. And since the article is in WaPo it may even be accurate. Forget this "technically" clear bit:

This, folks, is hubris. Those whom the gods wish to destroy, they first make mad. If McCain ignores this law he's in deep, deep shit, and the Republican party better be finding themselves another candidate like yesterday. He didn't have to apply in the first place. He didn't have to promise the bank that he would get matching funds if necessary. Once he did, he can't pretend he didn't.

By the way, the NY Sun editorial outlines the SpeechNow case:

Oh, the injustice! O the horror! Somebody, call the Supreme Court! Oh, the tragedy! It would seem that Mr. McCain_Bipartisan_Feingold, who does not want the little pukes to be able to mention a S_n_t_r's name in vain during the campaign season might be gored by an ox of his own feeding called the FEC.

Speechnow.org should be extremely cheerful at the moment. That is a link to the cached version, since it seems their actual website just vanished.

PS: If you were to put in writing to a bank that you would pay back a loan, if necessary, with your 401K funds or IRA funds and the bank granted the loan using that promise as collateral, under federal law you'd have to pay taxes on the amount used as collateral. It would be treated as a withdrawal. The same principle should hold for McCain. He did use his ability to get the money as collateral according to the article. And since the article is in WaPo it may even be accurate. Forget this "technically" clear bit:

It involves a $1 million loan McCain obtained from a Bethesda bank in January. The bank was worried about his ability to repay the loan if he exited the federal financing program and started to lose in the primary race. McCain promised the bank that, if that happened, he would reapply for matching money and offer those as collateral for the loan. While McCain's aides have argued that the campaign was careful to make sure that they technically complied with the rules, Mason indicated that the question needs further FEC review.Uh-uh. He's trying to have this both ways. He used his ability to get the funds as collateral to get a loan so that he didn't have to draw funds, if this is true. Not only that, but according to the article McCain only tried to cancel out his application for federal funds as of February 6th, and the bank loan was in January. Needless to say, McCain's request has not yet been granted by the FEC, which, it now appears, IS SUDDENLY A VIOLATION OF HIS CONSTITUTIONAL RIGHTS:

Trevor Potter, a former FEC chairman who is McCain's top lawyer, immediately disputed the assertions in Mason's letter, saying McCain has a constitutional right to exit the federal program.Which leaves our fearless leader with about 5 million to spend for all the rest of the primary season. I think I will be sending ole Huck some money tomorrow.

This, folks, is hubris. Those whom the gods wish to destroy, they first make mad. If McCain ignores this law he's in deep, deep shit, and the Republican party better be finding themselves another candidate like yesterday. He didn't have to apply in the first place. He didn't have to promise the bank that he would get matching funds if necessary. Once he did, he can't pretend he didn't.

By the way, the NY Sun editorial outlines the SpeechNow case:

The group differs from other so-called 527 nonprofits. It refuses to take donations from corporations or labor, meaning it only solicits from individuals. Its aim is to let voters know where the various candidates stand on free speech issues, including campaign finance regulation. It would purchase advertising and endorse or criticize candidates based on their voting record on free speech.Yup. And now I've got to hear McCain's lawyer talking about his constitutional rights?

...

By discouraging people from forming groups the FEC discourages civil society through regulation. A wealthy individual, such as William Gates, would be free to spend $1 billion purchasing airtime to devote attention to just about any issue or candidate he so wished. But 1,000 individuals of modest incomes could be prohibited from organizing into a committee and spending $20,000 a piece to purchase equal airtime to disagree with whatever issue so concerned Mr. Gates. The geniuses in Congress have made free speech into something you must register for at the FEC.

The Climate Scientists Complain Of Censorship?

Roger Pielke Sr has an excellent Climate Science blog. Climate science is what the man does. His latest entry discusses his inability to get a summary of climate scientists' actual views published in mainstream venues. He writes, in part:

It would be odd indeed if scientists in any discipline as complex and novel as climate science were to be monolithic on such a question. Roger Pielke's views aren't easily slotted and can be found here.

My all-time favorite climate science blog is Climate Audit. It can be extremely technical, but is often lighthearted. The main focus in on the quality of the research and data. It is the botfly of such efforts and is producing very healthy change (amid hatred).

PS: My favorite science blog is The Reference Frame. This man is a gifted teacher, as evidenced by posts such as How To Disprove Spoon Bending. He is also hilariously politically incorrect.

From this experience, it is clear that the AGU EOS and Nature Precedings Editors are using their positions to suppress evidence that there is more diversity of views on climate, and the human role in altering climate, than is represented in the narrowly focused 2007 IPCC report.The paper is published below the explanation on his blog at the link above and is interesting. There's an approximately 18% tail in either direction (IPCC overstates/understates), and about 47% agree. Of course some didn't like being put into a box and felt their views were more complex. Since I didn't see this poll as being a threat to the idea that climate scientists take the threat of CO2 forced climate change seriously, it surprised me that it would be rejected. I suppose one could claim that it was rejected for other reasons.

Our article follows below. We invite colleagues who are expert in polling techniques to build on the polling questions that we pose in our contribution, and to provide the community and policymakers with the actual range of perspectives on climate science.

It would be odd indeed if scientists in any discipline as complex and novel as climate science were to be monolithic on such a question. Roger Pielke's views aren't easily slotted and can be found here.

My all-time favorite climate science blog is Climate Audit. It can be extremely technical, but is often lighthearted. The main focus in on the quality of the research and data. It is the botfly of such efforts and is producing very healthy change (amid hatred).

PS: My favorite science blog is The Reference Frame. This man is a gifted teacher, as evidenced by posts such as How To Disprove Spoon Bending. He is also hilariously politically incorrect.

Stupidity To The Fifth Power

Ah, heck. I read this Bloomberg article this morning and felt like hanging it all up. There's too much BS in this article to cover without citing more than half of it. The bottom line is that no, when a lawyer goes to court and points out to the judge that the outfit trying to foreclose on his or her client hasn't shown they own the mortgage, the judge is not being some sort of social activist by requesting the documents to prove it. Statements like:

For example, the Chief ran into this once. What happened is that the organization that owned his mortgage merged with another, and then sold a piece. So two entities merged, and then were split into two entities. Due to a little problem with recordkeeping, it ended up that both of the final entities had his one mortgage on their individual books. Both were trying to collect and he switched making payments between entities when contacted and told that he was making payments to the wrong place. He made every payment, spent months trying to prove to each of them that he had made every payment, hired a lawyer to write a letter, and still a foreclosure action was filed. He and the lawyer went to court with the original note and proof of payment, and the judge dismissed the foreclosure. As part of the dismissal it was stipulated which entity had rights to the payments and the other entity had to transfer the payments it had to the entity that rightfully owned the mortgage. The late charges were cancelled, etc. It took another year and a half to get the loan books fixed and all the payments properly credited.

The idea that these documents are a "waste of time" is beyond crazy. Obviously the recent climate has the potential to generate confusion, but that only serves to point out the necessity of covering all the bases. To imply that judges are the problem here is quite an amazing legal theory.

I cannot believe that some of the lawyers quoted in this article were lunatic enough to make these statements. Of my immediate family, every single one have had problems with their mortgages. Every one - and it hasn't been that the payments were missing. When servicing is transferred it is not rare to have some confusion, but it is very odd indeed to have lawyers claiming that legal documents establishing ownership are erroneous and irrelevant. With every month that passes I grow more convinced that we are eventually going to have more federal legislation to deal with the excesses of an industry that has grown fat, criminally arrogant, sloppy, and proud of it.

I hope Tanta goes to town on this.

I do not believe for one moment that most of these documents have been lost. I just think everyone is trying to operate as cheaply as possible and becoming irate when called on the sloppiness. Remember CW's "fake but accurate" escrow letters? The bottom line is that the homeowner either made payments or didn't. If they did but the payments got mislaid in the shuffle, the homeowner will have to prove payment in court. If they didn't, making sure that the legal owner of the debt is the entity that sells the property and take the proceeds is quite important.

For example, in at least some states failure to file the original mortgage or deed of trust within a certain period will result in losing your claim to the property. You'll still have a debt, and you can go to court to collect, but you don't have the legal right to foreclose for nonpayment of that debt. You'd have to get a judgment and then file against the property to satisfy the judgment, but if anyone else had since lent against it, you'd be up a creek without a paddle. An expensive error - but look at it another way. If someone applies for a loan secured by that property, and you never recorded your lien, and the subsequent creditor couldn't find any trace of it and so lent money secured by a free and clear property, why should they pay for your mistake? Perfection of security is always the responsibility of the creditor. How can a meaningful system work otherwise? It is the same with mortgages.

If people are buying mortgages without bothering to verify the legal provenance they're crazily stupid, and you cannot blame a judge for other people's crazy stupidity. But I believe that the ownership is really known in almost all cases, and that these foreclosures are being sloppily prepared. I do have questions as to why the homeowners would spend all the money for legal fees unless they believe that they eventually have a good chance of keeping the property, which would imply that they think there is something wrong with the reported arrears, so I find the headline on this article "Banks Lose to Deadbeat Homeowners as Loans Sold in Bonds Vanish" a bit demented.

Believe me, if community banks operated like this they'd be out of business in a heartbeat.

There is one reason why lawyers might routinely file affidavits saying the note was lost when it wasn't. That is to avoid potential grounds for litigation due to improper booking, rate adjustment or transfer of the loan. Oddly enough, many borrowers do not keep their copies of the original note or notes. This passage raises a lot of questions:

Requiring banks to produce the paperwork at a foreclosure hearing is a nuisance, said Jeffrey Naimon, a partner in the Washington office of Buckley Kolar LLP.Bullshit. Why does MERS, the industry standard, require that the proper documentation be produced before they add it to their system? They don't want the liabilities, that's why. If you don't verify that the true owner of the debt is foreclosing, you may in fact be giving property owned by someone else to an entity with no claim. You may also be wrongfully foreclosing on the owner. It does happen.

``It's a gigantic waste of time,'' Naimon said. ``The mortgage may have transferred five, six, eight times. It's possible that you don't have all the pieces of paper, but it was enough to convince the next guy in the chain. There's no true controversy over whether the owner owns the loan.''

For example, the Chief ran into this once. What happened is that the organization that owned his mortgage merged with another, and then sold a piece. So two entities merged, and then were split into two entities. Due to a little problem with recordkeeping, it ended up that both of the final entities had his one mortgage on their individual books. Both were trying to collect and he switched making payments between entities when contacted and told that he was making payments to the wrong place. He made every payment, spent months trying to prove to each of them that he had made every payment, hired a lawyer to write a letter, and still a foreclosure action was filed. He and the lawyer went to court with the original note and proof of payment, and the judge dismissed the foreclosure. As part of the dismissal it was stipulated which entity had rights to the payments and the other entity had to transfer the payments it had to the entity that rightfully owned the mortgage. The late charges were cancelled, etc. It took another year and a half to get the loan books fixed and all the payments properly credited.

The idea that these documents are a "waste of time" is beyond crazy. Obviously the recent climate has the potential to generate confusion, but that only serves to point out the necessity of covering all the bases. To imply that judges are the problem here is quite an amazing legal theory.

I cannot believe that some of the lawyers quoted in this article were lunatic enough to make these statements. Of my immediate family, every single one have had problems with their mortgages. Every one - and it hasn't been that the payments were missing. When servicing is transferred it is not rare to have some confusion, but it is very odd indeed to have lawyers claiming that legal documents establishing ownership are erroneous and irrelevant. With every month that passes I grow more convinced that we are eventually going to have more federal legislation to deal with the excesses of an industry that has grown fat, criminally arrogant, sloppy, and proud of it.

I hope Tanta goes to town on this.

I do not believe for one moment that most of these documents have been lost. I just think everyone is trying to operate as cheaply as possible and becoming irate when called on the sloppiness. Remember CW's "fake but accurate" escrow letters? The bottom line is that the homeowner either made payments or didn't. If they did but the payments got mislaid in the shuffle, the homeowner will have to prove payment in court. If they didn't, making sure that the legal owner of the debt is the entity that sells the property and take the proceeds is quite important.

For example, in at least some states failure to file the original mortgage or deed of trust within a certain period will result in losing your claim to the property. You'll still have a debt, and you can go to court to collect, but you don't have the legal right to foreclose for nonpayment of that debt. You'd have to get a judgment and then file against the property to satisfy the judgment, but if anyone else had since lent against it, you'd be up a creek without a paddle. An expensive error - but look at it another way. If someone applies for a loan secured by that property, and you never recorded your lien, and the subsequent creditor couldn't find any trace of it and so lent money secured by a free and clear property, why should they pay for your mistake? Perfection of security is always the responsibility of the creditor. How can a meaningful system work otherwise? It is the same with mortgages.

If people are buying mortgages without bothering to verify the legal provenance they're crazily stupid, and you cannot blame a judge for other people's crazy stupidity. But I believe that the ownership is really known in almost all cases, and that these foreclosures are being sloppily prepared. I do have questions as to why the homeowners would spend all the money for legal fees unless they believe that they eventually have a good chance of keeping the property, which would imply that they think there is something wrong with the reported arrears, so I find the headline on this article "Banks Lose to Deadbeat Homeowners as Loans Sold in Bonds Vanish" a bit demented.

Believe me, if community banks operated like this they'd be out of business in a heartbeat.

There is one reason why lawyers might routinely file affidavits saying the note was lost when it wasn't. That is to avoid potential grounds for litigation due to improper booking, rate adjustment or transfer of the loan. Oddly enough, many borrowers do not keep their copies of the original note or notes. This passage raises a lot of questions:

Nobody knows how widespread the use of lost-note affidavits are, Charney said. She's had foreclosure proceedings for 300 clients dismissed or postponed in the past year, with about 80 percent of them involving lost-note affidavits, she said.If they are the rule something is wrong.

``They raise the issue of whether the trusts own the loans at all,'' Charney said. ``Lost-note affidavits are pattern and practice in the industry. They are not exceptions. They are the rule.''

Thursday, February 21, 2008

Rut Roh - Philly Fed

Not as good as I hoped. Employment moved up a bit, the diffusion index moved down. The six month outlook is the killer:

The outlook for manufacturing growth over the next six months deteriorated further this month. The future general activity index declined from 5.2 in January to -16.9, its first negative reading since January 2001 and the lowest reading since 1990.That's truly bad. I have a mental bet with myself as to how long the pay for play economists can continue to deny a recession. Some may string it out for a few more months. Even supposing that the six month trend turned out to be far more favorable than these numbers suggest, it is likely that many manufacturing businesses will be in cost-cutting mode with numbers like these. The cycle of reinforcing cost-cuts that marks the second phase of a recession appears to be underway in a more intense fashion than the 2001 recession.

Rut Roh - Unemployment Claims

This week the four-week rolling average for SA initial claims moved up to 360,500. Generally a 4 week rolling average above 350,000 is considered recessionary by mainstream economists.

The headlines are pretty funny, because initial claims are supposed to have dropped 9,000 this week to 349,000. However that is not exactly comforting, because the previous week's advance figure was 348,000, which was revised upward to 358,000. Therefore the actual weekly trajectory for initial claims is up, not down. The trend of upward revisions on initial claims continues so it is exceedingly likely that this week's initial claims figure will be revised up next week.

I wonder how much of this relates to government jobs. The financial situation for quite a few states and even more municipalities can best be described as "strapped" and at the very least, many jobs opened by retirements are not being filled again. FUT treasury receipts still look strong, but government employers do not pay FUT, so a relative weakness in government jobs does not show up in FUT.

Continuing claims still show relative strength. The NSA number dropped, but the SA number rose nearly 50,000. Even though construction employment has diminished, at this time of the year construction employment is affected by weather, which can throw the seasonal adjustments off.

Overall a constraint on government employment accompanied by relative strength in private employment is a good trend. In the short term, it is likely to be extraordinarily painful because of the discrepancy between the wages and benefits paid to public sector employees versus private sector employees. This too must end for the overall economy to rebound without the need for bubbles and bizarre equity valuations.

Needless to say the ongoing problems with muni ARS bonds are not going to help government employment and spending.

The headlines are pretty funny, because initial claims are supposed to have dropped 9,000 this week to 349,000. However that is not exactly comforting, because the previous week's advance figure was 348,000, which was revised upward to 358,000. Therefore the actual weekly trajectory for initial claims is up, not down. The trend of upward revisions on initial claims continues so it is exceedingly likely that this week's initial claims figure will be revised up next week.

I wonder how much of this relates to government jobs. The financial situation for quite a few states and even more municipalities can best be described as "strapped" and at the very least, many jobs opened by retirements are not being filled again. FUT treasury receipts still look strong, but government employers do not pay FUT, so a relative weakness in government jobs does not show up in FUT.

Continuing claims still show relative strength. The NSA number dropped, but the SA number rose nearly 50,000. Even though construction employment has diminished, at this time of the year construction employment is affected by weather, which can throw the seasonal adjustments off.

Overall a constraint on government employment accompanied by relative strength in private employment is a good trend. In the short term, it is likely to be extraordinarily painful because of the discrepancy between the wages and benefits paid to public sector employees versus private sector employees. This too must end for the overall economy to rebound without the need for bubbles and bizarre equity valuations.

Needless to say the ongoing problems with muni ARS bonds are not going to help government employment and spending.

Wednesday, February 20, 2008

Filed Under "Hoist By Your Own Petard"

CPI-W** (from CPI release here):

Farming is fuel-intensive in most areas. The move to ethanol is likely making the overall energy situation worse instead of better, but it is producing a relative boom in grain-farming states. The split between the 7.7% annualized rate for the last quarter for all items and the 3.1% annualized rate for ex-food and energy is a sign that discretionary spending is truly constrained and limiting inflation. However, the corollary is that profits in businesses related to most consumer discretionary spending will continue to go down. This includes utilities such as phone service. For example, AT&T and Verizon are duelling with flat-rate calling plans.

Another sign that consumers are really being hammered is that the 12-month rate for food is higher than the 3-month rate for food (4.6% vs 5.0%). The higher diesel costs (started moving up in the fall) should be pushing up food prices much faster, but instead end consumer prices are being relatively cut a bit in a war to maintain volume. This will not last.

When looking at the reported retail sales figures for the Nov/Dec/Jan period, it is clear that inflation-adjusted sales are dropping, which accounts for the fact that the true rise in costs is not moving into CPI yet. Almost everyone in the consumer supply chain is taking a hit to maintain volume.

The type of inflation we are seeing is probably not very susceptible to monetary policy. Opening up new internal sources of energy would help a great deal.

The last PPI release is here. Look at the finished goods contrast:

The strong implication is that resourcing to internal sources is likely to occur wherever possible. A weaker dollar and relatively global energy/grain demand, plus these statistics, seem to almost guarantee that insourcing will grow. This can occur in anything from oranges to oil.

So the first petard is the US' poor energy policy. Recently I pointed out that gas consumption seems to be dropping, so it seems that in fact the population is conserving. However we haven't built energy plants like nuclear power, etc, which could help our overall situation. When you burn grains for fuel, you do push up the cost of animal and grain foods. The type of inflation that the US is seeing is highly regressive. It hurts the lower income earners far worse than the higher income earners, and it is difficult to avoid. this type of inflation. Indeed, in some cases the higher income earners who can buy new vehicles, etc, got a big bonus last year as prices for durables generally dropped.

And this phenomenon brings me to politics. I have been reading the Clinton campaign's explanations as to their continuing drop in the polls with great interest. They are very far from connecting with reality. I read at least one Democratic forum pretty regularly, and the Clinton campaign was badly hurt by the idea of mandating the purchase of health insurance, and either preventing employment for the uninsured or garnishing wages. Real median household income in the US has not risen overall for years now:

The decline in construction certainly impacted incomes last year as well, and in a negative direction. The decline in WIET receipts reported in the last few months strongly supports the idea that real median household incomes aren't rising now. Additionally, many individuals are involved in contracting, construction, manufacturing etc, which are fluctuating at best.

Imagine yourself as a worker who has experienced several different periods of prolonged layoffs in the last 15 years. You are not wowed by the prospect of someone telling you that you must purchase health insurance when you have experienced periods in which you had difficulty keeping the lights on and food on the table. A plan that subsidizes a part of health insurance for you sounds good, but at any given time it is not clear that you will have the money to pay the monthly subsidized fee. Your prior year income may have been excellent, and this year's income may be much lower. Hillary really hurt herself with this proposal. Massachusetts tried it, and it hasn't succeeded there either, although they are just taxing people who don't have health insurance.

As far as the male vote goes, Hillary's health care proposals alone must be a substantial worry. There are a very large number of men paying child support in this country. They are subject to being jailed if they don't pay, and many of them could not make their child support payments and buy insurance for themselves.

The second problem Hillary's campaign is suffering is the tendency of Hillary supporters to scream about sexism whenever things turn down. I strongly believe that Obama's relative strength among men in Wisconsin was assisted by the wails about sexism. I do not believe that most males are indeed sexist, but they are certainly going to be deeply turned off by being accused of it. Hillary's campaign was deeply damaged after the debate in which her secret plan to fix Social Security and her confusion on the question of licenses for illegal immigrants were questioned. Her supporters responded with wrath and the meme that the men had "ganged up" on her. It was not a Maggie Thatcher like performance. The somewhat acerbic negativity toward Obama did not help. Nor did the failure to congratulate him. The picture which is building up in many voters' minds is of a women who is very unwilling to be questioned and may be angry when questioned.

I believe that the Clinton campaign is fundamentally out of touch with the economic realities facing a lot of their target voters. Those voters want jobs. They would love help with health insurance, but are very doubtful that the government will get it right the first time. What they really need are jobs - good paying jobs.

Here's a dose of economic reality. MSN just published one of its helpful career oriented articles about the best states for employment. They listed the 15 states with the lowest unemployment rates, plus some other details:

2006 was about the top in some of these states. Because construction incomes were relatively high, the decline in construction is cutting into both jobs and incomes. Since half of all households will have incomes below the median income shown, it's a pretty good guess that about 30% of all households don't have a flaming chance in hell of maintaing coverage unless there is a very substantial subsidy. Massachusetts is already cutting provider reimbursements and those insured under the subsidized plan may be facing major premium increases. The state is facing some major financial difficulties due to much higher than expected costs. They are now appealing to the federal government to pick up more of the cost.

The maximum out of pocket expense for a single person in Massachusetts was set at $5,000. The coverage standards can be found here and include mental health coverage plus prescription drug coverage. The affordability standards are here. A couple making between 40-50K can be required to pay no more than $270 premium per month. Needless to say, it is very difficult to provide this type of insurance for a couple in their 50s for this type of premium, so the result has been that many more individuals are shifting to the subsidized plans.

** Correction helpfully sent in by JWalker who noticed I had labelled it CPI-U.

Expenditure CompoundApproximately 1/6th of the population gets Social Security. Last year's COLA of 2.3% isn't going to be doing much for them at this point. The average retiree gets more than half their retirement income from Social Security, and CPI is usually used to adjust other retirement benefits (if they adjust at all).

Category Changes from preceding month annual Un-

rate adjusted

3-mos. 12-mos.

July Aug. Sep. Oct. Nov. Dec. Jan. ended ended

2007 2007 2007 2007 2007 2007 2008 Jan. 2008 Jan. 2008

All items.......... .2 .0 .4 .3 1.0 .4 .4 7.7 4.6

Food and beverages .3 .5 .5 .2 .3 .1 .7 4.5 4.9

Housing........... .1 .0 .2 .3 .4 .2 .2 3.5 3.1

Apparel........... .5 -.2 .0 .1 .4 .2 .8 5.6 .5

Transportation.... .3 -.6 .7 .3 3.8 1.1 .7 24.6 10.2

Medical care...... .6 .5 .4 .5 .4 .3 .6 5.4 5.1

Recreation........ -.1 -.1 .3 .2 .1 .1 .2 1.3 .7

Education and

communication.. .2 .3 .1 .3 .0 .2 .3 2.2 3.0

Other goods and

services....... .2 .1 .4 .2 .2 .4 .5 4.5 3.4

Special indexes:

Energy............ .1 -1.8 1.4 1.1 7.2 1.8 .8 45.9 20.4

Food.............. .3 .5 .5 .2 .3 .1 .7 4.6 5.0

All items less

food and energy .2 .2 .2 .2 .2 .2 .3 3.1 2.4

Consumer Price Index data for February are scheduled for release on

Friday, March 14, 2008, at 8:30 A.M. (EDT).

Farming is fuel-intensive in most areas. The move to ethanol is likely making the overall energy situation worse instead of better, but it is producing a relative boom in grain-farming states. The split between the 7.7% annualized rate for the last quarter for all items and the 3.1% annualized rate for ex-food and energy is a sign that discretionary spending is truly constrained and limiting inflation. However, the corollary is that profits in businesses related to most consumer discretionary spending will continue to go down. This includes utilities such as phone service. For example, AT&T and Verizon are duelling with flat-rate calling plans.

Another sign that consumers are really being hammered is that the 12-month rate for food is higher than the 3-month rate for food (4.6% vs 5.0%). The higher diesel costs (started moving up in the fall) should be pushing up food prices much faster, but instead end consumer prices are being relatively cut a bit in a war to maintain volume. This will not last.

When looking at the reported retail sales figures for the Nov/Dec/Jan period, it is clear that inflation-adjusted sales are dropping, which accounts for the fact that the true rise in costs is not moving into CPI yet. Almost everyone in the consumer supply chain is taking a hit to maintain volume.

The type of inflation we are seeing is probably not very susceptible to monetary policy. Opening up new internal sources of energy would help a great deal.

The last PPI release is here. Look at the finished goods contrast:

| | Percentage | |

| | change 12 | Seasonally adjusted annual |

| | months ended | rate for 3 months ended |

| Grouping | in December |-----------------------------|

| |--------------------| March | June | Sept. | Dec. |

| | 2005 | 2006 | 2007 | 2007 | 2007 | 2007 | 2007 |

|----------------------------------------------------------------------------------|

Finished goods 5.4 1.1 6.3 6.9 6.5 1.0 13.3

Finished consumer foods 1.7 1.7 7.4 18.7 -1.7 4.2 9.4

Finished energy goods 23.9 -2.0 18.4 10.0 29.5 -3.0 51.9

Finished goods less foods

and energy 1.4 2.0 2.0 2.0 2.3 1.7 2.2

Finished consumer goods,

excluding foods and energy 1.6 1.8 2.5 2.2 2.9 2.1 2.8

Capital equipment 1.2 2.3 1.3 1.6 1.3 1.1 1.3

Intermediate materials,

supplies, and components 8.6 2.8 6.8 5.4 10.4 -.5 15.0

Intermediate foods and feeds 2.4 4.7 17.5 29.5 11.7 10.5 19.2

Intermediate energy goods 26.2 -3.3 18.6 16.3 24.2 -3.6 55.3

Intermediate materials less

foods and energy 4.8 4.5 3.3 1.7 6.9 0 4.6

Materials for nondurable

manufacturing 8.9 1.2 13.0 8.1 21.3 3.3 20.3

Materials for durable

manufacturing 5.9 12.5 1.6 2.2 19.5 -11.6 -1.5

Materials and components

for construction 6.1 4.3 1.8 2.6 3.6 .6 .4

Crude materials for further

processing 21.1 -4.7 20.6 25.1 14.8 -8.5 59.6

Foodstuffs and feedstuffs 1.6 2.8 25.2 60.7 12.6 11.3 19.2

Crude energy materials 42.2 -15.7 17.2 -11.3 26.3 -26.9 129.5

Crude nonfood materials

less energy 5.2 17.0 16.8 60.1 0 12.4 3.6

The strong implication is that resourcing to internal sources is likely to occur wherever possible. A weaker dollar and relatively global energy/grain demand, plus these statistics, seem to almost guarantee that insourcing will grow. This can occur in anything from oranges to oil.

So the first petard is the US' poor energy policy. Recently I pointed out that gas consumption seems to be dropping, so it seems that in fact the population is conserving. However we haven't built energy plants like nuclear power, etc, which could help our overall situation. When you burn grains for fuel, you do push up the cost of animal and grain foods. The type of inflation that the US is seeing is highly regressive. It hurts the lower income earners far worse than the higher income earners, and it is difficult to avoid. this type of inflation. Indeed, in some cases the higher income earners who can buy new vehicles, etc, got a big bonus last year as prices for durables generally dropped.

And this phenomenon brings me to politics. I have been reading the Clinton campaign's explanations as to their continuing drop in the polls with great interest. They are very far from connecting with reality. I read at least one Democratic forum pretty regularly, and the Clinton campaign was badly hurt by the idea of mandating the purchase of health insurance, and either preventing employment for the uninsured or garnishing wages. Real median household income in the US has not risen overall for years now:

The decline in construction certainly impacted incomes last year as well, and in a negative direction. The decline in WIET receipts reported in the last few months strongly supports the idea that real median household incomes aren't rising now. Additionally, many individuals are involved in contracting, construction, manufacturing etc, which are fluctuating at best.

Imagine yourself as a worker who has experienced several different periods of prolonged layoffs in the last 15 years. You are not wowed by the prospect of someone telling you that you must purchase health insurance when you have experienced periods in which you had difficulty keeping the lights on and food on the table. A plan that subsidizes a part of health insurance for you sounds good, but at any given time it is not clear that you will have the money to pay the monthly subsidized fee. Your prior year income may have been excellent, and this year's income may be much lower. Hillary really hurt herself with this proposal. Massachusetts tried it, and it hasn't succeeded there either, although they are just taxing people who don't have health insurance.

As far as the male vote goes, Hillary's health care proposals alone must be a substantial worry. There are a very large number of men paying child support in this country. They are subject to being jailed if they don't pay, and many of them could not make their child support payments and buy insurance for themselves.

The second problem Hillary's campaign is suffering is the tendency of Hillary supporters to scream about sexism whenever things turn down. I strongly believe that Obama's relative strength among men in Wisconsin was assisted by the wails about sexism. I do not believe that most males are indeed sexist, but they are certainly going to be deeply turned off by being accused of it. Hillary's campaign was deeply damaged after the debate in which her secret plan to fix Social Security and her confusion on the question of licenses for illegal immigrants were questioned. Her supporters responded with wrath and the meme that the men had "ganged up" on her. It was not a Maggie Thatcher like performance. The somewhat acerbic negativity toward Obama did not help. Nor did the failure to congratulate him. The picture which is building up in many voters' minds is of a women who is very unwilling to be questioned and may be angry when questioned.

I believe that the Clinton campaign is fundamentally out of touch with the economic realities facing a lot of their target voters. Those voters want jobs. They would love help with health insurance, but are very doubtful that the government will get it right the first time. What they really need are jobs - good paying jobs.

Here's a dose of economic reality. MSN just published one of its helpful career oriented articles about the best states for employment. They listed the 15 states with the lowest unemployment rates, plus some other details:

1. South DakotaThe wages cited are mean, not median. I added the Median household incomes for each state. It is not a good sign that government is the top industry in 33% (five) of these states. As for trade and transportation, truckers, especially independents, are taking a bad hit to income.

Unemployment rate: 3 percent*

Population: 796,214**

Mean annual wage: $30,460

Top industry: Trade, transportation and utilities (19.9 percent)***

Median Household Income 2006: $53,806

2. Idaho

Unemployment rate: 3 percent

Population: 1,499,402

Mean annual wage: $34,810

Top industry: Trade, transportation and utilities (20.2 percent)

Median Household Income 2006: $51,640

3. Wyoming

Unemployment rate: 3.1 percent

Population: 522,830

Mean annual wage: $34,290

Top industry: Government (23 percent)

Median Household Income 2006: $57,505

4. Nebraska

Unemployment rate: 3.2 percent

Population: 1,774,571

Mean annual wage: $34,300

Top industry: Trade, transportation and utilities (21.1 percent)

Median Household Income 2006: $56,940

5. Utah

Unemployment rate: 3.2 percent

Population: 2,645,330

Mean annual wage: $35,540

Top industry: Trade, transportation and utilities (19.7 percent)

Median Household Income 2006: $58,141

6. Hawaii

Unemployment rate: 3.2 percent

Population: 1,283,388

Mean annual wage: $38,630

Top industry: Government (19.6 percent)

Median Household Income 2006: $70,277

7. North Dakota

Unemployment rate: 3.3 percent

Population: 639,715

Mean annual wage: $32,440

Top industry: Trade, transportation and utilities (21.4 percent)

Median Household Income 2006: $55,385

8. Virginia

Unemployment rate: 3.5 percent

Population: 7,712,091

Mean annual wage: $41,450

Top industry: Government (18 percent)

Median Household Income 2006: $66,886

9. Montana

Unemployment rate: 3.6 percent

Population: 957,861

Mean annual wage: $31,290

Top industry: Trade, transportation and utilities (20.5 percent)

Median Household Income 2006: $51,006

10. New Hampshire

Unemployment rate: 3.6 percent

Population: 1,315,828

Mean annual wage: $39,250

Top industry: Trade, transportation and utilities (23.3 percent)

Median Household Income 2006: $71,176

11. New Mexico

Unemployment rate: 3.7 percent

Population: 1,969,915

Mean annual wage: $33,980

Top industry: Government (23.2 percent)

Median Household Income 2006: $48,199

12. Delaware

Unemployment rate: 3.8 percent

Population: 864,764

Mean annual wage: $41,680

Top industry: Trade, transportation and utilities (18.7 percent)

Median Household Income 2006: $62,623

13. Maryland

Unemployment rate: 3.8 percent

Population: 5,618,344

Mean annual wage: $44,030

Top industry: Government (18.2 percent)

Median Household Income 2006: $77,839

14. Iowa

Unemployment rate: 4 percent

Population: 2,988,046

Mean annual wage: $33,250

Top industry: Trade, transportation and utilities (20.4 percent)

Median Household Income 2006: $55,735

15. Vermont

Unemployment rate: 4 percent

Population: 621,254

Mean annual wage: $36,350

Top industry: Trade, transportation and utilities (19.4 percent)

Median Household Income 2006: $58,163

2006 was about the top in some of these states. Because construction incomes were relatively high, the decline in construction is cutting into both jobs and incomes. Since half of all households will have incomes below the median income shown, it's a pretty good guess that about 30% of all households don't have a flaming chance in hell of maintaing coverage unless there is a very substantial subsidy. Massachusetts is already cutting provider reimbursements and those insured under the subsidized plan may be facing major premium increases. The state is facing some major financial difficulties due to much higher than expected costs. They are now appealing to the federal government to pick up more of the cost.

The maximum out of pocket expense for a single person in Massachusetts was set at $5,000. The coverage standards can be found here and include mental health coverage plus prescription drug coverage. The affordability standards are here. A couple making between 40-50K can be required to pay no more than $270 premium per month. Needless to say, it is very difficult to provide this type of insurance for a couple in their 50s for this type of premium, so the result has been that many more individuals are shifting to the subsidized plans.

** Correction helpfully sent in by JWalker who noticed I had labelled it CPI-U.

Tuesday, February 19, 2008

Munis And Chickens

It truly worries me that the financial chickens are coming home to roost in a major election year. I'm sure we're going to see more and more wild ideas about how to reverse the entropy of bad debt. It is impossible to reverse the entropy of bad debt, just as it's impossible to make time flow backwards. You can convert so-so debt into more manageable debt by cutting the rates on it, but that's all.

The Alt-A and prime overleveraged stuff is going down, and it will deliver more of a punch than subprime.

As I wrote at the end of January, the final event was the demise of the monolines, and that impact is slowly trickling through the financial system. Calculated Risk is doing a great job covering the undignified brawl, but no one is discussing the one essential and basic point. Insurance regulators are just as incompetent at anyone else at assessing the risk on these complicated securities and of the funny-money mortgages. Therefore they are stuck cleaning up the wreckage, and I still believe that they will split most of the firms. They have no option other than to get the banks to pony up to recapitalize the firms, but if the banks have to pony up for the insurance and then essentially pay for the payouts, it's hardly a benefit. So the regulators are using the split to try to force the banks to change covenants and ante up, and now the banks are starting to threaten to litigate.

In the end the regulators will win on the basis of necessity.

The weirdness of Credit Suisse announcing that whoops! some traders mismarked some things, so now we have to change the figures we just released is probably going to generate some additional financial heartburn. They say they may have to restate 2007.

The overall picture is that no one knows the sum of the losses out there, or where they are hiding. So it's not as if banks and financials are going to feel comfortable about lending to each other.

And that observation brings us to the current situation with auction rate munis. The auctions are failing now. When the auction fails, a default rate goes into effect. The recent problems have sparked calls for more disclosure on the auctions. I think the suspicion is that some institutional buyers are going on strike, which has opened the market to manipulation by some players. Take, for example, the case of U of Pittsburg's Medical Center:

There are some genuinely bad munis out there, but a lot of them are along the same lines as this one. Not gold quality, but not junk debt either. Much more of this could have an incredibly strong effect on the US banking and financial system.

The Alt-A and prime overleveraged stuff is going down, and it will deliver more of a punch than subprime.

As I wrote at the end of January, the final event was the demise of the monolines, and that impact is slowly trickling through the financial system. Calculated Risk is doing a great job covering the undignified brawl, but no one is discussing the one essential and basic point. Insurance regulators are just as incompetent at anyone else at assessing the risk on these complicated securities and of the funny-money mortgages. Therefore they are stuck cleaning up the wreckage, and I still believe that they will split most of the firms. They have no option other than to get the banks to pony up to recapitalize the firms, but if the banks have to pony up for the insurance and then essentially pay for the payouts, it's hardly a benefit. So the regulators are using the split to try to force the banks to change covenants and ante up, and now the banks are starting to threaten to litigate.

In the end the regulators will win on the basis of necessity.

The weirdness of Credit Suisse announcing that whoops! some traders mismarked some things, so now we have to change the figures we just released is probably going to generate some additional financial heartburn. They say they may have to restate 2007.

The overall picture is that no one knows the sum of the losses out there, or where they are hiding. So it's not as if banks and financials are going to feel comfortable about lending to each other.

And that observation brings us to the current situation with auction rate munis. The auctions are failing now. When the auction fails, a default rate goes into effect. The recent problems have sparked calls for more disclosure on the auctions. I think the suspicion is that some institutional buyers are going on strike, which has opened the market to manipulation by some players. Take, for example, the case of U of Pittsburg's Medical Center:

The hospital offered to buy back $91 million of its debt yesterday, and will make similar offers for almost $340 million more, according to Tal Heppenstall, UPMC's treasurer. Holders have until March 19 to sell the bonds back for $100.01 of par value plus accrued interest, according to a notice posted on Bloomberg.Needless to say, the draw on the bank funds takes money away from other lending, although it is profitable business for the local banks. Since the last two auction rates were over 16%, a bank can make a nice chunk of change and will. Presumably the local lines will be paid back when the debt is rolled over to long-term debt.

Funding costs soared nationwide in the $330 billion market for auction-rate securities as banks from Citigroup Inc. to Goldman Sachs Group Inc. stopped bidding for the debt at the periodic sales they organize.

...

After repurchasing the auction-rate securities using local bank credit lines, the Pittsburgh hospital plans to issue long- term, fixed-rate debt, Heppenstall said.

``We put up with this for a week, but that's enough.''

There are some genuinely bad munis out there, but a lot of them are along the same lines as this one. Not gold quality, but not junk debt either. Much more of this could have an incredibly strong effect on the US banking and financial system.

Sunday, February 17, 2008

Surviving A Recession, Part II

It's important to start early. Pay down debt, pull money out of your HELOC before your bank yanks it, and cut back your daily living expenses. The margin for changing jobs is a tight one. It's obviously better to bail early if you think your company is in difficulty, but you don't want to put yourself in the "last hired, first fired" bracket with a reckless job change either.