MaxedOutMama

MaxedOutMama

Thursday, November 29, 2012

Ain't It Just

As TJ notes, "hard to write that MMT column when every other word is four letters." Uh-huh. Yeah.

I wouldn't normally be so whacked out, except that the economic news is rather ugly and I am losing my objectivity over the negativity. I looked at this morning's initial claims and promptly generated a whirlwind of brilliant explanations as to why these figures don't mean what they seem to mean.In other words, I'm BSing myself.

I will not inflict the BS on you - there's plenty available for free. The initial claims report is here. There may even be some small chance that some of my brilliant explanations as to why this report doesn't mean what it seems to mean have some merit, but the fact is that the four-week MA is 405K, and this marks an unlovely signpost in that last year it was 392K. Furthermore, this week's SA claims are 393K, which tends to suggest that some of my brilliant explanations are completely false.

Every human being is condemned to fight a lifelong battle against his or her own tendency to fantasize reality. The truth is that getting what we want can only be achieved by struggling to recognize the worst aspects of our current reality so that we can improve upon them. The worst of it is that the more intelligent a person is, the greater the ability to construct an attractive and plausible detailed network of explanations as to why one's preferred reality is the reality, so intelligence is not the answer. Nor is plausibility.

No, the answer is to pin your worldview to a framework of evidence, and to nail your own mental BS to that framework of evidence when you start to slide into fantasy. At times like these, this can be a painful process, but I now have to do it to myself. I do not want to be a walking, talking ID 10 T error, and if I don't correct this now, I may end up adopting MMT myself.

Economics always contains huge evidential uncertainties, and so it is a very seductive field for fantasists. I can't afford to let myself join that crowd, and right now my inner toddler is just begging for admission to that club.

I wouldn't normally be so whacked out, except that the economic news is rather ugly and I am losing my objectivity over the negativity. I looked at this morning's initial claims and promptly generated a whirlwind of brilliant explanations as to why these figures don't mean what they seem to mean.In other words, I'm BSing myself.

I will not inflict the BS on you - there's plenty available for free. The initial claims report is here. There may even be some small chance that some of my brilliant explanations as to why this report doesn't mean what it seems to mean have some merit, but the fact is that the four-week MA is 405K, and this marks an unlovely signpost in that last year it was 392K. Furthermore, this week's SA claims are 393K, which tends to suggest that some of my brilliant explanations are completely false.

Every human being is condemned to fight a lifelong battle against his or her own tendency to fantasize reality. The truth is that getting what we want can only be achieved by struggling to recognize the worst aspects of our current reality so that we can improve upon them. The worst of it is that the more intelligent a person is, the greater the ability to construct an attractive and plausible detailed network of explanations as to why one's preferred reality is the reality, so intelligence is not the answer. Nor is plausibility.

No, the answer is to pin your worldview to a framework of evidence, and to nail your own mental BS to that framework of evidence when you start to slide into fantasy. At times like these, this can be a painful process, but I now have to do it to myself. I do not want to be a walking, talking ID 10 T error, and if I don't correct this now, I may end up adopting MMT myself.

Economics always contains huge evidential uncertainties, and so it is a very seductive field for fantasists. I can't afford to let myself join that crowd, and right now my inner toddler is just begging for admission to that club.

Wednesday, November 28, 2012

My G_d

New Home sales came in crushingly low. It's not just this month's figure - it's the prior month's revisions, which now make a three month SA trend between 366-368, far below the 380s trend that everyone thought we had going.

Since May, then, we have gone from 369 to 368 seasonally adjusted, with a low of 360 (June) and a high of 369 (May, Sept). In other words, no raw growth EDGE at all.

Obviously mortgage rates aren't going to be providing additional momentum in 2013.

Hey - If you want to be conspiratorial and all, one might question just what the h_ll happened here and if there was any political bias this summer.

In the US economy, if you've lost the growth edge on autos and the growth edge on housing, you've lost your growth edge. Nothing is holding us up now but the season of Bling, and that is followed by the season of Ding quite inevitably.

This doesn't surprise me, honestly. I was favorably surprised by the better figures we thought we had. Next year mortgage regulation is unfavorable to risk, so there's a bad wind a'blowing. All this talk about the fiscal cliff is bravely ignoring our current situation.

PS: I was honestly and truly going to do the MMT thing today (late), but now I am sitting and staring in shock.

Since May, then, we have gone from 369 to 368 seasonally adjusted, with a low of 360 (June) and a high of 369 (May, Sept). In other words, no raw growth EDGE at all.

Obviously mortgage rates aren't going to be providing additional momentum in 2013.

Hey - If you want to be conspiratorial and all, one might question just what the h_ll happened here and if there was any political bias this summer.

In the US economy, if you've lost the growth edge on autos and the growth edge on housing, you've lost your growth edge. Nothing is holding us up now but the season of Bling, and that is followed by the season of Ding quite inevitably.

This doesn't surprise me, honestly. I was favorably surprised by the better figures we thought we had. Next year mortgage regulation is unfavorable to risk, so there's a bad wind a'blowing. All this talk about the fiscal cliff is bravely ignoring our current situation.

PS: I was honestly and truly going to do the MMT thing today (late), but now I am sitting and staring in shock.

Tuesday, November 27, 2012

Durables

The advance report is here. The only thing that really matters about this now is motor vehicles, because that is what is going to move the economy up or down. Unfortunately, October was not a good month in that respect. Inventories have risen for three months and unfilled orders have declined. It is in no sense a catastrophic decline, but it is hard to look at this report and not think that autos have topped out.

This does not surprise me at all, because as the summer wore on the auto advertising became increasingly desperate and moved up the economic ladder - so now all of a sudden Lexis dealerships were advertising ridiculously cheap lease deals, I started to hear radio ads for the 12-month no payments thing, etc. Auto financing terms have gotten as lax as they can be and will have to tighten, so there is less life in this whole shebang.

All other things being equal, this would not be a disaster. As autos paused and lost their position as the leading broad economic growth edge, residential construction would pick up and assume that position. We would not be poised for great growth, but we would be prevented from falling right through the bottom.

However all other things are not equal. There are not one, but two, deeply disruptive economic changes in store for the next two years. The first is the fiscal cliff thing - which will largely be avoided - but the second is Obamacare, which cannot be avoided. The mandate for individual coverage does not kick in until 2014, but the exchanges are supposed to be open in October 2013 so individuals can sign up. Businesses are forced to deal with the issue right now in their planning, and will make changes right through 2013 to implement their plans.

My estimate for Obama care is the loss of 1.2 million full-time jobs equivalent, which leaves us a very slack possible jobs gain over the next year and a half. A great deal of the loss is in hours, and it hits the consumer side of the economy strikingly hard. By the end of 2014, the unfortunates in this system will start defaulting on their mortgages and other loans again, so all by itself, Obamacare is a portfolio challenge for small banks.

And the fiscal impact on the 2014/2015 budget will be immense. The subsidies and Medicaid bills will be far higher cost than CBO has calculated. Ultimately, Obamacare will fail because it is utterly unfeasible economically, but the car wreck will be like on of those fog-generated massive chain accidents on some CA highway, and will tie up economic traffic for a very long time.

This does not surprise me at all, because as the summer wore on the auto advertising became increasingly desperate and moved up the economic ladder - so now all of a sudden Lexis dealerships were advertising ridiculously cheap lease deals, I started to hear radio ads for the 12-month no payments thing, etc. Auto financing terms have gotten as lax as they can be and will have to tighten, so there is less life in this whole shebang.

All other things being equal, this would not be a disaster. As autos paused and lost their position as the leading broad economic growth edge, residential construction would pick up and assume that position. We would not be poised for great growth, but we would be prevented from falling right through the bottom.

However all other things are not equal. There are not one, but two, deeply disruptive economic changes in store for the next two years. The first is the fiscal cliff thing - which will largely be avoided - but the second is Obamacare, which cannot be avoided. The mandate for individual coverage does not kick in until 2014, but the exchanges are supposed to be open in October 2013 so individuals can sign up. Businesses are forced to deal with the issue right now in their planning, and will make changes right through 2013 to implement their plans.

My estimate for Obama care is the loss of 1.2 million full-time jobs equivalent, which leaves us a very slack possible jobs gain over the next year and a half. A great deal of the loss is in hours, and it hits the consumer side of the economy strikingly hard. By the end of 2014, the unfortunates in this system will start defaulting on their mortgages and other loans again, so all by itself, Obamacare is a portfolio challenge for small banks.

And the fiscal impact on the 2014/2015 budget will be immense. The subsidies and Medicaid bills will be far higher cost than CBO has calculated. Ultimately, Obamacare will fail because it is utterly unfeasible economically, but the car wreck will be like on of those fog-generated massive chain accidents on some CA highway, and will tie up economic traffic for a very long time.

Monday, November 26, 2012

Just Recession Graphs of Various Types

The best first. You will find an explanation and links to papers at this link:

This approach has now been tested on two recessions since its intro in 1998. Oh, wait, make that three.... See the updated discussion here. The Chauvet-Piger method is strong and rapid. this summer we exceeded the lower bound, and now (October) it says we are in a recession. The interesting thing about this method is that it also "catches" the beginning of the 2006 industrial recession in the US, which few other indicators do.

The weakness of this method is that it catches the turning points, but it does so in real-time (six to nine months ahead of NBER), whereas one would like to have the Fed and gov get six month's warning so effective interventions were possible. But no, this doesn't do it.The bottom line here is that the Fed needed to do what it is doing now back in the spring to have any hope of fending this recession off. Readers of this blog may remember CF's comments early this year that the Fed would begin buying mortgage bonds in the spring. Haha. This is why CF has the jet and they don't. There's a theory out there that the Fed is going to launch a panic buying program of 80 (double) or so to try to deal with the situation. I don't think they can. I don't think there are enough bonds out there to support it.

CFNAI diffusion: CFNAI was released today. CFNAI also produces a diffusion index. You can find this graph in their release:

Once the 3-month diffusion index reaches -0.35 we are in a recession. According to this one, not yet, but almost (-0.32). Negative diffusion trends once you've completed the first inventory cycle after a recession always have to be watched, though. It would be unlikely to reach a diffusion point this low at this point in the business cycle without a succeeding recession, and by unlikely, I mean it doesn't really happen. Strong monetary expansions (which must include introducing the money and ensuring that it circulates) can create considerable lift at this point, but how is that possible now?

Once the 3-month diffusion index reaches -0.35 we are in a recession. According to this one, not yet, but almost (-0.32). Negative diffusion trends once you've completed the first inventory cycle after a recession always have to be watched, though. It would be unlikely to reach a diffusion point this low at this point in the business cycle without a succeeding recession, and by unlikely, I mean it doesn't really happen. Strong monetary expansions (which must include introducing the money and ensuring that it circulates) can create considerable lift at this point, but how is that possible now?

One really interesting thing about CFNAI diffusion, which can generally be reproduced in other countries with reliable economic data (not China) is that in a bubble, you will usually see the first dip, a pop and then a second dip as lending compensates. I do not use this for forecasting, but I do think it catches something very real and fundamental about the US economy, which is that the forces which create recessions usually move into a play a year before the actual recession.

The Texas manufacturing survey, which was my "strong" region, was very disappointing this month. This is kind of a kick in the M_O_M confidence, because all my wonderful hopes for something mildish in the recession line kind of depend on trends that are centered in this region. The DC envelope is of course still extant, but it is supported by a flood of government money that is inevitably going to be slowly throttled down, so it's nothing you can rely on.

I try to predict recessions a year out. Freight is very helpful, but these indicators are as well for shape and timing:

Really I track changes in disposable income and M_O_M calculated changes in real money supply, but these three sets of data serve as a useful check on my own numbers. The utilities change over time will give me a helpful read on sensitivity to changes in real money supply. When utility usage is stagnant, the economy is weak and very sensitive to negative changes. The current period of stagnation has endured since 2007, and is similar only to the period from 78-83.

Producer prices and consumer prices give me timing info. They will take an initial fall when the economy is seizing up, and then increase as we go into the full recession onset. Recessions have different shapes, and the price spread for businesses is one of the determining factors. When businesses find themselves with compressing profit margins due to high costs and price sensitivity in sales, they have to cut their operating costs, which generates waves of negative diffusion across the economy. This shows up in personal income trends:

Here we have a rather busy graph showing utilities (to show the correlation), real retail and food services sales in green, real disposable personal income and real personal consumption expenditures, and then, in purple, the dire real personal income excluding current transfer receipts.

In detail, the same series displayed so that you can see them:

To this one I have added the previous retail series in blue. So jagged blue and green are retail sales. Red/orange are real personal disposable personal income and Personal consumption (which captures non-retail sales as well). Then, in the heavy purple line, we have real personal income excluding government benefits, i.e., income generated by the private economy.

Now real personal income doesn't account for tax changes - remember that.

So now we come into a mild recessionary period with these mechanics. I have included the history so that you can see that the massive gap which opened up between the purple (privately generated income) and the red (all personal income less taxes) didn't exist in the 79-83 protracted slump.

It's blindingly obvious that spending is now dependent on government transfers to people. Whereas real personal consumption is higher than it was entering the recession, private incomes have not recovered nearly to the same point - they are back to 2006 levels. Nor are we closing the gap very fast at this point, which means that our tax basis isn't improving very much.

The gap may be widening now, which is what one would expect in a mild recession combined with a wave of retirements.

We are running a massive structural deficit:

Not surprisingly, this has generated a massive rise in issued federal government debt:

Company profits cannot be taxed at any levels that could remotely remedy the situation:

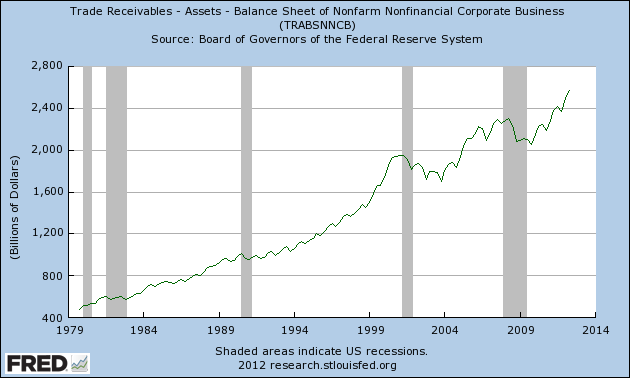

The first graph shows net worths - and note that on a market basis, net worths of nonfinancial corporations has not recovered to the pre-recession basis, much less grown. The bottom line - flow - trade receivables - shows that businesses are now growing, but with receivables at about 2.6 trillion, it is pretty obvious that you are not going to close a trillion dollar deficit by taxing corporate profits.

Furthermore, companies are borrowing to finance the growth you see:

So don't expect them not to be very responsive to tightening profits. They'll economize quickly, and they are sensitive to spreads of all kinds.

If you raise personal taxes a lot, you cut the purple line (income generated by the private economy), which may make things worse. Therefore, the problem is not really the recession we've got. It's the structural imbalance in the economy.

Also, we have reached the tipping point on pension funds between private and governmental. This will have future repercussions because it says a lot about the ability to generate growth by savings.

This approach has now been tested on two recessions since its intro in 1998. Oh, wait, make that three.... See the updated discussion here. The Chauvet-Piger method is strong and rapid. this summer we exceeded the lower bound, and now (October) it says we are in a recession. The interesting thing about this method is that it also "catches" the beginning of the 2006 industrial recession in the US, which few other indicators do.

The weakness of this method is that it catches the turning points, but it does so in real-time (six to nine months ahead of NBER), whereas one would like to have the Fed and gov get six month's warning so effective interventions were possible. But no, this doesn't do it.The bottom line here is that the Fed needed to do what it is doing now back in the spring to have any hope of fending this recession off. Readers of this blog may remember CF's comments early this year that the Fed would begin buying mortgage bonds in the spring. Haha. This is why CF has the jet and they don't. There's a theory out there that the Fed is going to launch a panic buying program of 80 (double) or so to try to deal with the situation. I don't think they can. I don't think there are enough bonds out there to support it.

CFNAI diffusion: CFNAI was released today. CFNAI also produces a diffusion index. You can find this graph in their release:

One really interesting thing about CFNAI diffusion, which can generally be reproduced in other countries with reliable economic data (not China) is that in a bubble, you will usually see the first dip, a pop and then a second dip as lending compensates. I do not use this for forecasting, but I do think it catches something very real and fundamental about the US economy, which is that the forces which create recessions usually move into a play a year before the actual recession.

The Texas manufacturing survey, which was my "strong" region, was very disappointing this month. This is kind of a kick in the M_O_M confidence, because all my wonderful hopes for something mildish in the recession line kind of depend on trends that are centered in this region. The DC envelope is of course still extant, but it is supported by a flood of government money that is inevitably going to be slowly throttled down, so it's nothing you can rely on.

I try to predict recessions a year out. Freight is very helpful, but these indicators are as well for shape and timing:

Really I track changes in disposable income and M_O_M calculated changes in real money supply, but these three sets of data serve as a useful check on my own numbers. The utilities change over time will give me a helpful read on sensitivity to changes in real money supply. When utility usage is stagnant, the economy is weak and very sensitive to negative changes. The current period of stagnation has endured since 2007, and is similar only to the period from 78-83.

Producer prices and consumer prices give me timing info. They will take an initial fall when the economy is seizing up, and then increase as we go into the full recession onset. Recessions have different shapes, and the price spread for businesses is one of the determining factors. When businesses find themselves with compressing profit margins due to high costs and price sensitivity in sales, they have to cut their operating costs, which generates waves of negative diffusion across the economy. This shows up in personal income trends:

Here we have a rather busy graph showing utilities (to show the correlation), real retail and food services sales in green, real disposable personal income and real personal consumption expenditures, and then, in purple, the dire real personal income excluding current transfer receipts.

In detail, the same series displayed so that you can see them:

To this one I have added the previous retail series in blue. So jagged blue and green are retail sales. Red/orange are real personal disposable personal income and Personal consumption (which captures non-retail sales as well). Then, in the heavy purple line, we have real personal income excluding government benefits, i.e., income generated by the private economy.

Now real personal income doesn't account for tax changes - remember that.

So now we come into a mild recessionary period with these mechanics. I have included the history so that you can see that the massive gap which opened up between the purple (privately generated income) and the red (all personal income less taxes) didn't exist in the 79-83 protracted slump.

It's blindingly obvious that spending is now dependent on government transfers to people. Whereas real personal consumption is higher than it was entering the recession, private incomes have not recovered nearly to the same point - they are back to 2006 levels. Nor are we closing the gap very fast at this point, which means that our tax basis isn't improving very much.

The gap may be widening now, which is what one would expect in a mild recession combined with a wave of retirements.

We are running a massive structural deficit:

Not surprisingly, this has generated a massive rise in issued federal government debt:

Company profits cannot be taxed at any levels that could remotely remedy the situation:

The first graph shows net worths - and note that on a market basis, net worths of nonfinancial corporations has not recovered to the pre-recession basis, much less grown. The bottom line - flow - trade receivables - shows that businesses are now growing, but with receivables at about 2.6 trillion, it is pretty obvious that you are not going to close a trillion dollar deficit by taxing corporate profits.

Furthermore, companies are borrowing to finance the growth you see:

So don't expect them not to be very responsive to tightening profits. They'll economize quickly, and they are sensitive to spreads of all kinds.

If you raise personal taxes a lot, you cut the purple line (income generated by the private economy), which may make things worse. Therefore, the problem is not really the recession we've got. It's the structural imbalance in the economy.

Also, we have reached the tipping point on pension funds between private and governmental. This will have future repercussions because it says a lot about the ability to generate growth by savings.

Sunday, November 25, 2012

Shoppertrak Interruption

Okay, okay, I gag every time I try to write about MMT. But I will.

However, a short, slightly amusing interlude with Shoppertrak:

Black Friday estimated sales fall from 11.4 billion to 11.2 billion.

Explanation offered: Thanksgiving Day sales!

But let us turn the clock back to this time in 2011:

However, a short, slightly amusing interlude with Shoppertrak:

Black Friday estimated sales fall from 11.4 billion to 11.2 billion.

Explanation offered: Thanksgiving Day sales!

But let us turn the clock back to this time in 2011:

More customers shopped the Sunday before Thanksgiving than the days following Black Friday, according to ShopperTrak, a leading provider of retail and mall foot-traffic counting services.Nonetheless, they managed to rack up nice gains in 2011. The full low-down comes next Tuesday, and it will be estimated, so don't place too much reliance on these numbers.

Both Black Saturday and Black Sunday showed year-over-year losses in retail sales and foot-traffic, which caused the entire Black Friday weekend to realize a 1.9% sales increase and 1.8% decline in foot-traffic when compared with the same period last year, ShopperTrak said. But the week leading up to Black Friday (ending Nov. 26), saw a 4.4% increase in sales, when compared to the same week in 2010. Black Sunday (Nov. 27) also saw a 1.7% decrease in enclosed mall foot-traffic, compared with the previous Sunday (Nov. 20).

“Retailers offered door-busters and other pre-holiday specials earlier in the Thanksgiving week to ensure they had the best opportunity to capture value-conscious shoppers,” said ShopperTrak founder Bill Martin. “Our customers have access to real-time traffic information, and they succeeded in taking share earlier than they had in past years.

Friday, November 23, 2012

Modern Money Theory

I would not do this, except some person has posted about this travesty of economics on MY INNOCENT BLOG. I cannot let it pass.

However it is excruciatingly painful and so first, to concentrate the mind, may I suggest the Mash theme? It goes right along with Modern Money theory. Suicide is painless.... Lalalala. But not for the survivors, huh? If you plan to be among them, or you plan for any of those you love to be among the survivors, Modern Money theory is not for you, because Modern Money theory is a justification for an economic suicide.

Modern Money theory is indeed being pushed by some idiot economists as if it were some new revelation, but indeed, the idea that governments can print money indefinitely is not. It's been tried a number of times. One example is the Mississippi Bubble, aka France's foray into paper money. As our Modern-Money-maimed commenter explains:

At any given time there is a practical limit to the expansion of the supply of goods and services. Therefore, if you expand the supply of circulating money rapidly, the prices of necessary goods and services must expand to correspond, because the supply of these goods and services cannot possibly expand as quickly as the fiat money supply may.

I will expand on the unlovely real world results in my next post.

However it is excruciatingly painful and so first, to concentrate the mind, may I suggest the Mash theme? It goes right along with Modern Money theory. Suicide is painless.... Lalalala. But not for the survivors, huh? If you plan to be among them, or you plan for any of those you love to be among the survivors, Modern Money theory is not for you, because Modern Money theory is a justification for an economic suicide.

Modern Money theory is indeed being pushed by some idiot economists as if it were some new revelation, but indeed, the idea that governments can print money indefinitely is not. It's been tried a number of times. One example is the Mississippi Bubble, aka France's foray into paper money. As our Modern-Money-maimed commenter explains:

There are now economists tauting the idea that the U.S. could never default on it's debt Modern Money Theory True or False? (we haz a winner!)

Just like a household, government has to finance it's spending out of it's income or through borrowing? The role of taxes is to provide finance for government spending? The National Government borrows money from the private sector to finance the budget deficit? By running budget surpluses the government takes pressures off interest rates because more funds are then available for private sector investment projects? Persistent budget deficits will burden future generations with inflation and higher taxes? Running budget surpluses now will help build up the funds necessary to cope with the aging population in the future? All the above are false. St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational. Moreover, there will always be a market for U.S. government debt at home because the U.S. government has the only means of creating risk-free dollar-denominated assets..." Government can never run out of dollars. It can never be forced to default. It can never be forced to miss a payment. It is never subject to the whims of "bond vigilantes".To which History, rolling around laughing and holding its sides, replies:

The weak spot in Law's scheme was his willingness to issue more bank notes to fund purchases of shares in the company. Stock prices began falling in January 1720 as some investors sold shares to turn capital gains into gold coin. To stop the sell-off, Law restricted any payment in gold that was more than 100 livres. The paper notes of the Bank Royale were made legal tender, which meant that they could be used to pay taxes and settle most debts. The company was trying to get people to accept the paper notes rather than gold. The bank subsequently promised to exchange its notes for shares in the company at the going market price of 10,000 livres. This attempt to turn stock shares into money resulted in a sudden doubling of the money supply in France. It is not surprising then that inflation started to take off. Inflation reached a monthly rate of 23 percent in January 1720.But no still-rational reader needs to read about the tragic history of vastly expanding money supplies duly followed by vastly collapsing monetary systems. No, those with a trace of actual functional brain power left only need to think about the definition of money. The definition of money I use is a functional one - money is a proxy for the exchange of goods and services.

At any given time there is a practical limit to the expansion of the supply of goods and services. Therefore, if you expand the supply of circulating money rapidly, the prices of necessary goods and services must expand to correspond, because the supply of these goods and services cannot possibly expand as quickly as the fiat money supply may.

I will expand on the unlovely real world results in my next post.

Wednesday, November 21, 2012

Happy Thanksgiving!!!

The truce between Hamas and Israel is the right way to start this thing off.

Well, I know everyone's worried about things (or unconscious), but this is the time to be thankful for everything one has, and all those loved ones one has had in one's life even if they are no longer with you.

I hope you all have a wonderful day with your dear ones.

Prayers for Jimmy and his wife, please.

Well, I know everyone's worried about things (or unconscious), but this is the time to be thankful for everything one has, and all those loved ones one has had in one's life even if they are no longer with you.

I hope you all have a wonderful day with your dear ones.

Prayers for Jimmy and his wife, please.

Monday, November 19, 2012

Howard!!!

If it's the Season of Bling, we must watch for Howard. He's so great.

Sunday, November 18, 2012

Financial Impressionism I

I value your comments, and some of them will come back to haunt us all in the final impressionistic masterpiece. For today, we will concentrate on the FHA actuarial evaluation of the MMI fund (the fund that insures amortizing mortgages). There is another reverse mortgage insurance fund, but we'll ignore that for now.

The report can be found here. It's 235 pages, so we can guess that few journalists will bother to get past the executive summary, and thus, our Monte Carlo simulation predicts with some confidence that they will miss such gems as scenario V8, which begins on internal page 62 and external page 73. The dominant feature of this scenario is that incorporates not the Moody's forecast, which has interest rates rapidly rising, but what the Fed has PROMISED TO DO.

Now you may feel that using the Fed's promises to run simulations of estimated fund values is a hazardous effort, but in banking, it is the common practice, especially when the Fed has already begun doing that which it has promised to do and there is every evidence that they will be able to do what they have promised to do and the promise covers the near term period (i.e. the next two or three years).

As the firm which did the analysis explains:

On internal page 64 and external page 75, there is a nice summary chart which shows the results of various scenarios and Monte Carlo results. Two of these have the fund still negative in 2019.

The current value has to center on the low interest (V8) to the extreme right for the beginning point. It's important to note that there are offsetting effects in rate assumptions. A protracted period of low interest rates reduces fund values by reducing investment returns, but it also tends to sustain housing values. Rapidly rising interest rates (ain't gonna happen) prevents prepayments to a high extent (controlling adverse sort), but it tends to suppress housing values, which increases expected losses.

The second highly meaningful variable is expected economic performance. In a few months, once the dust has settled in DC, we can say more about that. However, given my recession call I am somewhat more negative on that trajectory than the mean assumptions contained in this report.

The bottom line is that there is a very real chance that the MMI fund will be negative or marginally valuable in 2019. Right now this is unimportant, except that legislatively, the fund is supposed to add up to 2% of the book. So theoretically Congress has to intervene.

But the theory does not concern anyone, because under the current law, even if FHA has no capital reserves it has an open checkbook with the Treasury to pay claims.

However in 2019 it should concern us, because that is past the event horizon when future federal borrowing becomes far more difficult. A legal right to something does not mean anything when the right cannot be exercised in the real world.

So what you, the taxpayers, need is for this fund to come back into a meaningfully positive balance before 2017. If not, you will be forced to kick in the funds to make that happen considerably before 2019, because if investors get worried about the value of FHA insurance, a fan-excrement catastrophe occurs which will just crush the economy.

The first-time homebuyer is a crucial part of our housing economy, but even well-qualified first-time buyers are going to be cash short for a long time to come.

Student loans are a crucial reason. I know a young couple that are the "winners" in today's economy by any standards. They are both young, healthy, hardworking, intelligent and attractive. The guy graduated in 2010, and got a finance job as a trader. He has been quite successful and has since moved to another firm. He is earning in the six figures. She graduated this May and got a job. Their total gross income is definitely close to 150K. Both probably will have stable employment. They are very committed to each other and will get married eventually, but for now she lives at home and he does not have a car and lives in the city. They are trying to pay off their student loans before making ANY purchases, even of furniture or a second car. That's because their student loans are close to their pre-tax income. It will take them years to pay them off, and then they will have to buy two cars before even considering saving to buy a home.

Rents are high, but FHA loans are the only game in town for most first-time buyers. If you let FHA go down, you can kiss housing values goodbye, which paradoxically makes the FHA situation much worse. So this is one of the fundamentals of any reasonable future economy that does not look Greco-Spanish.

The report can be found here. It's 235 pages, so we can guess that few journalists will bother to get past the executive summary, and thus, our Monte Carlo simulation predicts with some confidence that they will miss such gems as scenario V8, which begins on internal page 62 and external page 73. The dominant feature of this scenario is that incorporates not the Moody's forecast, which has interest rates rapidly rising, but what the Fed has PROMISED TO DO.

Now you may feel that using the Fed's promises to run simulations of estimated fund values is a hazardous effort, but in banking, it is the common practice, especially when the Fed has already begun doing that which it has promised to do and there is every evidence that they will be able to do what they have promised to do and the promise covers the near term period (i.e. the next two or three years).

As the firm which did the analysis explains:

In a press release during August of 2011, the Federal Reserve Board announced its intention to keep the federal funds rate low for the next two years. On September 13, 2012 the Federal Reserve Board announced that “……the Committee also decided today to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that exceptionally low levels for the federal funds rate are likely to be warranted at least through mid-2015.” Based on this new position, interest rates are likely to remain at their currently very low levels for an extended time.

Hence, for the third scenario we coupled the baseline home price scenario with an interest rate path that remains at the current very low level for another two years. Rates then gradually rise toward the long-term stable levels of Moody’s baseline scenario. This low interest- rates scenario is constructed to understand better the impact of the performance of the Fund with respect to a persistence of unusually low rates. Exhibit V-8 indicates that under this scenario the economic value of the FY 2012 Fund would be lower than the baseline by $17.58 billion, at negative $31.06 billion. This is similar to the 5th worst path in the simulation, which indicates a 5 percent chance the economic value can be lower than that of this low interest rate scenario.So while our fearless analysts have earlier told us that there is an 80% chance that the current value of the fund is between -25 billion and +1.6 billion, or something very similar (I'm laughing so hard I can't focus my eyes well), now they are confessing that they get a dramatically worse result if they believe the Fed. This is like reading Chinese corporate financials. It also totally contradicts the executive summary, which is why you should never read the executive summaries. They exist to corrupt your mind.

On internal page 64 and external page 75, there is a nice summary chart which shows the results of various scenarios and Monte Carlo results. Two of these have the fund still negative in 2019.

The current value has to center on the low interest (V8) to the extreme right for the beginning point. It's important to note that there are offsetting effects in rate assumptions. A protracted period of low interest rates reduces fund values by reducing investment returns, but it also tends to sustain housing values. Rapidly rising interest rates (ain't gonna happen) prevents prepayments to a high extent (controlling adverse sort), but it tends to suppress housing values, which increases expected losses.

The second highly meaningful variable is expected economic performance. In a few months, once the dust has settled in DC, we can say more about that. However, given my recession call I am somewhat more negative on that trajectory than the mean assumptions contained in this report.

The bottom line is that there is a very real chance that the MMI fund will be negative or marginally valuable in 2019. Right now this is unimportant, except that legislatively, the fund is supposed to add up to 2% of the book. So theoretically Congress has to intervene.

But the theory does not concern anyone, because under the current law, even if FHA has no capital reserves it has an open checkbook with the Treasury to pay claims.

However in 2019 it should concern us, because that is past the event horizon when future federal borrowing becomes far more difficult. A legal right to something does not mean anything when the right cannot be exercised in the real world.

So what you, the taxpayers, need is for this fund to come back into a meaningfully positive balance before 2017. If not, you will be forced to kick in the funds to make that happen considerably before 2019, because if investors get worried about the value of FHA insurance, a fan-excrement catastrophe occurs which will just crush the economy.

The first-time homebuyer is a crucial part of our housing economy, but even well-qualified first-time buyers are going to be cash short for a long time to come.

Student loans are a crucial reason. I know a young couple that are the "winners" in today's economy by any standards. They are both young, healthy, hardworking, intelligent and attractive. The guy graduated in 2010, and got a finance job as a trader. He has been quite successful and has since moved to another firm. He is earning in the six figures. She graduated this May and got a job. Their total gross income is definitely close to 150K. Both probably will have stable employment. They are very committed to each other and will get married eventually, but for now she lives at home and he does not have a car and lives in the city. They are trying to pay off their student loans before making ANY purchases, even of furniture or a second car. That's because their student loans are close to their pre-tax income. It will take them years to pay them off, and then they will have to buy two cars before even considering saving to buy a home.

Rents are high, but FHA loans are the only game in town for most first-time buyers. If you let FHA go down, you can kiss housing values goodbye, which paradoxically makes the FHA situation much worse. So this is one of the fundamentals of any reasonable future economy that does not look Greco-Spanish.

Saturday, November 17, 2012

Q3 Chargeoffs and Delinquencies

Not going in the right direction as far as residential mortgages. This is deeply relevant to quite a lot of discussion that's going on, including FHA prospects.

When I have time I will babble on about this, but the bottom line is that an SA rate of 1.99 chargeoffs on residential mortgages for the 100 largest banks is quite some warning signal. That's the worst it has been since 2010.

Delinquencies for the 100 largest banks on residential mortgages are up to a staggering 12.13%, the worst since the third quarter of 2010.

And I have to read Fed droning about mortgage standards being too tight!!! These people have their heads up their butts. I find it hard to blog any more, because all I want to do is cuss in print.

This is mostly due to a bad economy and declining incomes, but the big wave of housing tax credits also generated a stream of bad buyers (overextended) who are now mostly underwater. Defaults on this latest crop will peak around 2014. Bad lending is the gift that just keeps giving.

The FHA actuarial report on the MMI was published yesterday. In one year, they calculate that the MMI present value dropped over 14 billion dollars. The largest single contribution (over 8 billion in the red) was due to low investment returns, largely courtesy of the Fed but also due to a slack economy.

In my opinion the Fed has created a deflationary spiral. It's clear that banks need to tighten credit standards now. This is going to be plug-ugly. Eeyore (CF) wins the palm again.

When you drop interest rates low initially, it gives a big boost. The assets out there are paying higher interest rates, it's cheap to borrow, and for a time the economy is boosted by the ability to borrow at low rates for new investment plus the high returns from prior lending. But as the thing wears on, return on total assets keeps dropping due to turnover/expiration of higher rate loans (assets).

After half a decade of this, we are into the worst of all possible scenarios in which the need for future saving is skyrocketing due to low investment returns, but lending decisions have to become more conservative due to a poor economy and the disproportionate role that the risk premium must now play in lending. When interest rates for prime borrowing are very low, the relative impact of risk is very high.

Or to put it another way, to cover that 1.99% chargeoff ratio you need to add 2% to 2.5% to the base interest rate. The 10 year is well below 2%. Thus the risk premium is more than the base interest rate. If you make a mistake and take on a little more risk than you had planned, any possible profits from the loan portfolio will be swallowed up like the whale gulped down Jonah, but unfortunately, there will be no happy ending in three days.

Therefore, you go conservative. You cannot compensate by charging significantly higher rates to riskier borrowers, because in a couple of years your better borrowers will refi out into significantly lower cost loans and you will be left with a load of disaster. There's no way to compensate for this without throwing yourself into the abyss of adverse selection. The only way out is to lend very very conservatively.

When I have time I will babble on about this, but the bottom line is that an SA rate of 1.99 chargeoffs on residential mortgages for the 100 largest banks is quite some warning signal. That's the worst it has been since 2010.

Delinquencies for the 100 largest banks on residential mortgages are up to a staggering 12.13%, the worst since the third quarter of 2010.

And I have to read Fed droning about mortgage standards being too tight!!! These people have their heads up their butts. I find it hard to blog any more, because all I want to do is cuss in print.

This is mostly due to a bad economy and declining incomes, but the big wave of housing tax credits also generated a stream of bad buyers (overextended) who are now mostly underwater. Defaults on this latest crop will peak around 2014. Bad lending is the gift that just keeps giving.

The FHA actuarial report on the MMI was published yesterday. In one year, they calculate that the MMI present value dropped over 14 billion dollars. The largest single contribution (over 8 billion in the red) was due to low investment returns, largely courtesy of the Fed but also due to a slack economy.

In my opinion the Fed has created a deflationary spiral. It's clear that banks need to tighten credit standards now. This is going to be plug-ugly. Eeyore (CF) wins the palm again.

When you drop interest rates low initially, it gives a big boost. The assets out there are paying higher interest rates, it's cheap to borrow, and for a time the economy is boosted by the ability to borrow at low rates for new investment plus the high returns from prior lending. But as the thing wears on, return on total assets keeps dropping due to turnover/expiration of higher rate loans (assets).

After half a decade of this, we are into the worst of all possible scenarios in which the need for future saving is skyrocketing due to low investment returns, but lending decisions have to become more conservative due to a poor economy and the disproportionate role that the risk premium must now play in lending. When interest rates for prime borrowing are very low, the relative impact of risk is very high.

Or to put it another way, to cover that 1.99% chargeoff ratio you need to add 2% to 2.5% to the base interest rate. The 10 year is well below 2%. Thus the risk premium is more than the base interest rate. If you make a mistake and take on a little more risk than you had planned, any possible profits from the loan portfolio will be swallowed up like the whale gulped down Jonah, but unfortunately, there will be no happy ending in three days.

Therefore, you go conservative. You cannot compensate by charging significantly higher rates to riskier borrowers, because in a couple of years your better borrowers will refi out into significantly lower cost loans and you will be left with a load of disaster. There's no way to compensate for this without throwing yourself into the abyss of adverse selection. The only way out is to lend very very conservatively.

Friday, November 16, 2012

Friday Notes

Industrial production. The note says that Sandy should be about -1% effect, but I don't think it shows up in October. The storm effects begin the 29th, and after that the 30th and the 31st of October. The supply chain effect and most reductions should show up much more in November. Publishing I'll buy, but factories in Ohio weren't affected much in October.

Anyway, headline is -0.4% for October. The sequence here as we now have it beginning in May is 0.0, 0.0, +0.7 in July, -1.1% in August, +0.2 in Sept, and now -0.4%. Now the July-August swings are really probably due to MV production calendars and SA effects, so the increase in July comes strongly back out of August. In other words, what I'm saying is that this series has been nearly static for months.

FHA report to be released later on fiscal problems and taxpayer bailout required in 2013. 'Cause 13s FHA's lucky number, and when you are talking this much luck, you like to release it on Friday. This is a really interesting story. FHA hadn't published their annual report to Congress, but we can tell what it's going to say by looking at their last quarterly here .

There's going to be a lot of nonsense written over this story, but you can cut through it by chanting "cash flow, cash flow, cash flow" to yourself and "Extend & pretend" when you get dizzy. On the quarterly report on internal page 12, external page 13, you will find a handy chart which summarizes cash flow effects. The rolling 4 quarter sequence is (millions)

Additional ugly detail: On new loans, the estimated credit premium is -2.75%, meaning that each poor sucker who gets an FHA loan now pays the insurance fund an average of 2.75% of the insured amount. In short, these innocents are paying for the bling of yesteryear, not to mention all those loan deals announced by an infinitely wise and kind government that's really here to help you. But it's not enough to cover the cash shortfall.

Premiums can't be raised further, because the result would be to make it much cheaper for better quality borrowers to go outside the FHA, which would further drop new loan generation and worsen credit quality. See the chart on internal page 4, external page 5 of new loan generation. That huge 2009 bulge is going to take some time to work off.

The refinance share is now around 40%, meaning that in many cases these are previous FHA buyers who are refinancing to get lower rates. Thus the loan drops out and then returns. That makes it more difficult to build the total base of good loans. Thus, as FHA elegantly explains on external page 15:

On internal page 15, external page 16 (I hope you are noting that pattern), you will find a chart showing serious deliquency rates. The current low was 8.18% in Q3 2011. The current quarter is 9.44%. However, seasonally adjusted, that turns to 9.94% This is a new high by a considerable fraction, which fact was not mentioned earlier.

When the full report is published, it will appear here. The full report includes an independent actuarial evaluation, which is probably going to stress the unfavorables, such as the effect of the streamlined (non-underwritten) refis which are not included in the generic statistics.The actuarial reviews of the MMI (mortgage insurance fund) are published here.

Anyway, headline is -0.4% for October. The sequence here as we now have it beginning in May is 0.0, 0.0, +0.7 in July, -1.1% in August, +0.2 in Sept, and now -0.4%. Now the July-August swings are really probably due to MV production calendars and SA effects, so the increase in July comes strongly back out of August. In other words, what I'm saying is that this series has been nearly static for months.

FHA report to be released later on fiscal problems and taxpayer bailout required in 2013. 'Cause 13s FHA's lucky number, and when you are talking this much luck, you like to release it on Friday. This is a really interesting story. FHA hadn't published their annual report to Congress, but we can tell what it's going to say by looking at their last quarterly here .

There's going to be a lot of nonsense written over this story, but you can cut through it by chanting "cash flow, cash flow, cash flow" to yourself and "Extend & pretend" when you get dizzy. On the quarterly report on internal page 12, external page 13, you will find a handy chart which summarizes cash flow effects. The rolling 4 quarter sequence is (millions)

-249This is the taxpayer's problem. The predominant reason for this is that all that legal activity that delayed foreclosures delayed FHA claims, so now they are losing their butts.

-428

-1,154

-1,706.

Additional ugly detail: On new loans, the estimated credit premium is -2.75%, meaning that each poor sucker who gets an FHA loan now pays the insurance fund an average of 2.75% of the insured amount. In short, these innocents are paying for the bling of yesteryear, not to mention all those loan deals announced by an infinitely wise and kind government that's really here to help you. But it's not enough to cover the cash shortfall.

Premiums can't be raised further, because the result would be to make it much cheaper for better quality borrowers to go outside the FHA, which would further drop new loan generation and worsen credit quality. See the chart on internal page 4, external page 5 of new loan generation. That huge 2009 bulge is going to take some time to work off.

The refinance share is now around 40%, meaning that in many cases these are previous FHA buyers who are refinancing to get lower rates. Thus the loan drops out and then returns. That makes it more difficult to build the total base of good loans. Thus, as FHA elegantly explains on external page 15:

The serious delinquency rate held steady at 9.4% this quarter. This level is about 1.4% higher than this time a year ago. Two factors appear to be driving this result. The first is the persistency of loans in 90-day delinquency as lenders attempt to craft workout plans, and persistency of loans in foreclosure processing. The second is that the historically large FY 2009 and FY 2010 books-of-business are at the age where their serious delinquency rates are increasing toward their life-cycle peaks. Because those books are much larger than is the new FY 2011 book, their loan-age seasoning patterns are not offset by the low default rates on recent endorsements.BUT WAIT THIS IS GONNA GET MUCH BETTER DUE TO THE MAGIC OF FANTASY!!!!!

On internal page 15, external page 16 (I hope you are noting that pattern), you will find a chart showing serious deliquency rates. The current low was 8.18% in Q3 2011. The current quarter is 9.44%. However, seasonally adjusted, that turns to 9.94% This is a new high by a considerable fraction, which fact was not mentioned earlier.

When the full report is published, it will appear here. The full report includes an independent actuarial evaluation, which is probably going to stress the unfavorables, such as the effect of the streamlined (non-underwritten) refis which are not included in the generic statistics.The actuarial reviews of the MMI (mortgage insurance fund) are published here.

Thursday, November 15, 2012

Regarding Initial Claims

The release is here. NSA claims increased over 100K to 466K. The SA headline is 439K, with a four-week moving average of 383,750. I am a bit skeptical over the attribution of all of this rise to Sandy. The prior week claims (headline 361K) were probably depressed because many state offices were closed, and so they showed up this week. But many of those were not hurricane-related, because of filing requirements. Figure a non-hurricane moving average of around 373K, and you are probably pretty close.

Also, the 11/3 total of continuing claims has risen noticeably to 3.3 million. We'll have to wait a bit to see what this all means - much of hurricane-related disturbances will wash out in the next month. In the heavily affected states, there will be some hiring related to the storm. Several of these states now have large swaths of blue tarp country.

I remain comfortable with my recession call based on freight and producer prices etc. Grocery pricing has been in the recession zone for months. There is very obviously extreme price sensitivity in food and even more so on ancillary products, indicating that consumers are pressed and stretching budget dollars. There is an income gap - look at the negatives on real average hourly earnings over the last three months. Now that is not all bad news - some new jobs are being created, but at low wage levels so real average hourly earnings tend to be a bit suppressed. However not enough jobs are being created to account for all this - over the year real average weekly earnings fell 0.6% after the prior year's drop of 1.1%. Over time this adds up, as the release indicates:

Will we start restoring FICA payroll taxes? If so, it's going to add to this trend, won't it? If not, how can we claim with a straight face that we are committed to the SS system? But do we want to begin next year by knocking another 1 or 2% off take home pay? Yikes.

We are helped by the season of Bling which moves product, but the season of Ding is right behind:

I am skeptical of the theory that most of the retail sales drop in October was due to Sandy. Sandy probably had a negative contribution, but a small one only. There were indications of weakness earlier in the month.

Empire State Manufacturing Survey was mostly negative in employment, with sharp declines in the work week and a negative number of workers over -14. Nah. The future indices for employment seem to indicate that most of this is expected to continue, and therefore it can't be attributed to Sandy. Philadelphia Fed was negative also, which fits in with the prior months of diminishing future expectations.

Now, even if nothing else were changing in 2013, we'd still have a relative problem because of two quarters of low business investment and the draw forward on defense spending by the federal government in Q3.

What I have now is that we entered a very mild recession in July of this year. By August the diffusion was obvious to me. This now gets accentuated by two things - the impossibility of continuing the car financing and the need for the federal government to begin to get serious.

I have no idea what the federal government will do, and thus, like Neil, I find myself in a state of puzzled suspense.

PS: I am also a little bit wary of the attribution of lower auto sales to Sandy. It's possible, but the auto advertising I heard earlier in the month indicated levels of desperation to move product that are usual in a recession. It's spotty across the country, but MV inventories are rising and sooner or later auto production will correct somewhat as a result of the financing problem and the inventory numbers. That won't help the economy.

Also, the 11/3 total of continuing claims has risen noticeably to 3.3 million. We'll have to wait a bit to see what this all means - much of hurricane-related disturbances will wash out in the next month. In the heavily affected states, there will be some hiring related to the storm. Several of these states now have large swaths of blue tarp country.

I remain comfortable with my recession call based on freight and producer prices etc. Grocery pricing has been in the recession zone for months. There is very obviously extreme price sensitivity in food and even more so on ancillary products, indicating that consumers are pressed and stretching budget dollars. There is an income gap - look at the negatives on real average hourly earnings over the last three months. Now that is not all bad news - some new jobs are being created, but at low wage levels so real average hourly earnings tend to be a bit suppressed. However not enough jobs are being created to account for all this - over the year real average weekly earnings fell 0.6% after the prior year's drop of 1.1%. Over time this adds up, as the release indicates:

Since reaching a peak in October 2010, real average weekly earnings for production and nonsupervisory employees has fallen 2.9 percent.

Will we start restoring FICA payroll taxes? If so, it's going to add to this trend, won't it? If not, how can we claim with a straight face that we are committed to the SS system? But do we want to begin next year by knocking another 1 or 2% off take home pay? Yikes.

We are helped by the season of Bling which moves product, but the season of Ding is right behind:

I am skeptical of the theory that most of the retail sales drop in October was due to Sandy. Sandy probably had a negative contribution, but a small one only. There were indications of weakness earlier in the month.

Empire State Manufacturing Survey was mostly negative in employment, with sharp declines in the work week and a negative number of workers over -14. Nah. The future indices for employment seem to indicate that most of this is expected to continue, and therefore it can't be attributed to Sandy. Philadelphia Fed was negative also, which fits in with the prior months of diminishing future expectations.

Now, even if nothing else were changing in 2013, we'd still have a relative problem because of two quarters of low business investment and the draw forward on defense spending by the federal government in Q3.

What I have now is that we entered a very mild recession in July of this year. By August the diffusion was obvious to me. This now gets accentuated by two things - the impossibility of continuing the car financing and the need for the federal government to begin to get serious.

I have no idea what the federal government will do, and thus, like Neil, I find myself in a state of puzzled suspense.

PS: I am also a little bit wary of the attribution of lower auto sales to Sandy. It's possible, but the auto advertising I heard earlier in the month indicated levels of desperation to move product that are usual in a recession. It's spotty across the country, but MV inventories are rising and sooner or later auto production will correct somewhat as a result of the financing problem and the inventory numbers. That won't help the economy.

Tuesday, November 13, 2012

Pretty Much Back

I've caught up with the news somewhat. I spent a sobering Veteran's Day weekend feebly trying to fix the driveway, wondering what the vets I knew would think about what this country has become.

Regarding economics - Europe continues to slide down the ladder of failure. The latest tocsin of despair is the drive to stop foreclosures in Spain. While that might sound fine and dandy, it seems likely to put some surviving banks under. That cannot be helpful.

In Europe, the bright spot is Ireland, which is expanding. See the October Euro Markit composite. Unfortunately, Ireland's contribution is quite outweighed by Germany's slump. Germany now appears in recession. Yes, I know that's the German version, but I don't see the English version. Just look at the graphs and numbers. This is reinforced by the Construction PMI (English version), which shows a very significant contraction. Italy is contracting at a softer pace.

Asia: Singapore - GDP contracted in the latest quarter. The verbiage is positive, the data is not. However it is contracting at a soft pace. China - well, we have loud cries of stabilization, but I am dubious. I think the net forward impetus is still negative. They are pushing it a bit, and I can only hope that involves hiring a bunch of construction inspectors, so those new subway tunnels don't start falling in on people's heads in a year or two. Japan is in a frank slump. The impending rise in sales taxes is hardly going to help. The disputes with China will hurt both countries. India is very weak indeed, but central bank stimulus is on hold due to consumer inflation near 10%.

US: NACM (business-to-business credit) showed the first signs of real problems. There was a big slump in payments, which, if continued, would indicate a significant problem that is doomed to affect the flow of credit. Chicago PMI - in slight contraction for the second month. Order backlogs are firmly negative and the effects are showing in employment, which is near contraction at almost a three-year low. Freight strongly supports the idea that the US economy continues to slow. Small business (NFIB) report for October shows continued weakness in earnings and sales. Earnings trends are declining but almost exactly where they were last year. However sales are worsening and are below where they were last year. Since April actual sales trends have been dropping very slowly, but this continued erosion suggests a poor business climate. October is one of the months with a big sample, and this one was particularly large.

One of the most interesting reports I have looked at over the last few days was consumer credit. There has been a remarkable rise in Fed gov (aka student loan debt) reported July-Sept on an NSA basis - more than 37 billion, or almost 8%. Of course this corresponds with the beginning of the fall semester, but it does answer one of the questions that was bothering me - where did the extra money come from for retail sales? Not all of this money went for tuition - some is being used for living expenses and showing up in retail numbers. Compare that number to the NSA rise in revolving July-Sept of just under 5 billion dollars. The student loan debt shows up in the non-revolving section, which in total over that period only rose 50.5 billion dollars. These are acutely imbalanced credit flows and a lot of this money won't be paid back. At this rate, student loan bad debts are going to be more of a burden on the taxpayer than Fannie/FHA/Freddie, which is saying a lot.

I'm extremely comfortable with my US recession call, and apparently Treasury buyers are too.

Another post, whenever I get around to it, on election effects.

Regarding economics - Europe continues to slide down the ladder of failure. The latest tocsin of despair is the drive to stop foreclosures in Spain. While that might sound fine and dandy, it seems likely to put some surviving banks under. That cannot be helpful.

In Europe, the bright spot is Ireland, which is expanding. See the October Euro Markit composite. Unfortunately, Ireland's contribution is quite outweighed by Germany's slump. Germany now appears in recession. Yes, I know that's the German version, but I don't see the English version. Just look at the graphs and numbers. This is reinforced by the Construction PMI (English version), which shows a very significant contraction. Italy is contracting at a softer pace.

Asia: Singapore - GDP contracted in the latest quarter. The verbiage is positive, the data is not. However it is contracting at a soft pace. China - well, we have loud cries of stabilization, but I am dubious. I think the net forward impetus is still negative. They are pushing it a bit, and I can only hope that involves hiring a bunch of construction inspectors, so those new subway tunnels don't start falling in on people's heads in a year or two. Japan is in a frank slump. The impending rise in sales taxes is hardly going to help. The disputes with China will hurt both countries. India is very weak indeed, but central bank stimulus is on hold due to consumer inflation near 10%.

US: NACM (business-to-business credit) showed the first signs of real problems. There was a big slump in payments, which, if continued, would indicate a significant problem that is doomed to affect the flow of credit. Chicago PMI - in slight contraction for the second month. Order backlogs are firmly negative and the effects are showing in employment, which is near contraction at almost a three-year low. Freight strongly supports the idea that the US economy continues to slow. Small business (NFIB) report for October shows continued weakness in earnings and sales. Earnings trends are declining but almost exactly where they were last year. However sales are worsening and are below where they were last year. Since April actual sales trends have been dropping very slowly, but this continued erosion suggests a poor business climate. October is one of the months with a big sample, and this one was particularly large.

One of the most interesting reports I have looked at over the last few days was consumer credit. There has been a remarkable rise in Fed gov (aka student loan debt) reported July-Sept on an NSA basis - more than 37 billion, or almost 8%. Of course this corresponds with the beginning of the fall semester, but it does answer one of the questions that was bothering me - where did the extra money come from for retail sales? Not all of this money went for tuition - some is being used for living expenses and showing up in retail numbers. Compare that number to the NSA rise in revolving July-Sept of just under 5 billion dollars. The student loan debt shows up in the non-revolving section, which in total over that period only rose 50.5 billion dollars. These are acutely imbalanced credit flows and a lot of this money won't be paid back. At this rate, student loan bad debts are going to be more of a burden on the taxpayer than Fannie/FHA/Freddie, which is saying a lot.

I'm extremely comfortable with my US recession call, and apparently Treasury buyers are too.

Another post, whenever I get around to it, on election effects.

Thursday, November 08, 2012

Fiat Lux!

I had a generator, but I had fled to my brother's because I didn't think I could run it safely in the second storm. Lo and behold, the power company finally came by today and fixed the downed poles - and then, this is practically miraculous - on the eleventh day, THERE WAS POWER. That was followed by phone and internet.

So now I'm really back. The generator can run the basics only.

Heh, my storm tales would fill a book. Really had a bleeping NE hurricane. Part of the roof ripped off. Trapped in house by fir tree down across driveway. No light and heat for a while, because I had given the generator to someone who needed it more. Had firewood, though.

As for the tree down across the driveway, I had cut it down to the bare trunk by hand and started to cut through the trunk by hand, and then a Good Samaritan showed up with a chain saw and finished the job. My brother came by and we (meaning really he) patched the roof with the scanty materials at hand. It held through the second storm, so we (he) did a surprisingly good job.

I escaped durance vile on Friday, and then I got the generator back late that day because the loan house got a generator. Saturday I rigged it a little house out of firewood racks, cinderblocks and a tarp, which worked surprisingly well. Then Monday of this week we wired up Superdoc's office, because he was sitting there with no lights, no heat, no computers and no phones, treating patients.

Among the more entertaining incidents, a crew of chainsaw-toting Baptists showed up and started cutting people's trees for free. This was extremely necessary, because all tree service companies are booked up solid on larger jobs.

I need a chainsaw, although I do not think I am qualified to join the Baptist group which does this.

I am tired after a lot of physical work in the cold and the damp. I have been out of touch, and I need to start baking for various tree elves. I did not see a cop the whole time, but aside from the terror of gangs of chainsaw wielding Baptists roaming around freeing people from their houses, I also did not see the need for them. Mainly it was just people helping people.

Some of the people who came in from the south (and there are tons of them) do not have clothing for this weather. They need blankets, coats, hats and so forth. So if you can donate such things, please do, and if you are in the area and see foreign work crews (even the feral chainsaw wielding Baptists), go up and ask them if they need anything, because they don't even know where to get it.

So now I'm really back. The generator can run the basics only.

Heh, my storm tales would fill a book. Really had a bleeping NE hurricane. Part of the roof ripped off. Trapped in house by fir tree down across driveway. No light and heat for a while, because I had given the generator to someone who needed it more. Had firewood, though.

As for the tree down across the driveway, I had cut it down to the bare trunk by hand and started to cut through the trunk by hand, and then a Good Samaritan showed up with a chain saw and finished the job. My brother came by and we (meaning really he) patched the roof with the scanty materials at hand. It held through the second storm, so we (he) did a surprisingly good job.

I escaped durance vile on Friday, and then I got the generator back late that day because the loan house got a generator. Saturday I rigged it a little house out of firewood racks, cinderblocks and a tarp, which worked surprisingly well. Then Monday of this week we wired up Superdoc's office, because he was sitting there with no lights, no heat, no computers and no phones, treating patients.

Among the more entertaining incidents, a crew of chainsaw-toting Baptists showed up and started cutting people's trees for free. This was extremely necessary, because all tree service companies are booked up solid on larger jobs.

I need a chainsaw, although I do not think I am qualified to join the Baptist group which does this.

I am tired after a lot of physical work in the cold and the damp. I have been out of touch, and I need to start baking for various tree elves. I did not see a cop the whole time, but aside from the terror of gangs of chainsaw wielding Baptists roaming around freeing people from their houses, I also did not see the need for them. Mainly it was just people helping people.

Some of the people who came in from the south (and there are tons of them) do not have clothing for this weather. They need blankets, coats, hats and so forth. So if you can donate such things, please do, and if you are in the area and see foreign work crews (even the feral chainsaw wielding Baptists), go up and ask them if they need anything, because they don't even know where to get it.

Lived Through It

Still no power, phone or internet service. Maybe by Monday.

I have spent the time since the storm primarily struggling with the damage and helping others, and obviously my ability to get news was limited.

As for the election, nothing changes this:

Despite anything we want, the need for massive adjustments stares us in the face.

I have spent the time since the storm primarily struggling with the damage and helping others, and obviously my ability to get news was limited.

As for the election, nothing changes this: